Excerpt:

Transparency is not just a good thing for the public. A study of the 2012 Recovery Act (ARRA) showed that the biggest users of publicly available data were government officials, who used the information to track spending. Cities that do not already issue comprehensive annual financial reports (CAFRs) should adopt them for the benefit of policymakers and the public. Meet or exceed Generally Accepted Accounting Principles (GAAP) and Government Accounting Services Board (GASB) statements in your reporting. Clearly account for liabilities such as pensions, retiree health benefits and infrastructure maintenance and replacement. Have that accounting independently verified.

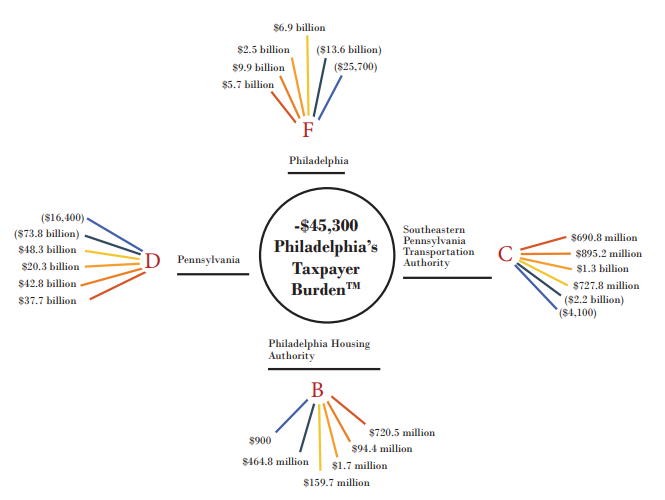

…..

According to a January 2021 report from Truth in Accounting, the top 75 US cities have a combined unfunded public pension obligation of more than $180 billion. Cities often underfund these obligations to cover budget shortcomings elsewhere, an irresponsible game of whack-a-mole.

Treasury guidance forbids using ARPA money in pension funds to cover unfunded liabilities from before the COVID emergency. It does allow spending on current payments for either defined benefit or defined contribution plans. Cities could use ARPA funds to provide additional payments to those plans to encourage employees to switch from their traditional pension to a defined contribution plan—which is a much more financially sound position for cities to be in.

Author(s): Patrick Tuohey

Publication Date: 31 May 2021

Publication Site: Better Cities Project