As the Russian invasion of Ukraine continues, the AFSCME union in Illinois has asked the state board of investment to divest all holdings in assets tied to Russia.

A letter from the executive director of AFSCME Council 31 was sent to Illinois State Board of Investment Chairman Terrence Healy. Council 31 Executive Director Roberta Lynch referred to the invasion as a “genocidal slaughter of civilians.”

….

The state investment board governs investment policy for the State Employees Retirement System, as well as to other Illinois public pension funds that AFSCME members participate in.

#4. Copper USGS data shows that Russia produced 920,000 tonnes of refined copper in 2021, about 3.5% of the world total, out of which Nornickel produced 406,841 tonnes.

UMMC and Russian Copper Company are the other two major producers, with Asia and Europe being Russia’s key export markets.

Prices of green metals, including copper, are projected to reach historical peaks for an unprecedented, sustained period in a net-zero emissions scenario. Copper prices are sitting at all-time highs thanks to surging demand, especially in developed countries, with increasing usage in electric vehicles and wind farms, solar panels and the power grid, combined with tight supply.

Benchmark copper prices on the London Metal Exchange are currently sitting at $10,100 per ton, not far removed from its May 2021 all-time high of 10,724.50 per ton.

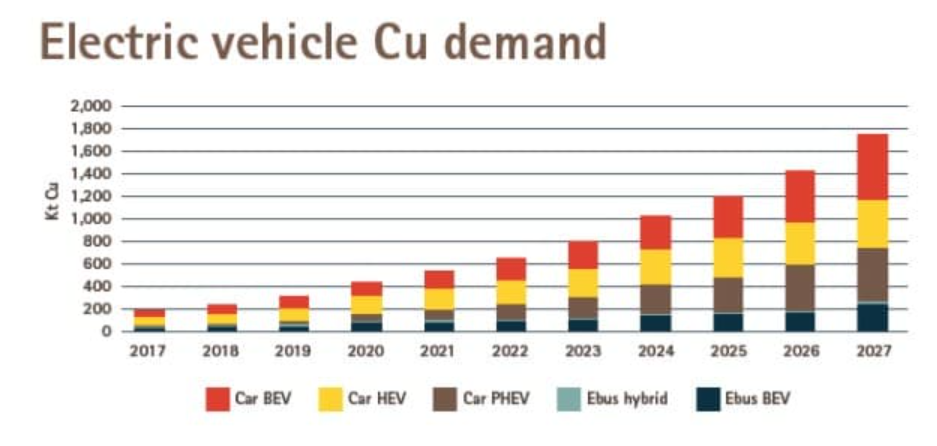

Copper is being billed as the new oil, with the ‘green’ shift in the post-COVID economy supporting higher demand for copper and other base metals since EVs use about 4x more copper than gasoline-powered vehicles. The International Copper Association estimates that the rapid rise of EVs will raise copper demand in EVs from 185,000 tonnes in 2017 to 1.74 million tonnes by 2027.

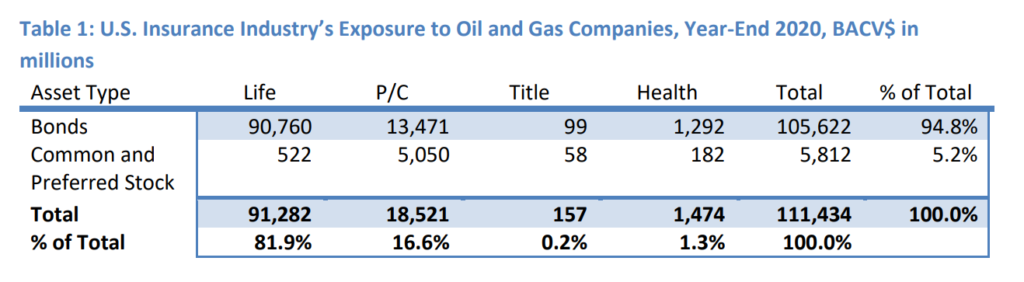

Table 1 identifies the year-end 2020 bond, common stock and preferred stock exposure of the U.S. insurance industry to oil and gas companies. The industry’s $111 billion book/adjusted carrying value (BACV) exposure represented approximately 1.5% of the industry’s total cash and invested assets as of year-end 2020. Oil and gas companies will benefit from the rise in oil prices, and they are currently in a much better financial position than during 2020 when Brent crude prices briefly fell below $10 per barrel and remained depressed relative to historical levels due to lower demand resulting from the effects of the COVID-19 pandemic.

