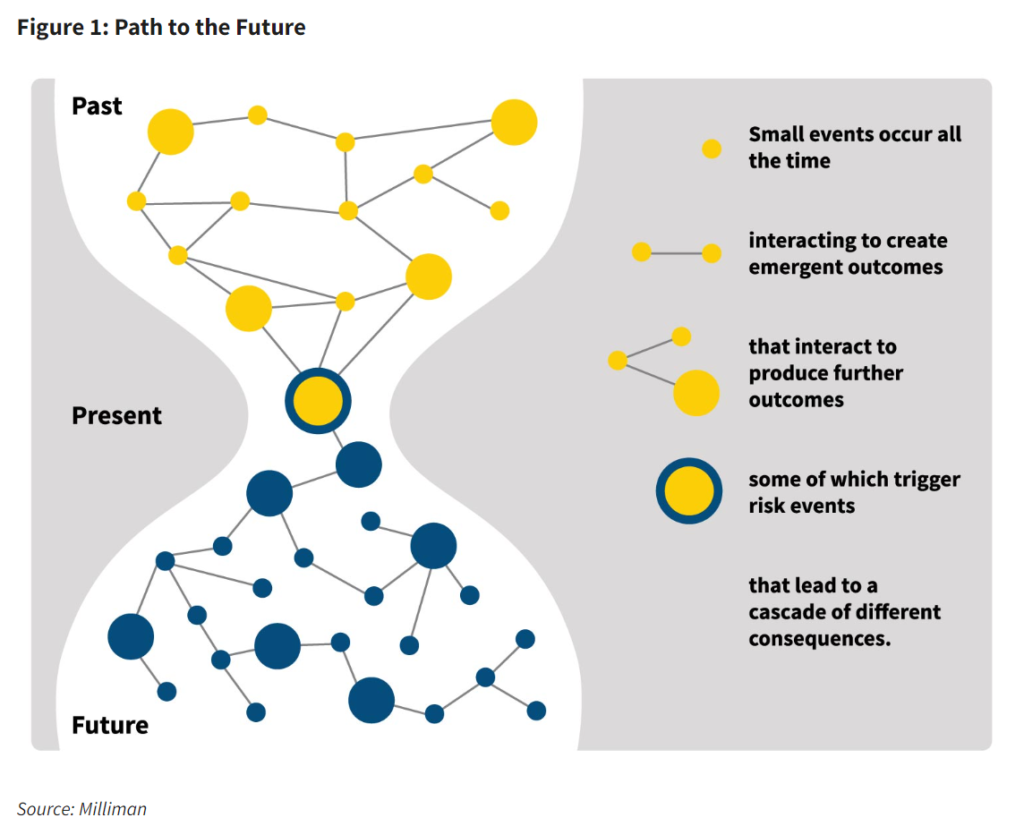

If we consider how risk events unfold in reality, they usually occur through a sequence of interacting factors (see Figure 1). For example: A control does not quite work as intended because the usual supervisor is not available, and coincidentally a staff member has unintended access to a system from which they are able to extract personal information. On any other day, those conditions might have been different and resulted in another outcome. The reality, therefore, is that risks emerge as a result of a complex series of interactions among a large number of factors, and small changes in conditions can lead to significantly different risk outcomes.

Risk events also often involve active participants who learn and adapt their behaviors accordingly. Cyber is a good example—the attacker generally is trying to outthink their adversary and stay one step ahead. All of this means that past performance is not necessarily a reliable predictor of the future. There are too many things that can be subtly different, leading to hugely different outcomes.

LIMRA, Reinsurance Group of America (RGA), the Society of Actuaries (SOA) Research Institute, and TAI have collaborated on an ongoing effort to analyze the impact of COVID-19 on the individual life insurance industry’s mortality experience and share the emerging results with the insurance industry and the public. The Individual Life COVID-19 Project Work Group (Work Group) was formed as a collaboration of LIMRA, RGA, the SOA Research Institute, and TAI to design, implement, and create the study and to produce and distribute a variety of analyses. This report is the fifth public release from this collaboration and contains the results of the study of excess mortality for individual life insurance to include the second quarter of 2021. Data from 31 companies representing approximately 72% of the industry face amount in force have been included in the analysis in this report. A total of 3.0 million death claims from individual life policies from 2015 through June 30, 2021 make up the basis of the analysis.

