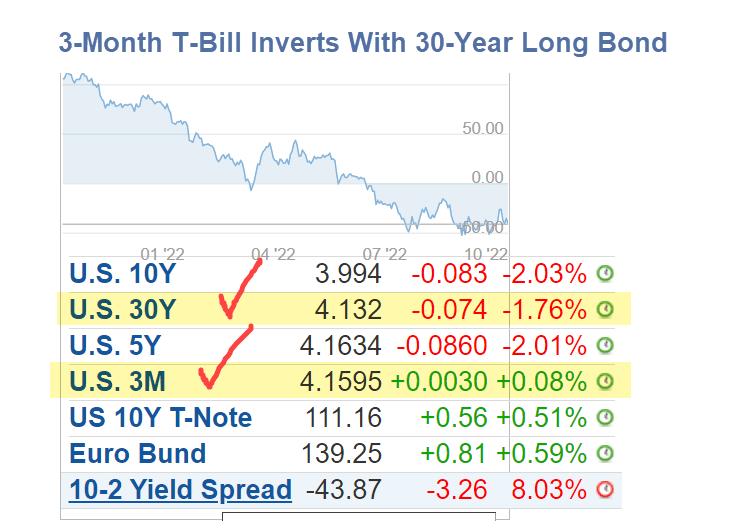

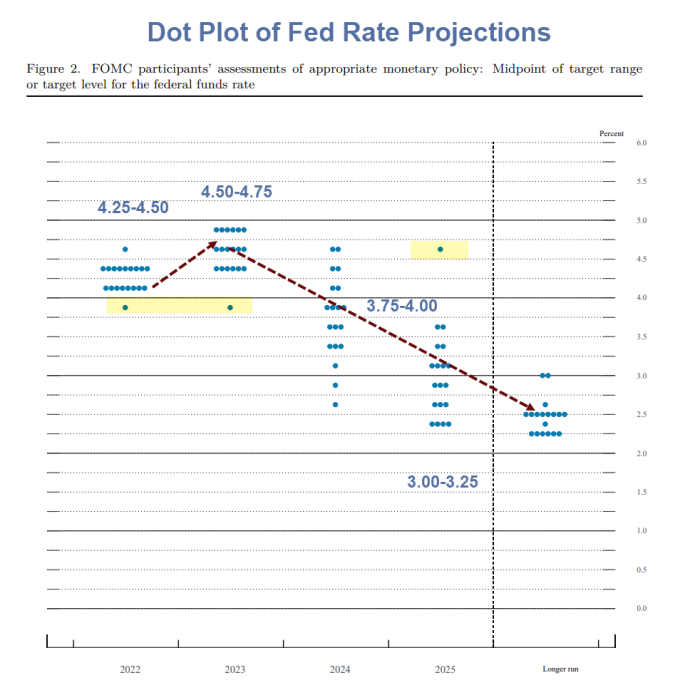

The Fed participants have a median expectation of 4.25 to 4.50 percent for the end of 2022

That’s another 1.25 percentage points more this year.

The Fed then anticipates one more hike in 2023 to 4.50 to 4.75 percent.

I have to admit that a year ago I did not foresee this. But here we are.

The key question is not where we’ve been but where we are headed. I Highly doubt the Fed hikes another 1.25 percentage points this year or gets anywhere close to 4.50 to 4.75 percent in 2023.

The Governing Council today decided to raise the three key ECB interest rates by 75 basis points. This major step frontloads the transition from the prevailing highly accommodative level of policy rates towards levels that will ensure the timely return of inflation to our two per cent medium-term target. Based on our current assessment, over the next several meetings we expect to raise interest rates further to dampen demand and guard against the risk of a persistent upward shift in inflation expectations.

Inflation remains far too high and is likely to stay above our target for an extended period. According to Eurostat’s flash estimate, inflation reached 9.1 per cent in August. Soaring energy and food prices, demand pressures in some sectors owing to the reopening of the economy, and supply bottlenecks are still driving up inflation.

Price pressures have continued to strengthen and broaden across the economy and inflation may rise further in the near term.

Very high energy prices are reducing the purchasing power of people’s incomes and, although supply bottlenecks are easing, they are still constraining economic activity. In addition, the adverse geopolitical situation, especially Russia’s unjustified aggression towards Ukraine, is weighing on the confidence of businesses and consumers.

