The higher the interest rates, the more costly the financing of a new project is over the long run, thus increasing pressure on the municipal budget.

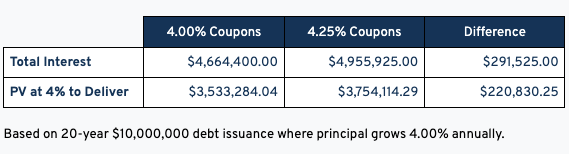

The example below compares the cost of a 20-year, $10 million debt issuance at different rates. “Coupons” refer to the interest rate that bondholders get back on their investment. “PV” stands for “present value,” or the face value of the bonds when they’re issued.

The reasons behind the racial disparity in refinancing align with documented evidence about other inequities in housing, Keys said during an interview with Wharton Business Daily on SiriusXM. (Listen to the podcast above.) Structural racism built into both public policy and the private sector has led to longstanding asymmetry in income, credit scores, loan-to-value ratios and other risk factors that inhibit refinancing for minorities.

The coronavirus pandemic is exacerbating the problem, Keys said, because Black and Hispanic households are more likely to experience job loss than white households. The U.S. unemployment rate in May dropped to 5.8%, yet it was 7.3% for Hispanics and 9.1% for Blacks.

“Some of this may be a function of just measuring incomes and employment disruptions, but I think there is another factor, which is related to just how tight mortgage credit is right now,” Keys added. “Mortgage credit is perceived as being very tight. It can be a hard time to get a loan, and there are a lot of hoops to jump through when you’re refinancing.”

Author(s): Benjamin Keys interviewed on Wharton Business Daily

The coronavirus pandemic changed the way U.S. consumers use credit, as lower interest rates spurred a boom in home buying and refinancing and virus-related shutdowns led to a drop in credit card use and an increase in paying off debt, according to a report released on Wednesday by the New York Federal Reserve.

Total household debt last year increased by $414 billion to $14.56 trillion at the end of December, the New York Fed found in its quarterly household debt and credit report.