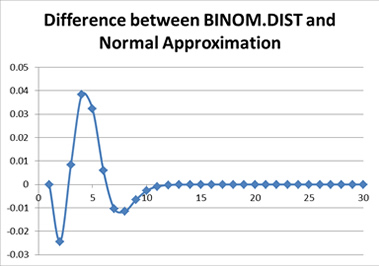

Before we get into the different approaches, why should you care about knowing multiple ways to calculate a distribution when we have a perfectly good symbolic formula that tells us the probability exactly?

As we shall soon see, having that formula gives us the illusion that we have the “exact” answer. We actually have to calculate the elements within. If you try calculating the binomial coefficients up front, you will notice they get very large, just as those powers of q get very small. In a system using floating point arithmetic, as Excel does, we may run into trouble with either underflow or overflow. Obviously, I picked a situation that would create just such troubles, by picking a somewhat large number of people and a somewhat low probability of death.

I am making no assumptions as to the specific use of the full distribution being made. It may be that one is attempting to calculate Value at Risk or Conditional Tail Expectation values. It may be that one is constructing stress scenarios. Most of the places where the following approximations fail are areas that are not necessarily of concern to actuaries, in general. In the following I will look at how each approximation behaves, and why one might choose that approach compared to others.

Under the old regime, the impairment was the incurred credit losses, in determining which only past events and current conditions are used. Credit losses were booked after a credit event had taken place, thus the name “incurred.” ECL and CECL require the incorporation of forward-looking information in addition to the past/current info in the calculation of impairment. There will be an allowance for credit losses since initial recognition regardless of the creditworthiness of the investment asset. The allowance can be perceived as the reserve or capital for credit risks. In practice, the allowance could be zero if there are no expected default losses for the instrument, US Treasury bonds, US Agency MBS, just to name a few.

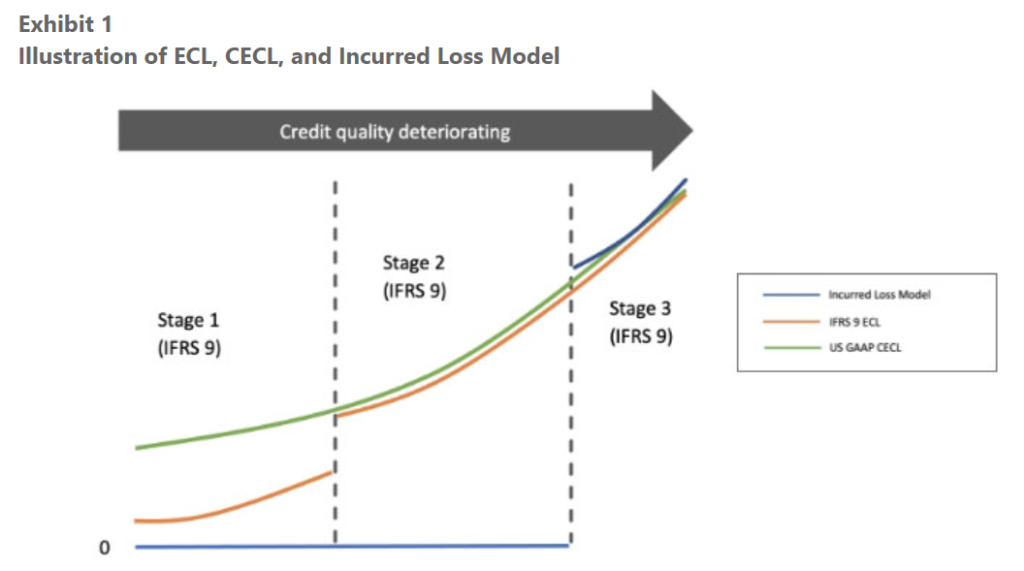

ECL under IFRS 9 is typically calculated as a probability weighted estimate of the present value of cash shortfalls over the expected life of the financial instrument. It Is an unbiased best estimate with all cash shortfalls taking into consideration the collaterals or other credit enhancement. Four typical parameters underlying its calculation are: Probability of default (PD), loss given default (LGD, i.e., 1-Recovery Rate), exposure at default (EAD) and discounting factor (DF). Prepayments, usage given default (UGD) and other parameters can also play a role in the calculations. In the general approach the loss allowance for a financial instrument is 12-month ECL regardless of credit risk at the reporting date, unless there has been a significant increase in credit risk since initial recognition: The PD is only considered for the next 12 months while the cash shortfalls are predicted over the full lifetime; as the creditworthiness deteriorates significantly, the loss allowance is increased to full lifetime ECL in Stage 2, which should always precede stage 3 (credit impairment). Even without change of stages, any credit condition changes should be flowing into the credit loss allowance via updates in some of the underlying parameters. Exhibit 1 has an illustrative comparison between ECL, CECL, and incurred loss model.

