— Raise the full retirement age further. Starting in 2028, it would go up by one month every half-year until it reaches 68 1/2 in nine years. That means that in 101 years (1935-2036) the full retirement age would have risen 3 1/2 years — far less than the increase in average life span over the same period.

— Raise the early eligibility age. Since the 1960s, all workers have had the option of retiring at 62 with benefits reduced by around 25%. Most retirees now claim Social Security at 62, and the rising full retirement age strengthens the incentive to do so. Once it’s at 67, holding out for higher payments will mean giving up five years’ worth of benefits — a three-year gap will have widened to five.

If my first reform were enacted, the gap would grow further, to an irresistible 6 1/2 years. So Congress should return to the three-year gap by raising the early eligibility age to 65 1/2 as soon as possible.

— Change the way benefits are calculated for new recipients. At a 1983 White House Rose Garden ceremony, I sat next to a Senate member of the Social Security Reform Commission. I told him, “You can fix Social Security by not indexing the bend points for five years.” His response: “What the hell are bend points?”

Bend points determine how much your initial Social Security check will be. First they take the 35 years of your highest income. Thirty-five years ago, you were a junior employee and the dollar didn’t go as far. So each year’s wages are adjusted for inflation to compute an average monthly wage in today’s dollars.

Using the present rules, assume you’re retiring in 2022 and your average inflation-adjusted monthly wage is $6,572. Your first check would be $2,628.96 — 90% of the first $1,024 (or $921.60), plus 32% from $1,024 to $6,172 (or 1,647.36), plus 15% in excess of $6,172 (or $60).

The bend points are $1,024 and $6,172. They were $230 and $1,388 in 1982, when I wrote my constituent newsletter. The growth in benefits could be constrained by indexing the bend points every other year rather than annually for six to 10 years. In addition, the initial benefit should be based on 38 years of wages rather than 35, since Americans not only live longer but work longer, and the inflation-adjusted average wage should be discounted by 5%.

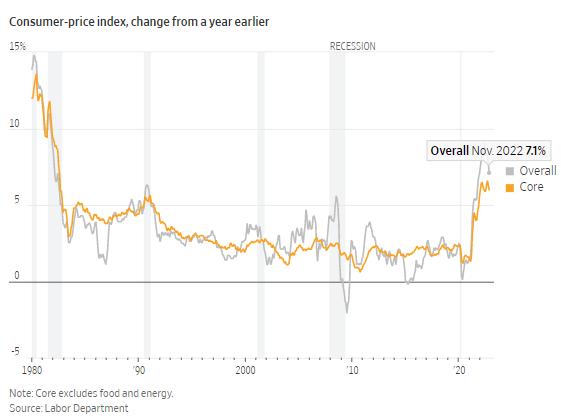

— Slow the growth of benefits for new and existing beneficiaries alike by changing the basis on which they’re indexed for inflation. All indexing of Social Security now uses the Consumer Price Index for Urban Wage Earners and Clerical Workers, or CPI-W. Economists agree that the Chained CPI is the most accurate inflation index available. Between 2000 and 2020, the Chained CPI was around 0.3 percentage point lower each year than the CPI-W. The government uses Chained CPI to index income-tax brackets and the higher CPI-W to calculate government outlays, including Social Security cost-of-living adjustments — which leads both taxes and spending to rise more quickly.

— Withhold some Social Security COLAs from higher-income retirees. Those who report income of more than $60,000 (a threshold that itself would rise with inflation) from sources other than Social Security could be denied the COLA every other year for up to six years.

— Give the COLA not annually but every 14 or 15 months using the 12 months of lowest inflation.

— Tax Social Security income for higher-bracket taxpayers, and give them the option to forgo all or part of their monthly payment. The forgone amount could be deducted as a charitable contribution. In high-income-tax states, forgoing Social Security payments would incur little or no cost. Skeptics may be surprised by how many Americans will forgo a part of their monthly checks to assure the system’s solvency for their grandchildren. The election to forgo would be reversible annually.

— Raise the payroll tax by 0.1% of wages every other year — half from withholding, half for the employer’s contribution — for 20 years, a total tax increase of 1%.