Link: https://www.ineteconomics.org/perspectives/blog/meet-the-grinch-stealing-the-future-of-gen-y-and-z

Excerpt:

There’s one threat that gets far less attention, which has been impacting American workers since the 1970s: wages that just don’t keep up, despite increased productivity. Social Security was designed for wages that rise with inflation – but that’s not happening. In an interview with the Institute for New Economic Thinking, Eric Laursen, author of The People’s Pension: The Struggle to Defend Social Security Since Reagan, breaks down how the program works, why wage stagnation represents a mounting threat, and what can be done to strengthen and update the program for the 21stcentury.

Lynn Parramore: Social Security has been America’s most successful retirement program for the last 87 years. Yet the public is constantly hearing that the program is going to “run out of money.” Is that actually true? Can Social Security actually go bankrupt?

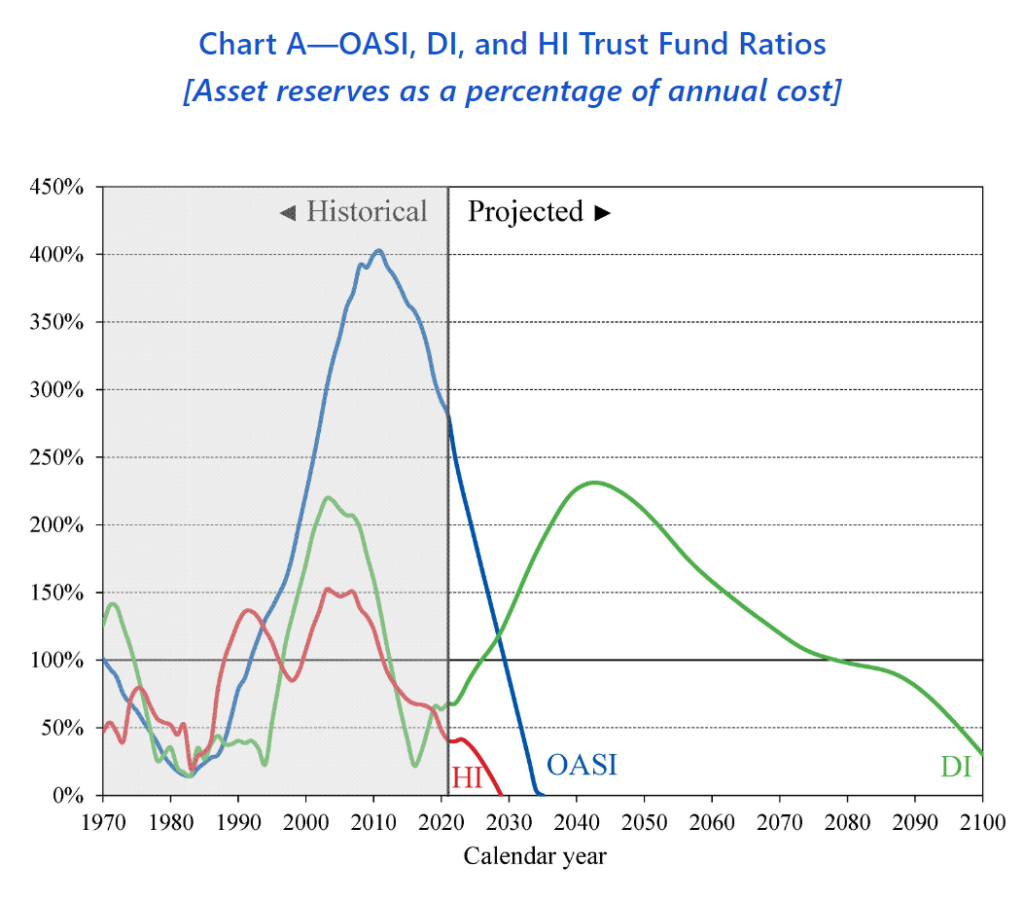

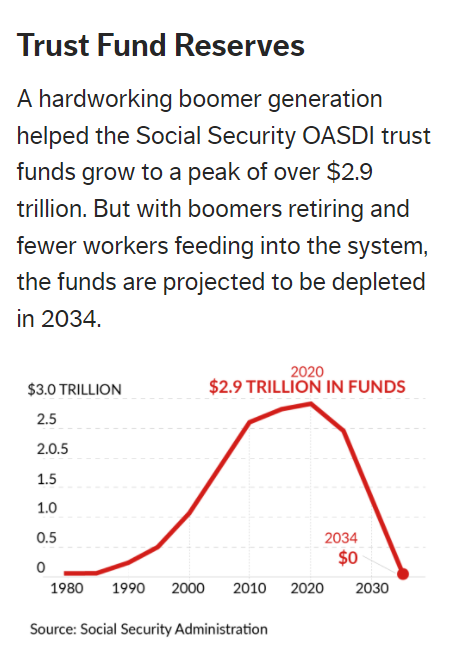

Eric Laursen: No, and the word bankrupt is just about a complete misnomer when it comes to Social Security. The program is funded by contributions that participants and their employers make through their paychecks. It’s also backed by a Trust Fund which is accumulated over time.

That Trust Fund is dwindling now, and it’s expected to run out of money in the early 2030s. But Social Security can’t actually go bankrupt. If the situation arises where there is not enough money either in the Trust Fund or coming through from contributions to fund current benefits, then those benefits can’t be paid, perhaps as much as 25%. In that case, Congress would be faced with a choice to either cut benefits or increase contributions.

There’s a lot of pressure from people who want to cut Social Security to do it now rather than waiting for that point in the future, because at that point, Congress would be under a lot of pressure to make good on what people have been promised.