Highlights for the 2nd Quarter

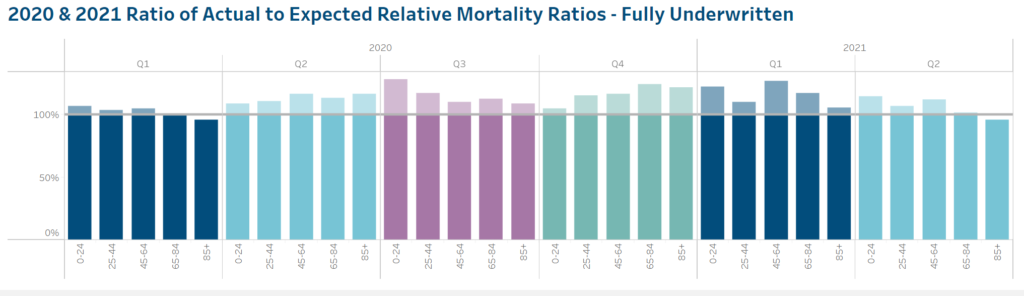

The second quarter of 2021 showed a significant realignment of the actual to expected relative mortality ratios, across many different cuts of the data.

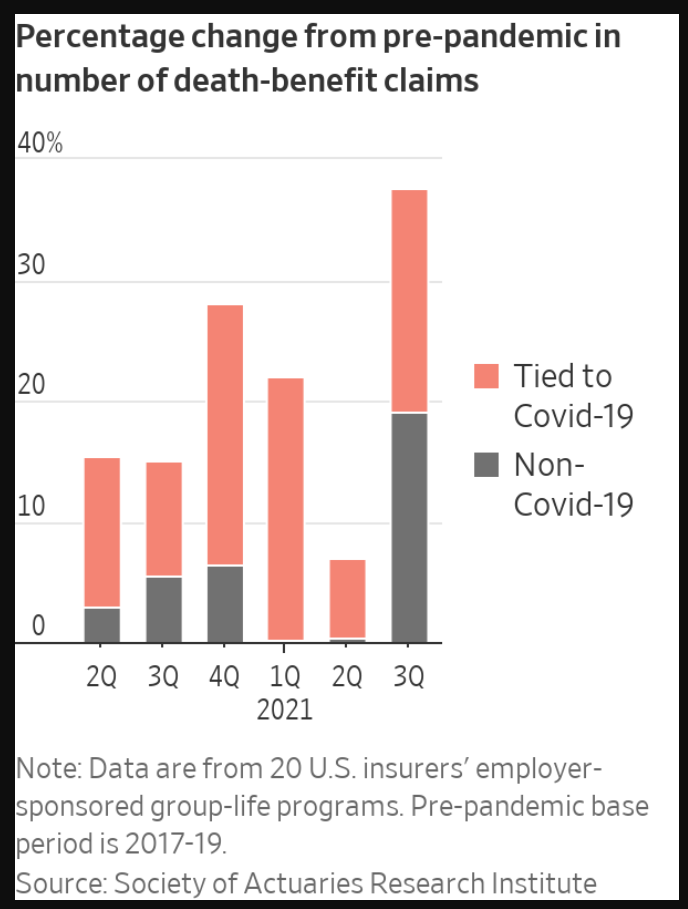

It is worth noting that the third quarter 2021 results will likely not be as favorable due to the impact of the COVID-19 Delta variant whose impact first started in July 2021 and peaked around mid- September

All age groups improved in the second quarter compared to the first quarter of 2021, but the improvement was more dramatic in the older ages. While the three age groups shown under age 65 were still significantly over the trend established by 2015-2019, the age 65-84 group was within the 95% confidence bands and the age 85+ group was significantly better than the 2015-2019 trend (p < 0.05).

Whereas the pandemic experience so far had showed substantial variations across different regions, this appears to have moderated during the 2nd quarter of 2022.