Author(s): Michele Wong, Jennifer Johnson and Jean-Baptiste Carelus

A growing number of state governments are looking at dumping public pension fund investments they have in Russia in response to the country’s invasion of Ukraine.

California, Connecticut, Colorado and Illinois are among the states where officials are looking to do so.

While the divestment efforts are meant as a show of solidarity with Ukraine and a rebuke of Russia’s attack, the amount of money potentially affected compared to the overall size of the nation’s public pension assets is relatively small. And some of the actions would involve legislation and other measures that aren’t yet finalized.

Risks with investing in Russia that preceded the war, like corruption, and shortfalls with rule of law and transparency, mean that many pension managers would have been leery of investing heavily in the country in recent years.

“For most public pension funds in the U.S., Russia exposure is probably quite modest,” Ash Williams, former executive director and chief investment officer for Florida State Board of Administration, noted during an interview at an event the National Institute on Retirement Security held in Washington, D.C. on Tuesday.

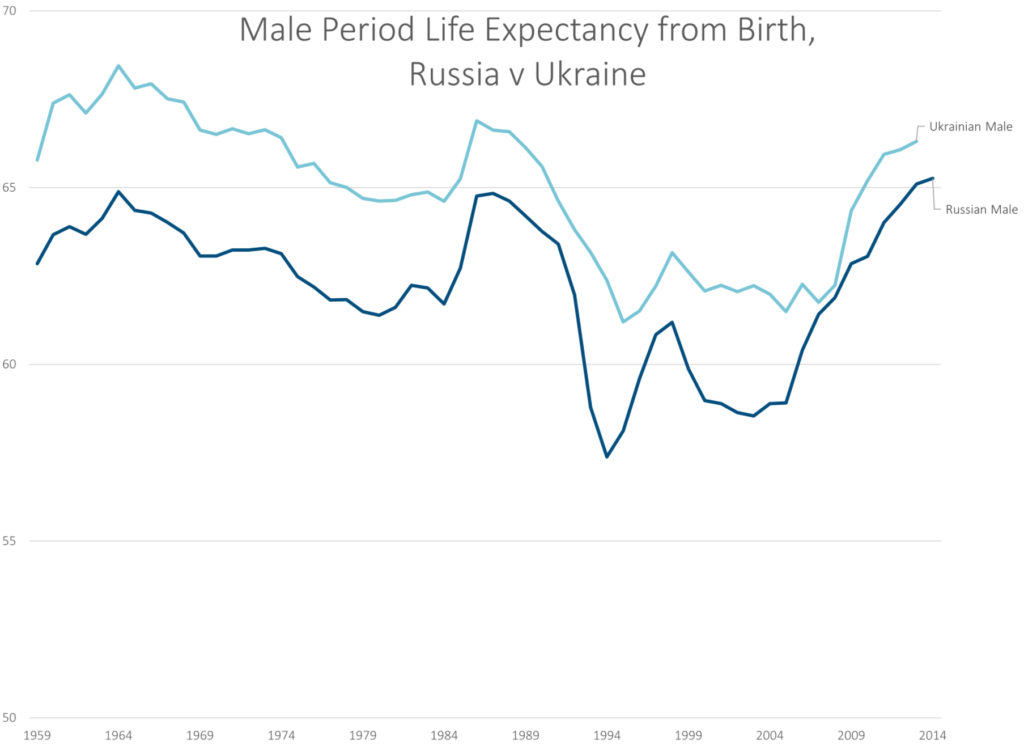

These are awful trends. There’s nothing to caveat. Yes, Ukraine’s life expectancy is a little bit higher, but these numbers are awful, and yes, there was a cratering of male life expectancy after the collapse of the Soviet Union.

I will note that there was a general slide from the early 1960s until the early 1980s… a run-up for some reason (falsifying data?), and then absolute cratering. That’s just hideous.

Dropping about 5 years over a 5-year period is a horrible decrease.

