Link: https://www.washingtonpost.com/opinions/2021/09/18/tart-truth-underlying-salt-repeal-arguments/

Excerpt:

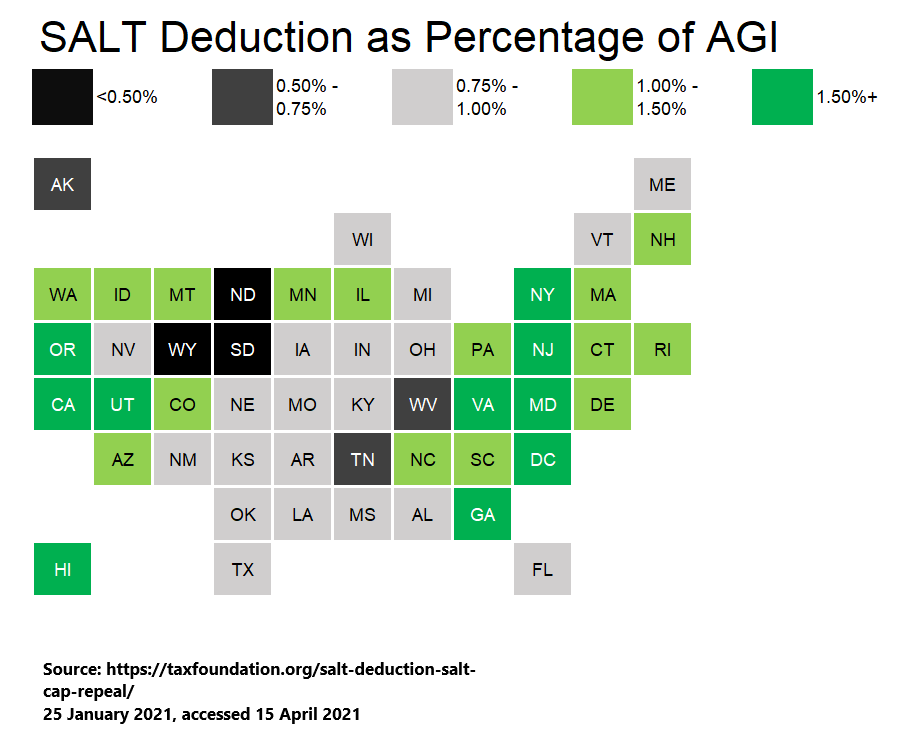

According to the Tax Foundation, just 13.7 percent of filers itemize their deductions — a prerequisite for deducting state and local taxes. Only at the top 10 percent of the income distribution do even a majority of taxpayers itemize. But among the top 1 percent of taxpayers, 92 percent do, and of course, their higher marginal tax rates make each deduction more valuable.

So it is these taxpayers whom the SALT deduction primarily benefits. According to Maya MacGuineas of the Committee for a Responsible Federal Budget, households in the top 0.1 percent of earners would receive an average benefit of about $150,000, while those in the middle would get closer to $15. Repealing the caps would cost about $350 billion by 2026, and an estimated 85 percent of that revenue would end up in the pockets of the richest 5 percent of Americans.

You can probably think of many better uses of taxpayer money than giving a tax break to the most affluent people in the most affluent parts of the most affluent states in the country. Unless, of course, you are someone who would benefit from a larger SALT deduction. As, I admit, I would.

Author(s): Megan McArdle

Publication Date: 18 Sept 2021

Publication Site: Washington Post