Author(s): Individual Life COVID-19 Project Work Group, SOA

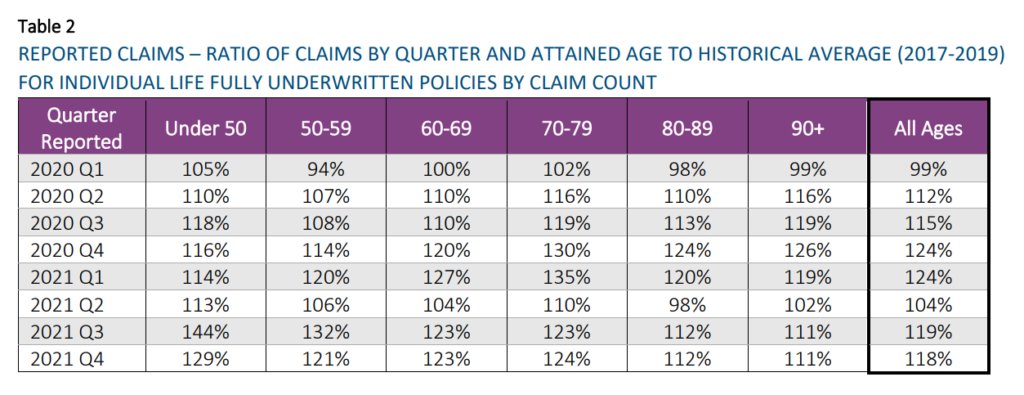

LIMRA, Reinsurance Group of America (RGA), the Society of Actuaries Research Institute (SOA), and TAI have collaborated on an ongoing effort to analyze the impact of COVID-19 on the individual life insurance industry’s mortality experience and share the emerging results with the insurance industry and the public. This report documents a high-level analysis of the claims that have been reported through December 31, 2021. The results presented here are based on data from 32 companies representing approximately 72% of the individual life insurance in force for the experience period of the study.

Author(s): Individual Life COVID-19 Project Work Group

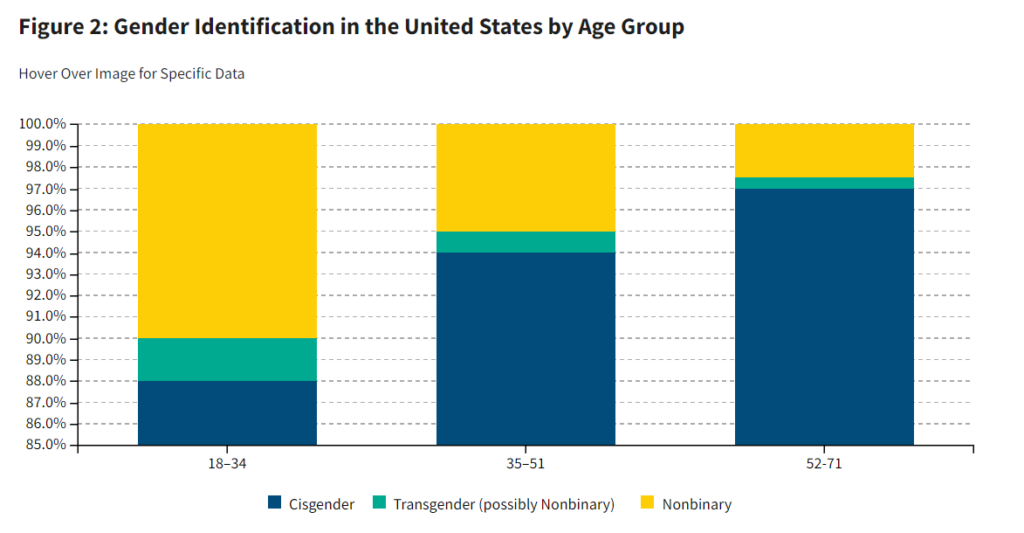

With nonbinary genders recognized on legal documents, customers are beginning to ask for forms and applications to include nonbinary options as well—so they’re not forced into a false selection. Even so, a person still could make an inaccurate selection. A customer falsely selecting a nonbinary gender is slightly less risky for the insurance company than selecting a false binary gender, as nonbinary rates are likely to fall somewhere between male and female to ensure they’re not discriminatory.

In the end, providing false information on an insurance application is fraudulent activity regardless of the question. Many of the states that include nonbinary gender markers on birth certificates and/or driver’s licenses already require the individual to sign an affidavit stating that they are not changing their gender marker for a fraudulent purpose. The benefits of including options for nonbinary customers and the potential for more accurate risk evaluations hopefully will outweigh a possible increase in fraudulent activity.

Growing popularity in no-medical-exam life insurance products has had one expected outcome: More life insurance policies with accelerated underwriting options available in the marketplace. For example, Policygenius offered just three accelerated underwriting options in 2020. In 2021, that number more than doubled to seven, and more options will likely be available in 2022.