There has been a recovery since 2004, but that life expectancy is still very low compared to other European countries, even other Eastern European countries, as we’ll see below.

The timing on Wednesday was impeccable. I was looking at the price of oil, which was up four percent that day and about to pass $100/barrel. Energy stocks were up over one percent despite a horrible day for the rest of the market.

So, with inflation raging, gasoline moving towards $4.00/gallon and Russia murdering Ukrainians with the help of American oil purchases, Chicagoans can take comfort knowing that the city will refuse to invest in oil and other fossil fuel production and thereby “will be sending a message that Chicago is permanently leaving dirty energy in the past and welcoming a clean energy future for generations to come.”

That’s from Chicago Treasurer Melissa Conyears-Ervin. She and members of the City Council, with Mayor Lori Lightfoot’s support, are pushing for an ordinance to mandate that the city divest its funds from fossil fuel companies, as Crain’s reported.

In fact Conyears-Ervin had already made oil and gas divestment office policy. The new ordinance would make the change permanent going forward. Her office has already removed $70 million in fossil fuel-associated bonds from the city’s portfolio, she says.

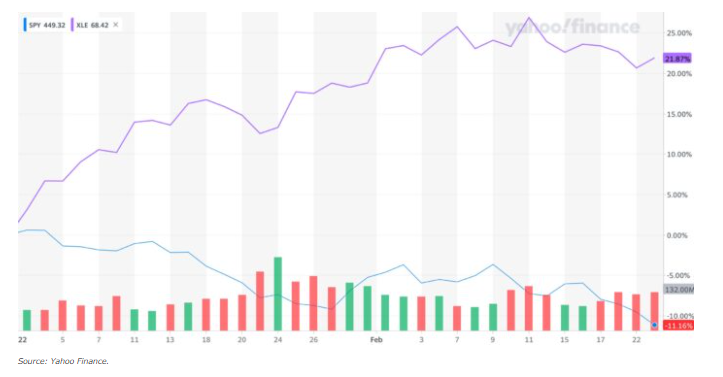

How wise has it been lately to be shunning fossil fuel investments? Here’s a chart comparing performance year-to-date of the S&P 500 to XLE, an ETF basket of mostly oil and gas companies. While the market in general is down some 10% the oil and gas stocks are up over 21%.

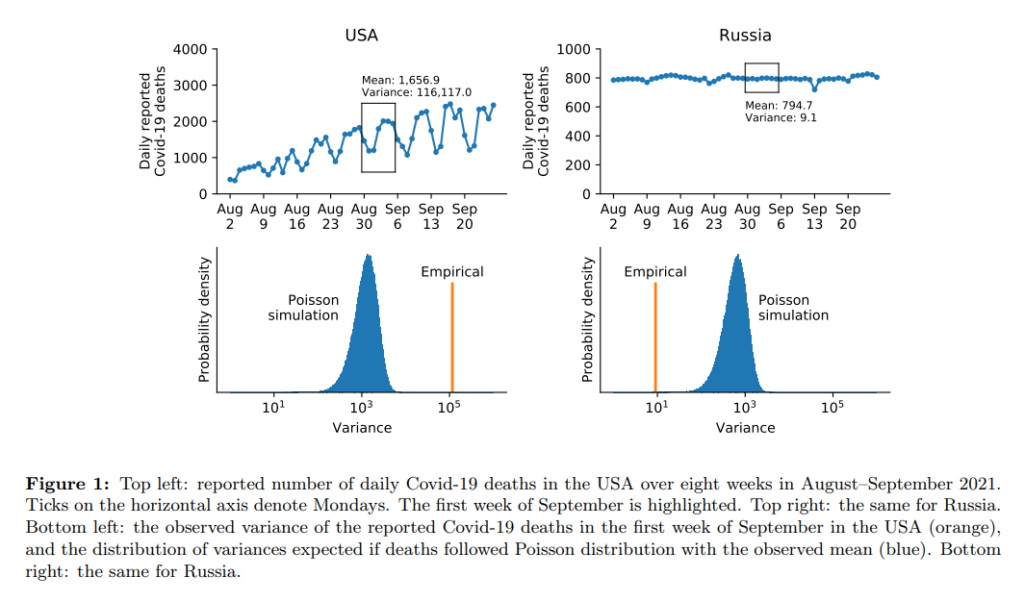

We suggest a statistical test for underdispersion in the reported Covid-19 case and death numbers, compared to the variance expected under the Poisson distribution. Screening all countries in the World Health Organization (WHO) dataset for evidence of underdispersion yields 21 country with statistically significant underdispersion. Most of the countries in this list are known, based on the excess mortality data, to strongly undercount Covid deaths. We argue that Poisson underdispersion provides a simple and useful test to detect reporting anomalies and highlight unreliable data.

