Excerpt:

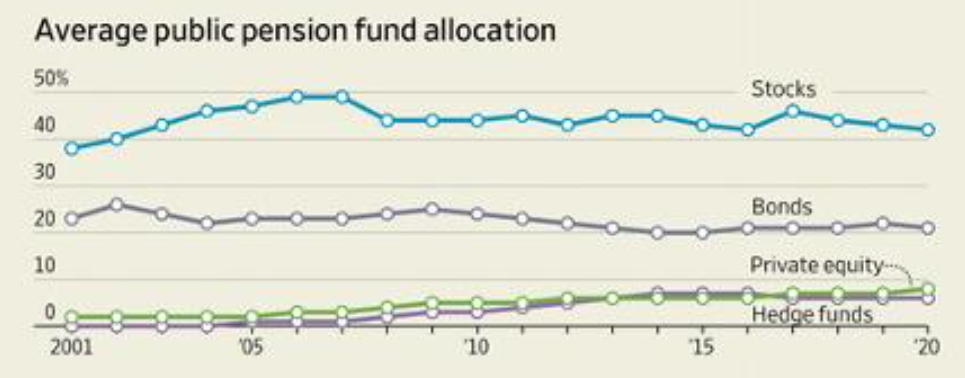

The State Teachers’ Retirement Board of Ohio shifted its asset mix at its board meeting last week, announcing it will now target 26% of its assets to U.S. equities, down from 28%. It also decreased its international equity allocation to 22% from 23%. The fund increased its allocation to private equity to 9% from 7% and its allocation to fixed income to 17% from 16%.

The increase in private equity, which had record returns this past year, is part of a broader trend. STRS Ohio saw 29% returns in fiscal year 2021, in part driven by a 45% return on alternative assets. These returns were topped only by domestic equities, which returned 46.3% for the fund.

The pension plan is also beginning to share some of these returns with pension beneficiaries. At its board meeting last week, the pension approved a 3% one-time cost-of-living increase for beneficiaries who retired before June 1, 2018. The 3% adjustment is still less than half of the Bureau of Labor Statistics’ official inflation calculation of 7% in 2021.

Author(s): Anna Gordon

Publication Date: 22 Mar 2022

Publication Site: ai-CIO