CECL is similar to ECL except FASBs doesn’t have so-called staging as IFRS 9, which requires that only 12-month ECL is calculated in stage 1 (in the general model). In other words, CECL requires a full lifetime ECL from Day 1. There are also other differences: IFRS 9 requires certain consideration of time value of money, multiple scenarios, etc., in measurement of ECL while US GAAP CECL doesn’t.

Under US GAAP, different from CECL, currently the impairment for AFS assets, while also recorded as an allowance (with a couple exceptions), is only needed for those whose fair value is less than the amortized cost. Once it is triggered, the credit losses are then measured as the excess of the amortized cost basis over the probability weighted estimate of the present value of cash flows expected to be collected. Only the fair value change related to credit is considered in the calculation of AFS impairment. The quantitative calculation behind the probability weighted best estimate is like CECL/ECL. Both can use discounted cash flow methods with parameters such as PD although one is calculating expected cash shortfalls directly in CECL and the other is calculating the expected collectible cash payments and then is used to back out the impairment.

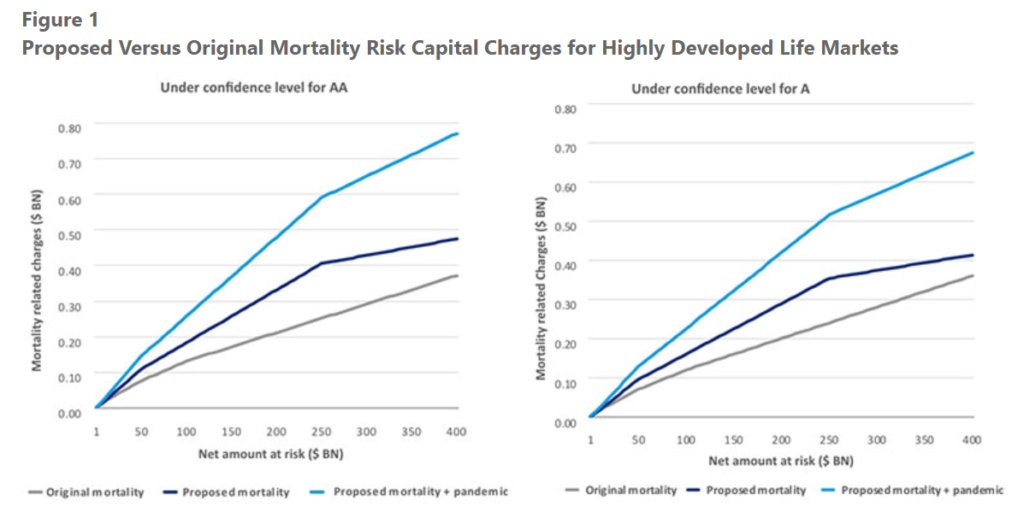

Life technical risks measure the possible losses from deviations from the best estimate assumptions relating to life expectancy, policyholder behavior, and expenses. The life technical risks are captured through mortality, longevity, morbidity, and other risks. The methodology for calculating the capital adequacy for these four risk categories remains unchanged under the proposed method, apart from the recalibration of capital charges or the consolidation of defining categories within each risk. Comparing to the current GAAP based model, charges have materially increased across all categories partly due to higher confidence intervals, with notable exceptions of longevity risk, with reduced charges across all stress levels (changes applicable to U.S. life insurers are illustrated in Tables A2 to A5 in the Appendix linked at the end of this article). Please note that S&P’s current capital model under U.S. statutory basis does not have an explicit longevity risk charge. However, this article focuses on comparison to current GAAP capital model[1] that is closer to the new capital methodology framework.

