Most insurance companies at that time assessed hurricane exposure in their portfolios by simply multiplying customer premiums by a rough factor of supposed risk, rather than tracking actual property replacement costs. “They were just very crude formulas,” she said.

So in 1987, Clark had started her own company, Applied Insurance Research, or AIR, to develop software that better estimated the potential losses from catastrophic events. Unlike the rest of the industry, she used granular data and sophisticated analyses, an approach now called catastrophe modeling. Her first computer model estimated that a Category 5 hurricane hitting Dade County could cause losses almost 10 times more than previously believed. She warned her customers about the risk in Florida, but until Hurricane Andrew, no one listened.

Social Security states, at this link: retirement/planner/AnypiaApplet.html, that “(Its) Online Calculator is updated periodically with new benefit increases and other benefit amounts. Therefore, it is likely that your benefit estimates in the future will differ from those calculated today.” It also says that the most recent update was in August 2023.

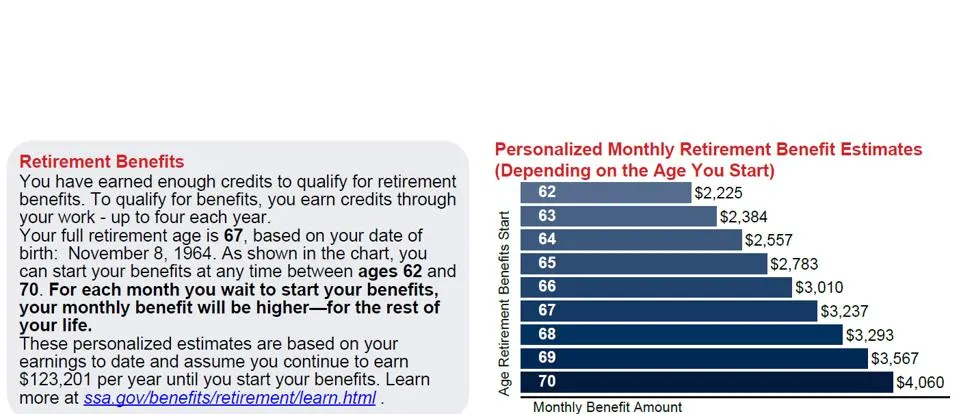

This statement references Social Security’s Online Calculator. But they have a number of calculators that make different assumptions. And it’s not clear what calculator they used to produce the graphic, see below, that projects your future retirement benefit conditional on working up to particular dates and then collecting immediately. Nor is Social Security making clear what changes they are making to their calculators through time.

What I’m quite sure is true is that the code underlying Social Security’s graphic projects your future earnings at their current nominal value. This is simply nuts. Imagine you are age 40 and will work till age 67 and take your benefits then. If inflation over the next 27 years is 27 percent, your real earnings are being projected to decline by 65 percent! This is completely unrealistic and makes the chart, if my understanding is correct, useless.

….

The only thing that might, to my knowledge, reduce projected future future benefits over the course of the past four months is a reduction in Social Security’s projected future bend point values in its PIA (Primary Insurance Amount) formula. This could lead to lower projected future benefits for those pushed higher PIA brackets, which would mean reduced benefit brackets. This could also explain why the differences in projections vary by person.

….

Millions of workers are being told, from essentially one day to the next, that their future real Social Security income will be dramatically lower. Furthermore, the assumption underlying this basic chart — that your nominal wages will never adjust for inflation — means that for Social Security’s future benefit estimate is ridiculous regardless of what it’s assuming under the hood about future bend points.

….

One possibility here is that a software engineer has made a big coding mistake. This happens. On February 23, 2022, I reported in Forbes that Social Security had transmitted, to unknown millions of workers, future retirement benefits statements that were terribly wrong. The statement emailed to me by a worker, which I copy in my column, specified essentially the same retirement benefit at age 62 as at full retirement age. It also specified a higher benefit for taking benefits several few months before full retirement.

Anyone familiar with Social Security benefit calculations would instantly conclude that there was either a major bug in the code or that that, heaven forbid, the system had been hacked. But if this wasn’t a hack, why would anyone have changed code that Social Security claimed, for years, was working correctly? Social Security made no public comment in response to my prior column. But it fixed its code as I suddenly stopped receiving crazy benefit statements.