Press release: https://www.soa.org/resources/announcements/press-releases/2021/2021-asa-changes-member/

FAQ: https://www.soa.org/education/general-info/asa-micro-credentials/

Pathway comparison, more info: https://www.soa.org/globalassets/assets/files/edu/asa-pathway-changes.pdf

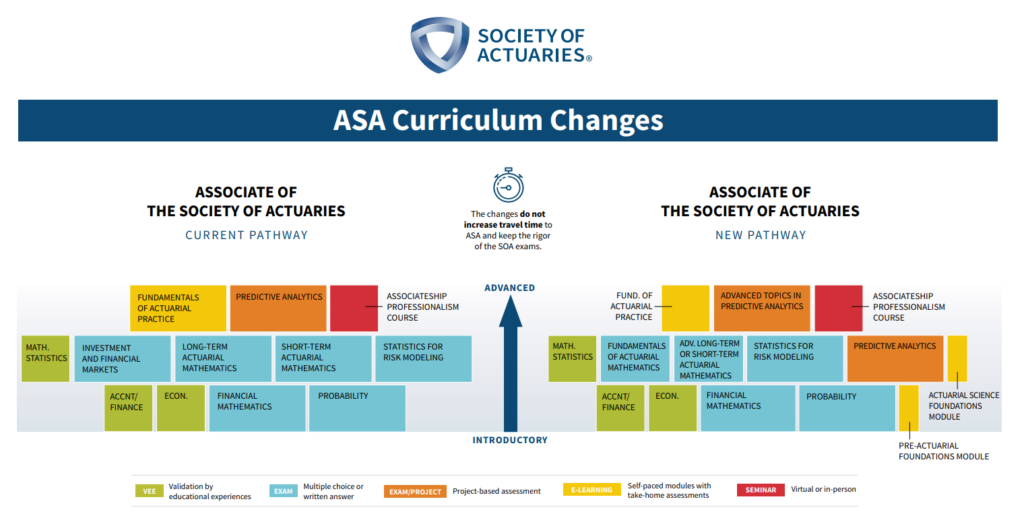

Graphic:

Excerpt:

Beginning in January 2022, pre-ASA candidates will also be able to begin work to earn new micro-credentials that recognize and demonstrate to employers their knowledge and skills gained along the pathway to ASA. These “milestone markers” will remain with candidates if they decide to leave the ASA pathway and are also applicable for those choosing to enter the pathway to only earn one or more micro-credential. All elements required to earn these micro-credentials are part of the ASA pathway and count in full toward earning the ASA and FSA designations.

These micro-credentials group together pathway components that represent distinct knowledge and skills to demonstrate the level of achievement candidates earn to employers, co-workers and their professional network. AQ/EQ and data science skills are driving changes to the ASA curriculum and will be incorporated into requirements for each micro-credential, allowing candidates the ability to demonstrate and build on those skills for their resume and jobs.

These micro-credentials do not make candidates qualified or “signing” actuaries; that work is reserved for those who earn the ASA and FSA designations. However, they do provide critical marks of candidates’ progress through the system and signal to employers the knowledge they’ve gained. We will be conducting an outreach program to employers to build awareness and support for the micro-credentials over the coming months.

Author(s): SOA

Publication Date: 12 July 2021

Publication Site: Society of Actuaries