For mortality risk, lower rates are charged for smaller exposures (net amount at risk (NAR) $5 billion or less) with the consolidation of size categories, but higher rates are charged for NAR between $5 billion and $250 billion, with an average increase of 49 percent for businesses under $400 billion NAR. A new pandemic risk charge (Table A3 in the Appendix linked at the end of this article) will further increase mortality related risk charges to be 109 percent higher than original mortality charges under confidence level for company rating of AA, and 93 percent higher for confidence level for company rating of A, respectively, on average (Figure 1). The disability risk charge rates increased moderately for most products, across all eight product types such that the increase of disability premium risk charges is 6 percent under confidence level for AA, and 2 percent for A, respectively. In addition, the proposed model introduced a new charge on disability claims reserve, ranging from 13.7 percent of total disability claims reserves for AAA, to 9.6 percent for BBB. However, the proposed model provides lower capital charge rates in longevity risk and lapse risk.

Author(s): Yiru (Eve) Sun, John Choi, and Seong-Weon Park

Publication Date: September 2022

Publication Site: Financial Reporting newsletter of the SOA

Under LDTI, DAC amortization will no longer obscure the relationship between direct and ceded accounting. It is now possible to align ceded accounting with direct, without any noise from DAC amortization. With poor alignment, distortions within the results reported to management and financial statement users will be different, sometimes greater than before. Whether the goal is to improve reporting or to avoid making it worse, a fresh look can help.

Most of the approaches that have been used to account for UL reinsurance can still be used. One exception is the implicit approach where, in lieu of explicit accounting for reinsurance, the gross profits used to amortize DAC were adjusted to be net of reinsurance. With the elimination of gross profits as an amortization base, this approach no longer has meaning.

For surviving approaches, it is now easier to evaluate their effectiveness in presenting the economic protection provided by reinsurance.

In this article, I begin an evaluation by examining the fundamentals of accounting for the insurance element of universal life. After that, I consider the economic protection provided by reinsurance and look for an ideal—a way to effectively account for that protection.

In a second article to be published later this year, I’ll evaluate several reinsurance approaches in terms of noise from missing the ideal, then end with some thoughts on what might be done to eliminate noise.

The focus of both articles is on the insurance element. Accounting for the deposit element, embedded derivatives, and market risk benefits is beyond the scope of these articles. Also outside of scope is the requirement, in Accounting Standards Codification (ASC) Topic 326, to recognize a current estimate of credit losses from the failure of a reinsurer to reimburse reinsured benefits.

Author(s): Steve Malerich

Publication Date: Sept 2022

Publication Site: Financial Reporting newsletter, SOA

Much of retirement planning focuses on financial, investment, and estate planning needs. Earlier research, such as the SOA’s Retirement Health & Happiness brief, showcases how this retirement planning overlooks some challenges of late-in-life retirees.

Retirees have access to more than 200,000 personal finance professionals, 10,000 senior centers, and approximately 28,000 assisted living facilities. Still, do retirees have all the information they need to make critical decisions throughout retirement, particularly in the latter stages of retirement?

In collaboration with Financial Finesse, the SOA Aging and Retirement Strategic Research Program prepared this guide as a resource to help older retirees and those who assist them. This guide will help the reader ask impactful questions to make informed decisions.