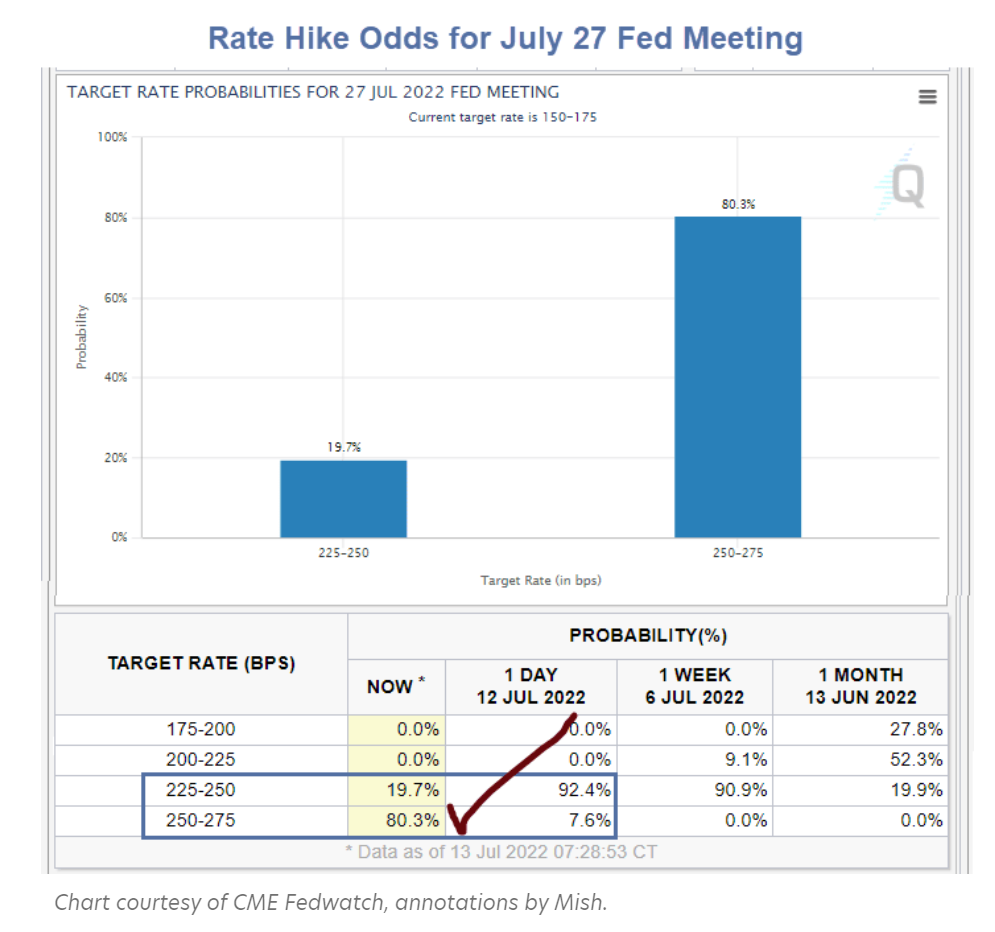

Yesterday, the market penciled in a three-quarter point hike. Today, the market expectation is for a full point hike.

The WSJ notes that would be the largest hike since the Fed started directly using overnight interest rates to conduct monetary policy in the early 1990s.

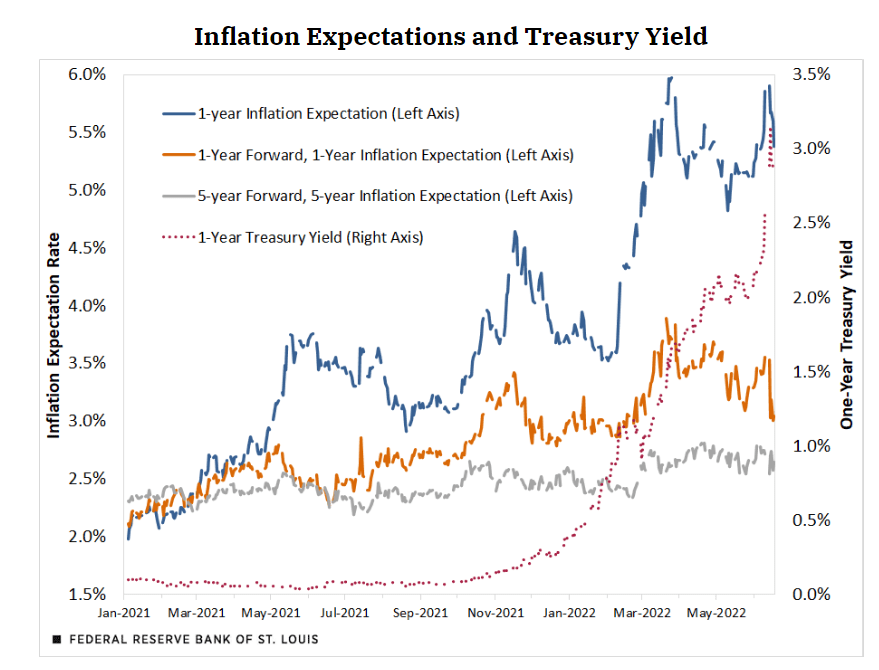

Common sense and practical examples suggest that inflation expectations theory is ass backward.

So much of the CPI is nondiscretionary that it’s difficult to impossible for CPI expectations to matter.

Yet, economists focus on expectations that don’t matter and ignore the expectations that do matter, namely asset prices!

I have written about this several times previously, two of them before I even found the Fed study supporting my view.

…..