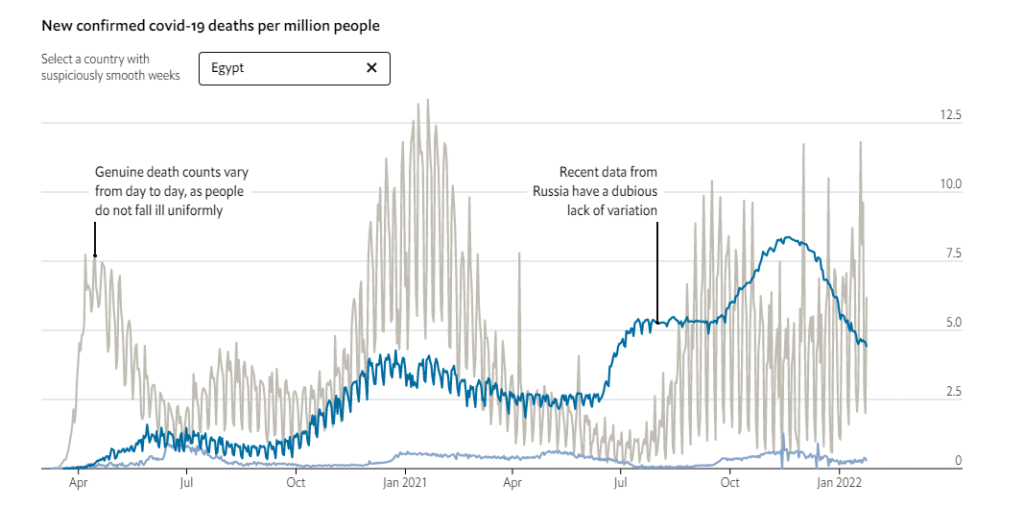

Irregular statistical variation has proven a powerful forensic tool for detecting possible fraud in academic research, accounting statements and election tallies. Now similar techniques are helping to find a new subgenre of faked numbers: covid-19 death tolls.

That is the conclusion of a new study to be published in Significance, a statistics magazine, by the researcher Dmitry Kobak. Mr Kobak has a penchant for such studies—he previously demonstrated fraud in Russian elections based on anomalous tallies from polling stations. His latest study examines how reported death tolls vary over time. He finds that this variance is suspiciously low in a clutch of countries—almost exclusively those without a functioning democracy or a free press.

Mr Kobak uses a test based on the “Poisson distribution”. This is named after a French statistician who first noticed that when modelling certain kinds of counts, such as the number of people who enter a railway station in an hour, the distribution takes on a specific shape with one mathematically pleasing property: the mean of the distribution is equal to its variance.

This idea can be useful in modelling the number of covid deaths, but requires one extension. Unlike a typical Poisson process, the number of people who die of covid can be correlated from one day to the next—superspreader events, for example, lead to spikes in deaths. As a result, the distribution of deaths should be what statisticians call “overdispersed”—the variance should be greater than the mean. Jonas Schöley, a demographer not involved with Mr Kobak’s research, says he has never in his career encountered death tallies that would fail this test.

….

The Russian numbers offer an example of abnormal neatness. In August 2021 daily death tallies went no lower than 746 and no higher than 799. Russia’s invariant numbers continued into the first week of September, ranging from 792 to 799. A back-of-the-envelope calculation shows that such a low-variation week would occur by chance once every 2,747 years.

Russia’s daily tolls of coronavirus infections and deaths surged to another record on Friday, a quickly mounting figure that has put a severe strain on the country’s health care system.

The government’s coronavirus task force reported 32,196 new confirmed coronavirus cases and 999 deaths in the past 24 hours.