Author(s): SOA Aging and Retirement Strategic Research Program

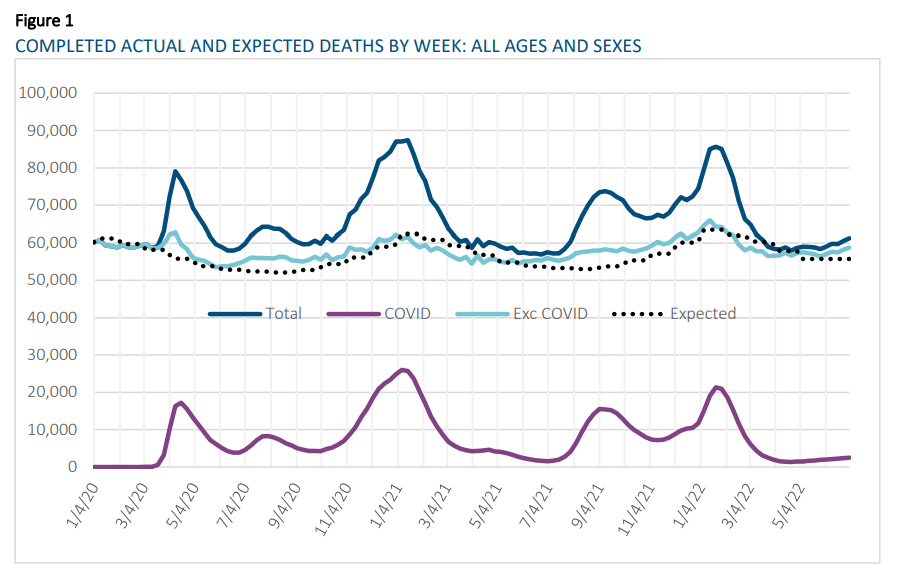

The data used for this analysis was provided by the CDC as of August 17, 2022 and includes incurred deaths by week, beginning on December 29, 2019 and going through July 2, 2022. For 2020, the CDC defines Week 1 as ranging from December 29, 2019 through January 4, 2020 and Week 52 as ranging from December 19, 2020 through December 26, 2020, so when reporting on 2020 results, this convention is used. The year 2021 begins on December 27, 2020 and runs through January 2, 2022. For the purposes of this analysis, the start of the COVID-19 active period is March 22, 2020. Due to the delay in reporting, the actual deaths have been completed based on factors that vary by age and sex. These are shown below along with the expectations that are based on the five-year trend after adjusting for seasonality.

These data are as of August 17, 2022 and exclude deaths that occurred after July 2, 2022. Figure 1 shows that, for most months, the total A/E ratio is much greater than 100%, while the A/E ratio excluding COVID19 deaths is also greater than 100% by a few percent.

Author(s): Rick Leavitt, ASA, MAAA

Publication Date: August 2022

Publication Site: Society of Actuaries Research Institute

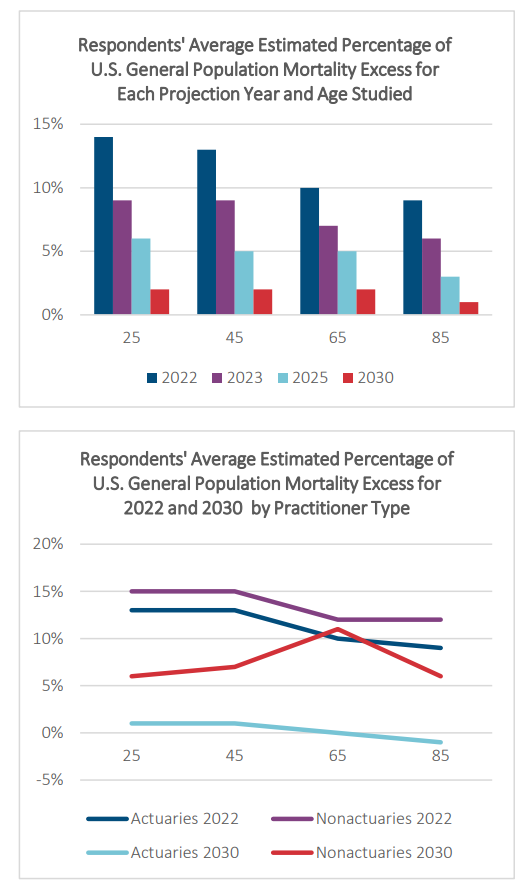

Excess mortality is expected to occur for all years studied with amounts varying by year and age. Although the largest mortality excess numbers for the U.S. general population are foreseen for 2022, excess mortality is expected to decline each year so that by 2030, excess mortality numbers are nearing expected levels. For 2030, mortality is projected to be 2% higher than expected for all ages except age 85. At this age, 2030 projected mortality is estimated to be 1% higher than expected.

Based on the average of the participants, generally, the amount of mortality excess is anticipated to be highest at the younger ages. For example, for 2022, projected mortality is anticipated to be 14% higher compared to expected levels for age 25, 13% higher for age 45, and 10% higher for ages 65 and 85.

