Link: https://content.naic.org/sites/default/files/capital-markets-special-reports-CLO-YE%202021.pdf

Graphic:

Excerpt:

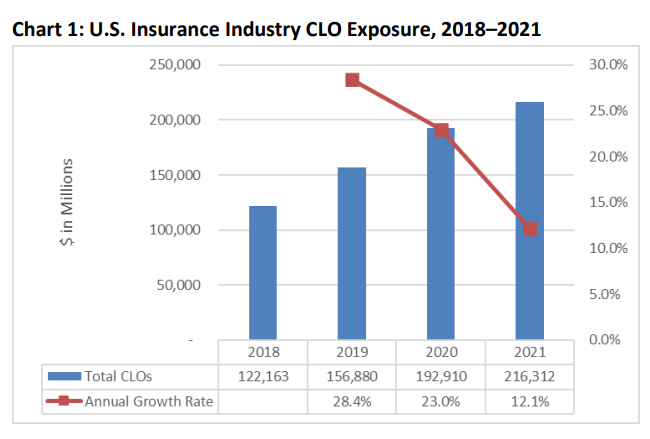

U.S. insurers’ exposure to CLOs increased significantly over the last few years, as they have represented

an attractive alternative investment with higher yields than traditional investments. As of year-end

2021, U.S. insurers’ exposure to CLOs collateralized predominantly by leveraged bank loans and middle

market loans increased by 12% to $216.3 billion in BACV from $192.9 billion at year-end 2020 and $156.9 billion at year-end 2019 (see Chart 1). However, the pace of growth has slowed from 23% and

28% at year-end 2020 and year-end 2019, respectively.

Author(s): Jennifer Johnson, Michele Wong, Jean-Baptiste Carelus

Publication Date: 15 Sept 2022

Publication Site: NAIC Capital Markets Bureau