Additionally, while such policies had historically only been available to applicants who were young and in good health, the competitive market has prompted more widespread availability. Now, applicants across all health classes can get no-medical-exam policies.

While no-medical-exam policies tend to be about the same cost as fully underwritten policies, applicants tend to favor them even when they are more expensive due to the convenience and expedited turnaround time.

“The losses we are seeing continue to be elevated over 2019 levels due at least in part, we believe, to the pandemic and the existence of either delayed or unavailable healthcare,” Globe Life finance chief Frank Svoboda told analysts and investors earlier this month.

Among the non-coronavirus-specific claims are deaths from heart and circulatory issues and neurological disorders, he said. “We anticipate that they’ll start to be less impactful over the course of 2022 but we do anticipate that we’ll still at least see some elevated levels throughout the year,” he said.

Primerica executives similarly cautioned in their fourth-quarter call about outsize numbers of non-Covid-19 deaths in 2022. “Some of these will be the result of delayed medical care or the increased incidence of societal-related issues, such as the increased prevalence of substance abuse,” Chief Financial Officer Alison Rand said in an email interview.

From early stages of the pandemic, many medical professionals have raised concerns about Americans’ untreated health problems, as Covid-19 put stress on the nation’s healthcare system.

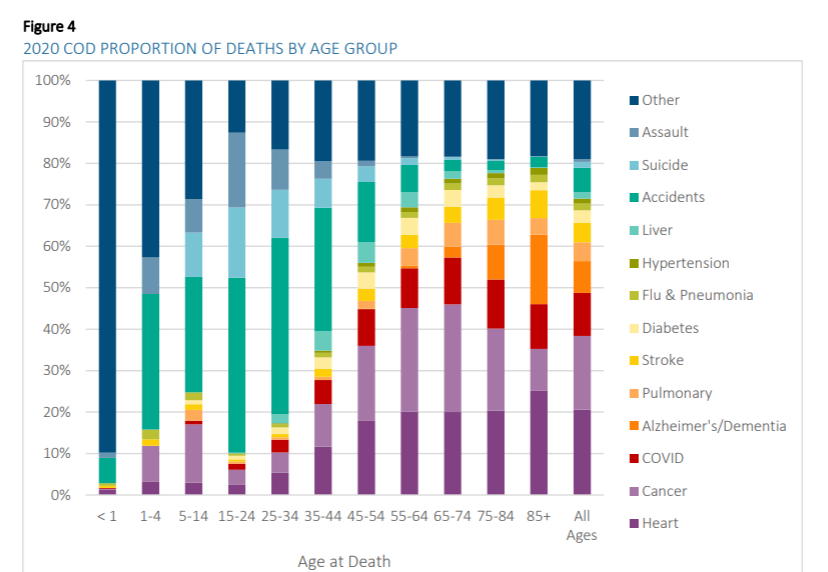

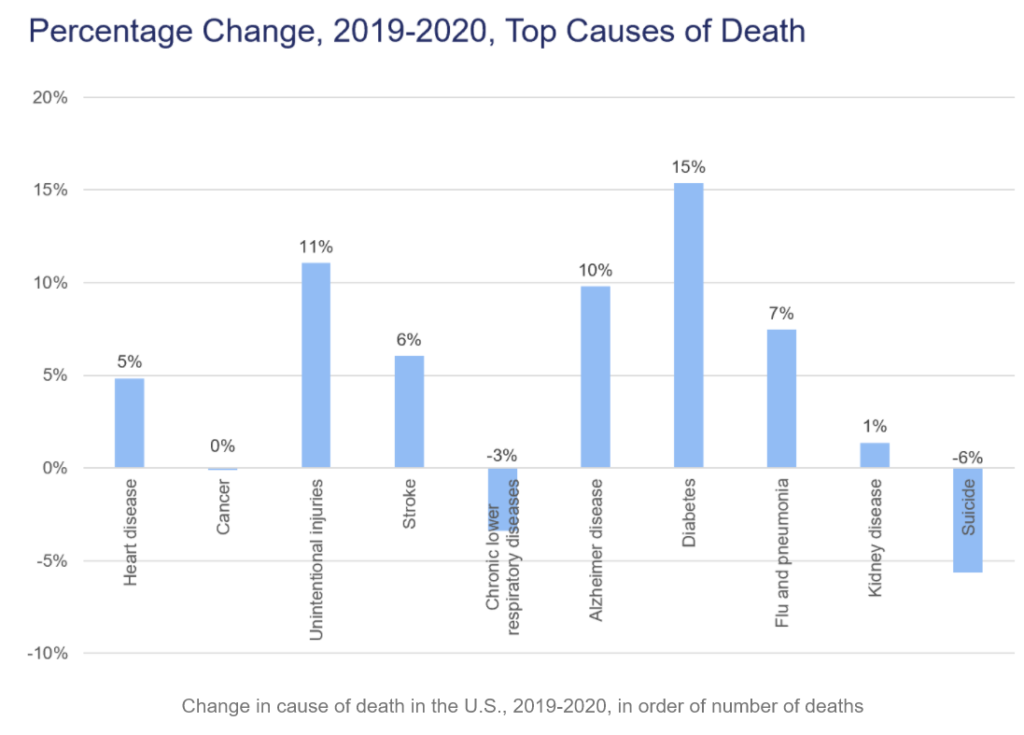

The overall age-adjusted mortality rate (both sexes) from all causes of death recorded the historically highest increase of published records dating back to 1900 of 16.8% in 2020, following a 1.2% decrease in 2019. The increase eclipsed the size of recent years’ annual volatility and exceeded the 11.7% increase in 1918 that occurred during the Spanish influenza pandemic. When COVID deaths are removed, all other CODs’ (Cause of Death) combined mortality increased by 4.9%, which was last exceeded by a 5.6% increase in 1936.