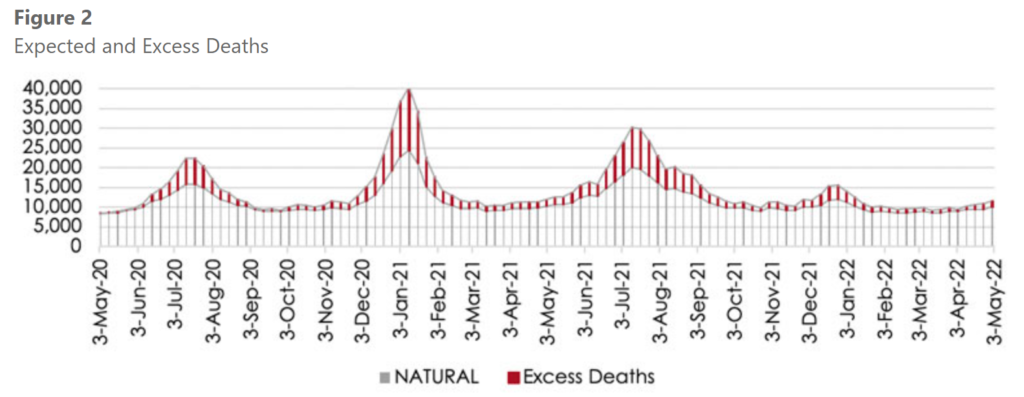

The impact of Covid-19 in South Africa in terms of excess deaths was substantial, when considering the reported excess deaths as published by the South African Medical Research Council (SAMRC).[4] Please note that in this article we will not further consider whether all excess deaths can be directly attributed to Covid-19, however, as per the article “Correlation of Excess Natural Deaths with Other Measures of the Covid-19 Pandemic in South Africa,”[5] it is estimated that 85 percent to 95 percent of excess natural deaths are attributable to Covid-19.

Based on the SAMRC excess deaths, taking the expected plus excess deaths as Actual and expected natural deaths as per their methodology as Expected, we observe an Actual versus Expected (AvE) ratio of 116 percent in 2020, a ratio of 131 percent in 2021, and a ratio of 113 percent in 2022 up to May 1. When we look at the AvE for each wave, we can see that the 2nd wave (predominantly Beta variant) and the 3rd wave (predominantly Delta variant), had the most severe impact on the general population (see figure 2 and figure 3)

Living benefit riders to life insurance policies (also known as ‘combo’ or ‘hybrid’ policies) have become a core component of life insurance sales strategy. LIMRA reported that in 2020 “Combination products represented 24 percent of life insurance sales based on total premium.”[1] Concurrently, the long-term care insurance (LTCI) industry reached an inflection point when more LTCI (and chronic illness) benefits were sold through hybrid products than from standalone LTCI coverage.

On the spectrum of life and LTCI hybrid policies, the richest of these provide coverage of LTCI first through accelerating the policy’s death benefit, and then by providing extended LTCI benefits for many more years. There are a handful of individual and worksite insurers who sell these rich hybrid policies. On the other end of this spectrum are acceleration-only riders to life insurance policies. These riders provide policyholders the opportunity to receive a portion of the policy’s death benefit in advance, under certain conditions. Some of these riders do not cover qualified LTCI, but instead cover ‘chronic illness,’ which has a similar benefit trigger but is not formally LTCI.

This article outlines industry practice and consideration for pricing these acceleration-only policies. The National Association of Insurance Commissioners (NAIC) Model Regulation #620 addresses accelerated death benefit riders to life insurance policies.[2] Model Regulation #620 outlines three financing methods for accelerated death benefit riders which we describe in this article. The Interstate Insurance Product Regulation Commission (the IIPRC, or the “Compact”) adopted standards for some of these riders in the Additional Standards for Accelerated Death Benefits (IIPRC-L-08-LB-I-AD-3).[3] For companies filing chronic illness, critical illness, and terminal illness products in the Compact, these standards define—among other items—the form and actuarial submission requirements and benefit design options for accelerated death benefit riders. If a company is filing an acceleration rider for a qualified LTCI benefit, that product would be subject to the IIPRC individual LTC insurance standards.