….

LP: What would you do to make sure that Social Security is protected and remains strong? Does it need to be modernized in some ways to keep it effective?

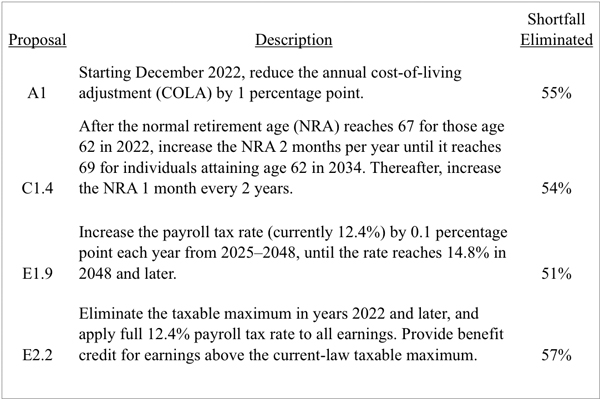

EL: There are a number of things that can be done. One is to raise the cap. More of income beyond the $147,000 threshold needs to be taxed for payroll tax purposes. Another thing that can be done is passing the Social Security Expansion Act that Sanders, Elizabeth Warren, and others have backed. There is a special minimum benefit for Social Security recipients that’s aimed at keeping people who have really low incomes during their lifetimes above the poverty level, and that needs to be improved. That’s not asking a lot. It should be done.

You can also change the rules for wealthy people. One of the differences between now and 40 years ago is that people in the really high income brackets get much more of their income from investments, stock options, and other business holdings than they do from salaries and wages. We need to figure out a formula for applying the payroll tax to at least some of that investment income – like capital gains and so forth. Definitely, the CPI-E needs to be instituted. There should be an expansion of benefits across the board for Social Security benefits. We need the CPI-E at a base level that’s more reasonable. Another thing I think is important: one of the changes that happened in ’83 that was really bad was that Social Security survivor benefits were ended for children of deceased or disabled workers above the age of 18. It used to be that you could get those until 22 and they would help you to go to college. That was abolished. It would be a very good thing if that could be reinstated so that more people have some level of security to pursue higher education.

Author(s): Lynn Parramore

Publication Date: 20 Dec 2022

Publication Site: Institute for New Economic Thinking