All other CODs featured in this report had increased 2020 mortality. In many instances, the single year mortality increases were the largest for the span of this report. Heart disease and Alzheimer’s/Dementia had 4.7% and 7.8% increases, respectively. Other physiological CODs with lower death rates had double-digit increases. Diabetes, liver and hypertension had increases of 14.9%, 16.0% and 13.3%, respectively. The external CODs of assaults and opioid overdoses had extreme increases at ages 15-24 of 35.9% and 61.2%, respectively.

Author(s):

Jerome Holman, FSA, MAAA, RJH Integrated Solutions, LLC Cynthia S. MacDonald, FSA, MAAA, Society of Actuaries Research Institute

(the answer: B — I’ll leave it to you to verify the calculations)

Excerpt:

Actuaries quantify risk. One of their riskiest endeavors is trying to become one.

Among people taking at least one exam from the Society of Actuaries—the field’s biggest U.S. credentialing body—15% eventually pass the multiple tests required to become an Associate, one of two designations allowing them to practice. Just 10% pass those and additional tests to become a Fellow, the group’s higher designation, which affords bigger responsibilities and salaries.

It’s such an arduous process that the number of test-takers has been declining in recent years, and the society is making changes to keep candidates from dropping out of the gantlet. It is also adding new “predictive analytics” tests to adjust to the massive amounts of data insurers now have.

There is no limit to how many times a candidate can take the tests. It took one man 50 years to become a Fellow, says Stuart Klugman, an official at the society. The society says a candidate typically takes seven to 10 years to become a Fellow. They must pass 10 exams plus other coursework and requirements.