Different mortality projection methodologies are utilized by actuaries across applications and practice areas. As a result, the SOA’s Longevity Advisory Group (“Advisory Group”) developed a single framework to serve as a consistent base for practitioners in projecting mortality improvement. The Mortality Improvement Model, MIM-2021-v2, Tools and User Guides, compose the consistent approach and are defined below.

A report describing MIM-2021-v2 which summarizes the evolution of MIM-2021-v2; provides an overview of MIM-2021-v2; presents considerations for applying mortality assumptions in the model; and outlines issues the Advisory Group is currently considering for future model enhancements.

A status report of the items listed in Section V of Developing a Consistent Framework for Mortality Improvement. This report advises practitioners about subsequent research and analysis conducted by the Advisory Group regarding these items.

An Excel-based tool, MIM-2021-v2 Application Tool, and user guide, MIM-2021-v2 Application Tool User Guide, for practitioners to construct sets of mortality improvement rates under this framework for specific applications.

An Excel-based tool, MIM-2021-v2 Data Analysis Tool, and user guide, MIM-2021-v2 Data Analysis Tool User Guide, for practitioners to analyze the historical data sets included in the MIM-2021-v2 Application Tool.

The Longevity Advisory Group is planning to update the framework annually as new data and enhancements become available. MIM-2021-v2 is the first revision since the initial release in April 2021. This version uses the same underpinning as the initial MIM-2021 release but has been refreshed to include another year of historical U.S. population mortality data as well as more user flexibility and functionality to replicate RPEC’s MP-2021 and O2-2021 scales.

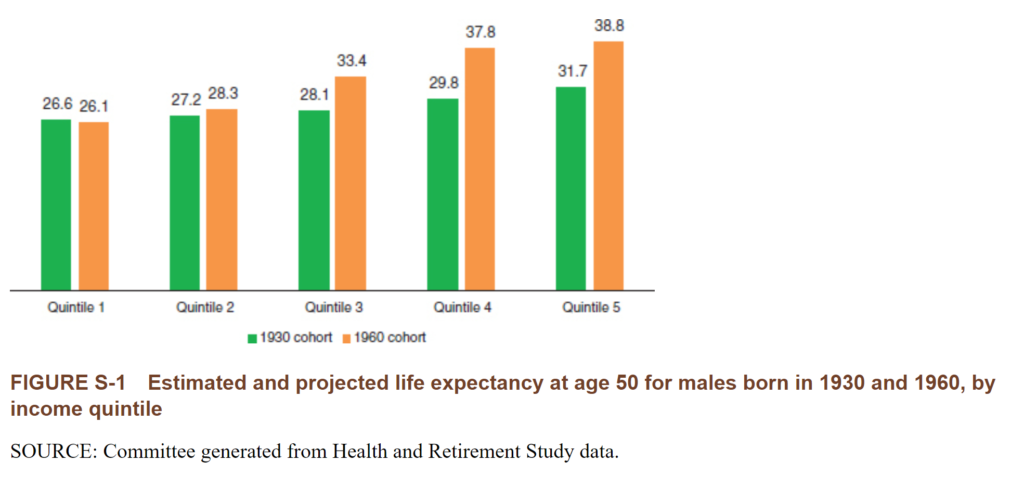

Many recent studies find the life expectancy gap is growing. By how much depends on how and when it’s measured. In 2014, the Congressional Budget Office (CBO) calculated that a 65-yearold man in the upper quintile (fifth) of life earnings could be expected to live more than three years longer than a similar man in the lowest quintile. By 2039, the difference would double to six years.

In a 2015 report, the National Academy of Sciences compared the 1930 and 1960 birth cohorts and found that life expectancy for the bottom quintile of men at age 50 decreased slightly to 26.1 years over the 30-year period. Meanwhile, life expectancy rose for men age 50 in higher-income quintiles. As shown in Figure 1, the life expectancy gap between the bottom (quintile 1) and top fifth of the income distribution widened from 5.1 to 12.7 years. In 2016, a Brookings study found, for men born in 1940, those in the lowest income decile at age 50 could expect to live to be about 76 years old compared with 88 years for the highest income decile. Another research team, led by Raj Chetty, found that disparity in longevity continued to increase over 2001–2014; the average gap between the bottom and top 1 percent was 14.6 years for men and 10.1 years for women.