The record for daily COVID-19 deaths in Russia has been broken repeatedly over the past few weeks, as fatalities steadily approach 1,000 in a single day. It comes amid increasing infections and a reluctance by authorities to toughen restrictions that would further cripple the economy.

The government said this week that about 43 million Russians, or just about 29% of the country’s nearly 146 million people, are fully vaccinated. Authorities have tried to speed up the pace of vaccination with lotteries, bonuses and other incentives, but widespread vaccine skepticism and conflicting signals from officials stymied the efforts.

The number of new daily cases is currently around 25,000, somewhat fewer than in Britain, and rising. But whereas in Britain this surge has translated into an average of 18 daily deaths over the past week, in Russia it has resulted in an average of 670 deaths a day.

The contrast is all the more striking because Russia was the first country in the world to approve a working vaccine, one based on the same science as the British-Swedish AstraZeneca one and apparently just as effective. But whereas in Britain 78% of the population has received at least one jab, in Russia the proportion is only 20%. The difference is not the availability or the efficacy of the jab, but people’s trust in the government and its vaccines.

All of this could have been avoided. A year ago the government decided to lift a partial lockdown (Mr Putin called it “a holiday”), hoping to save itself money and to prop up the president’s faltering popularity after a prolonged slump in incomes. Mr Putin’s ratings did go back up—but so did the risk of infection.

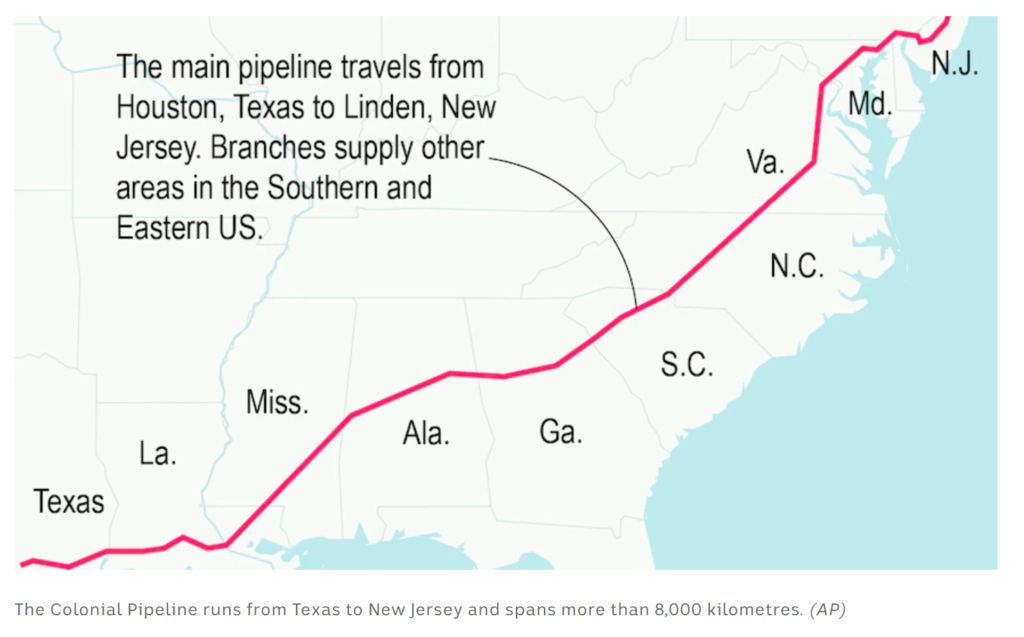

The Justice Department said on Monday that it had seized much of the ransom that a major U.S. pipeline operator had paid last month to a Russian hacking collective, turning the tables on the hackers by reaching into a digital wallet to snatch back millions of dollars in cryptocurrency.

Investigators in recent weeks traced 75 Bitcoins worth more than $4 million that Colonial Pipeline had paid to the hackers as the attack shut down its computer systems, prompting fuel shortages, a spike in gasoline prices and chaos at airlines.

Federal investigators tracked the ransom as it moved through a maze of at least 23 different electronic accounts belonging to DarkSide, the hacking group, before landing in one that a federal judge allowed them to break into, according to law enforcement officials and court documents.

The Justice Department said it seized 63.7 Bitcoins, valued at about $2.3 million. (The value of a Bitcoin has dropped over the past month.)