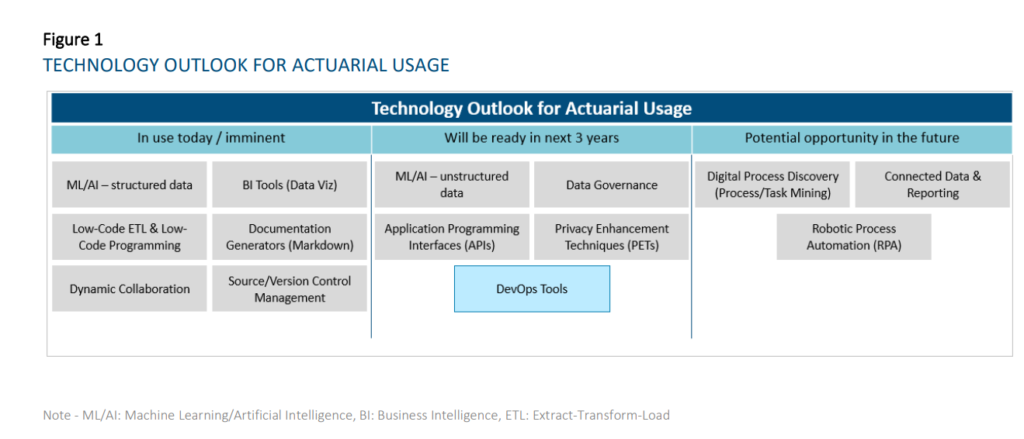

Technologies that have reached widespread adoption today: o Dynamic Collaboration Tools – e.g., Microsoft Teams, Slack, Miro – Most companies are now using this type of technology. Some are using the different functionalities (e.g., digital whiteboarding, project management tools, etc.) more fully than others at this time. • Technologies that are reaching early majority adoption today: o Business Intelligence Tools (Data Visualization component) – e.g., Tableau, Power BI — Most respondents have started their journey in using these tools, with many having implemented solutions. While a few respondents are lagging in its adoption, some companies have scaled applications of this technology to all actuaries. BI tools will change and accelerate the way actuaries diagnose results, understand results, and communicate insights to stakeholders. o ML/AI on structured data – e.g., R, Python – Most respondents have started their journey in using these techniques, but the level of maturity varies widely. The average maturity is beyond the piloting phase amongst our respondents. These are used for a wide range of applications in actuarial functions, including pricing business, modeling demand, performing experience studies, predicting lapses to support sales and marketing, producing individual claims reserves in P&C, supporting accelerated underwriting and portfolio scoring on inforce blocks. o Documentation Generators (Markdown) – e.g., R Markdown, Sphinx – Many respondents have started using these tools, but maturity level varies widely. The average maturity for those who have started amongst our respondents is beyond the piloting phase. As the use of R/Python becomes more prolific amongst actuaries, the ability to simultaneously generate documentation and reports for developed applications and processes will increase in importance. o Low-Code ETL and Low-Code Programming — e.g., Alteryx, Azure Data Factory – Amongst respondents who provided responses, most have started their journey in using these tools, but the level of maturity varies widely. The average maturity is beyond the piloting phase with our respondents. Low-code ETL tools will be useful where traditional ETL tools requiring IT support are not sufficient for business needs (e.g., too difficult to learn quickly for users or reviewers, ad-hoc processes) or where IT is not able to provision views of data quickly enough. o Source Control Management – e.g., Git, SVN – A sizeable proportion of the respondents are currently using these technologies. Amongst these respondents, solutions have already been implemented. These technologies will become more important in the context of maintaining code quality for programming-based models and tools such as those developed in R/Python. The value of the technology will be further enhanced with the adoption of DevOps practices and tools, which blur the lines between Development and Operations teams to accelerate the deployment of applications/programs

Author(s):

Nicole Cervi, Deloitte Arthur da Silva, FSA, ACIA, Deloitte Paul Downes, FIA, FCIA, Deloitte Marwah Khalid, Deloitte Chenyi Liu, Deloitte Prakash Rajgopal, Deloitte Jean-Yves Rioux, FSA, CERA, FCIA, Deloitte Thomas Smith, Deloitte Yvonne Zhang, FSA, FCIA, Deloitte

Work accomplished under the 2019 agreement between the Human Mortality Database (HMD) team and the Society of Actuaries (SOA) was divided between two main projects: 1) the continuous development of the United States Mortality Database (USMDB) and 2) the publication of cause-specific mortality series for selected HMD countries. Due to administrative delays at both the University of California, Berkeley, and the Society of Actuaries, work on these projects did not begin until July 2019. Furthermore, due to restriction in data access associated with the Covid-19 pandemic, a no-cost extension was requested by Magali Barbieri, the Principal Investigator for the projects, and accepted by the SOA to extend the project beyond the initial December 31, 2019 deadline.

Author(s): Magali Barbieri, Ph.D University of California-Berkeley

The long-term trend has been improvement for this cause of death, with it most obvious for the oldest age groups. This trend has been driven by improvement in medical treatment for the condition, but also due to the decrease in smoking rates… decades ago. Some causes of death have behavior that precedes the death by decades, which can get tricky to track for our top two causes of death: heart disease and cancer. Even so, smoking cigarettes has been a huge driver for both these causes, and made a large differentiator by sex and smoking status for a long time.

Do not put your career on hold. Continue to take (and hopefully pass) exams during the transition period.

Remember why you started taking actuarial exams in the first place. It was probably because you wanted to become an actuary or open doors to a variety of rewarding careers that combine business and the mathematical sciences. Unless your goals have changed, you should continue to take exams during the transition period. The SOA’s transition rules are usually very generous, so unless you repeatedly fail an exam that is being discontinued, you should not worry that the time spent studying for exams will be wasted.