Link: https://www.brookings.edu/research/the-federal-budget-outlook-2/

PDF of report: https://www.brookings.edu/wp-content/uploads/2023/03/20230313_TPC_Gale_FiscalOutlookFINAL.pdf

Graphic:

Excerpt:

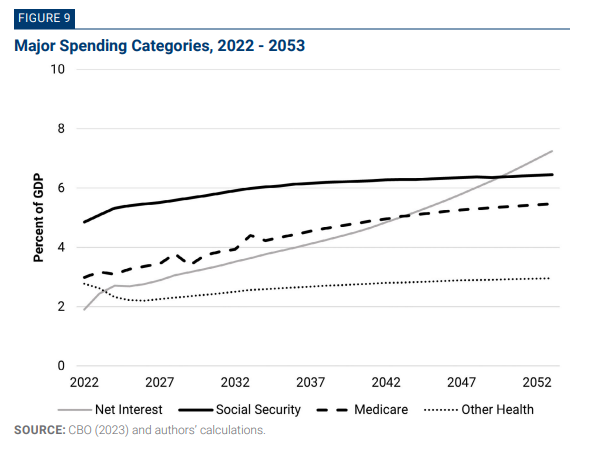

The basic story is familiar. Low revenues coupled with rising outlays on health-related programs and Social Security drive permanent, rising primary deficits as a share of the economy. Net interest payments also rise substantially relative to GDP due to high pre-existing debt, rising primary deficits, and gradually increasing interest rates. Unified deficits and public debt rise accordingly.

Under current law for the next 10 years, the CBO’s projections imply that persistent primary deficits will average 3.0% of GDP. Net interest payments will rise from 2.4% of GDP currently to 3.6% in 2033, an all-time high. The unified deficit, and even the cyclically adjusted deficit, will exceed 7% of GDP at the end of decade. Debt will rise from 98% of GDP currently to 118% by 2033, another all-time high.

Over the following two decades, the projected trends are even less auspicious. Primary deficits rise further as spending on Social Security and health-related programs continue to grow faster than GDP and revenue growth remains anemic. The average nominal interest rate on government debt rises to exceed the nominal economic growth rate by 2046, setting off the possibility of explosive debt dynamics. By 2053, relative to GDP, annual net interest payments exceed 7%, the unified deficit exceeds 11%, and the public debt stands at 195%. All these figures would be all-time highs (except for deficits during World War II and in the first two years of the COVID-19 pandemic) and would continue to grow after 2053.

Author(s): Alan J. Auerbach and William G. Gale

Publication Date: 14 Mar 2023

Publication Site: Brookings