Graphic:

Excerpt:

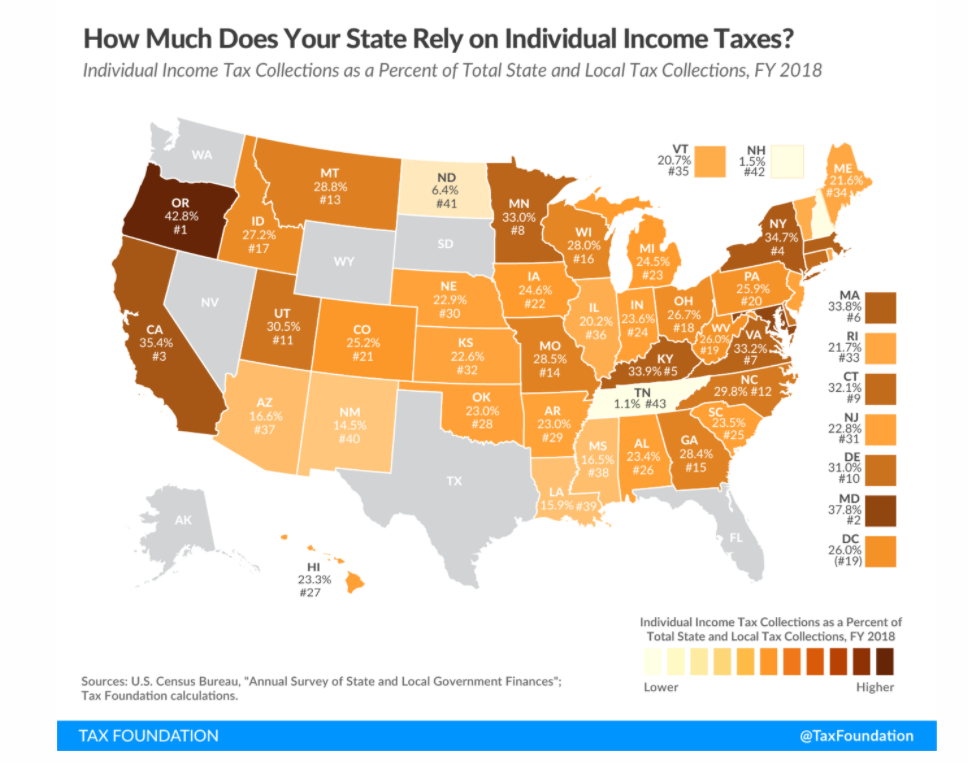

Individual income taxes are a major source of state government revenue, accounting for 38 percent of state tax collections in fiscal year 2018, the latest year of data available.

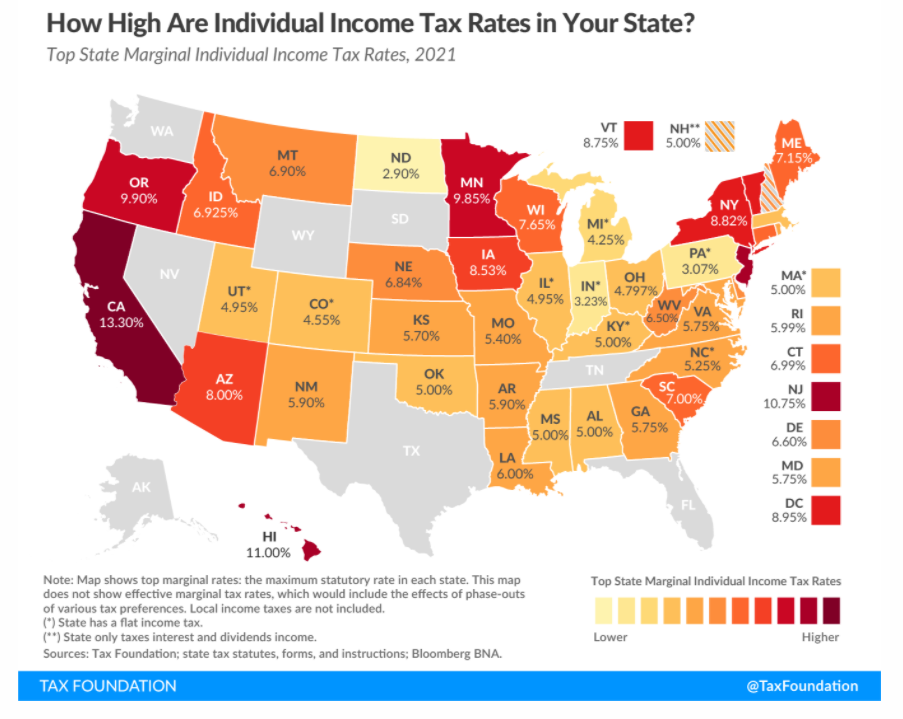

Forty-two states levy individual income taxes. Forty-one tax wage and salary income, while one state—New Hampshire—exclusively taxes dividend and interest income. Eight states levy no individual income tax at all.

Of those states taxing wages, nine have single-rate tax structures, with one rate applying to all taxable income. Conversely, 32 states and the District of Columbia levy graduated-rate income taxes, with the number of brackets varying widely by state. Hawaii has 12 brackets, the most in the country.

Author(s): Katherine Loughead

Publication Date: 17 February 2021

Publication Site: Tax Foundation