A BIS study concluded “Deflation may actually boost output. Lower prices increase real incomes and wealth. And they may also make export goods more competitive.“

Indeed, that must be the case as more goods for less money by default improves standards of living.

The Fed was hell bent on reducing standards of living via inflation. Now they struggle to undo the inflation and asset bubble consequences they created.

1. Japan can defend its interest rate line by printing more money but at expense of the yen

2. Japan can defend the yen by hiking rates or by selling its reserves until reserves run out

Japan has a nasty choice

I received this email reply to the above Tweet from Michael Pettis.

“Looks right. I’d add that by weakening the yen, Japan seems always to support their exporters at the expense of their consumers, which may be why domestic demand is always so weak and growth so sluggish.“

The smart thing for Japan would be to hike rates and let the Yen strengthen.

Instead, if they stay on the same path, the yen might blow up.

All of Japan’s efforts to achieve growth by inflation and exports have backfired. One might think that after 40 years they would try something else.

The single worst choice for Japan would be to blow its currency reserves in an attempt to defend both the Yen and its interest rate peg.

“This is surely unworkable – a carve out for Hungary, which allows its refineries to enjoy sky rocketing margins on sales elsewhere in the EU because of their access to Russian crude. It’s almost laughable,” said Jeremy Warner.

It seems the carve out for Hungary was “workable” after all, with predictable results.

Russia, China, Hungary, and energy producers are the beneficiaries of these terribly counterproductive sanctions.

This is my “Hoot of the Day” but it’s early. I may easily need bonus hoots.

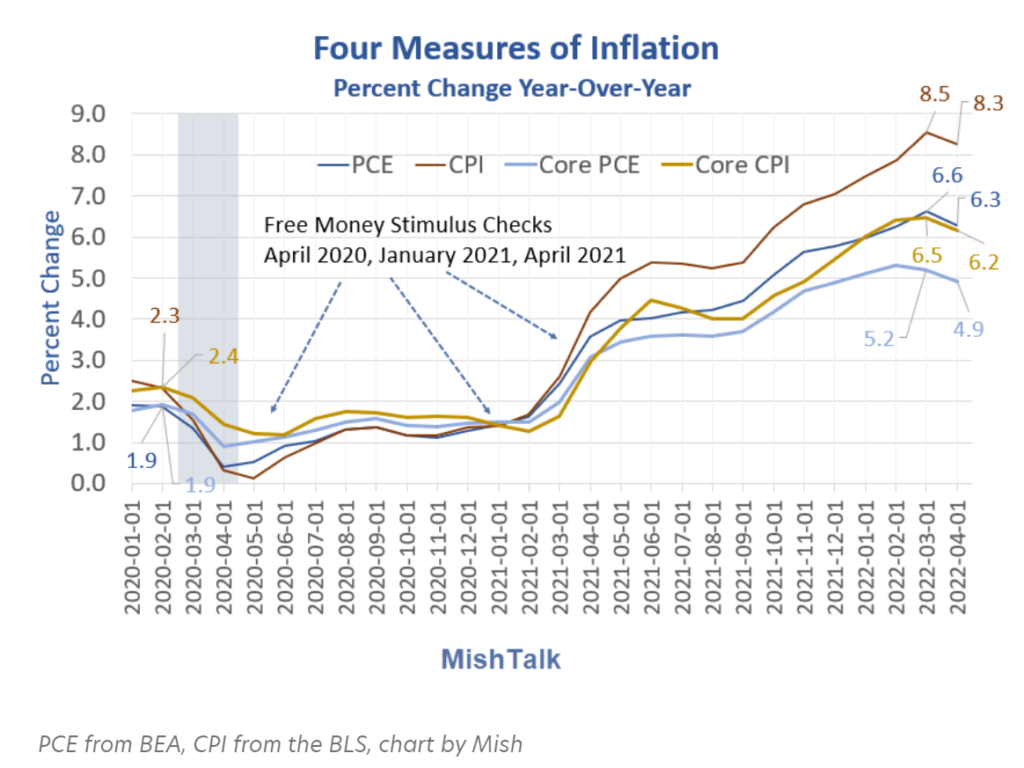

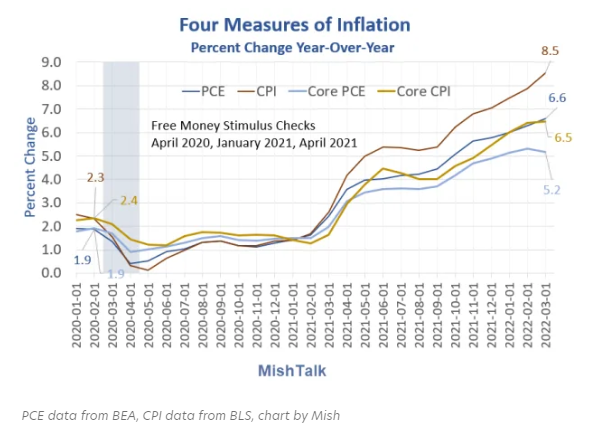

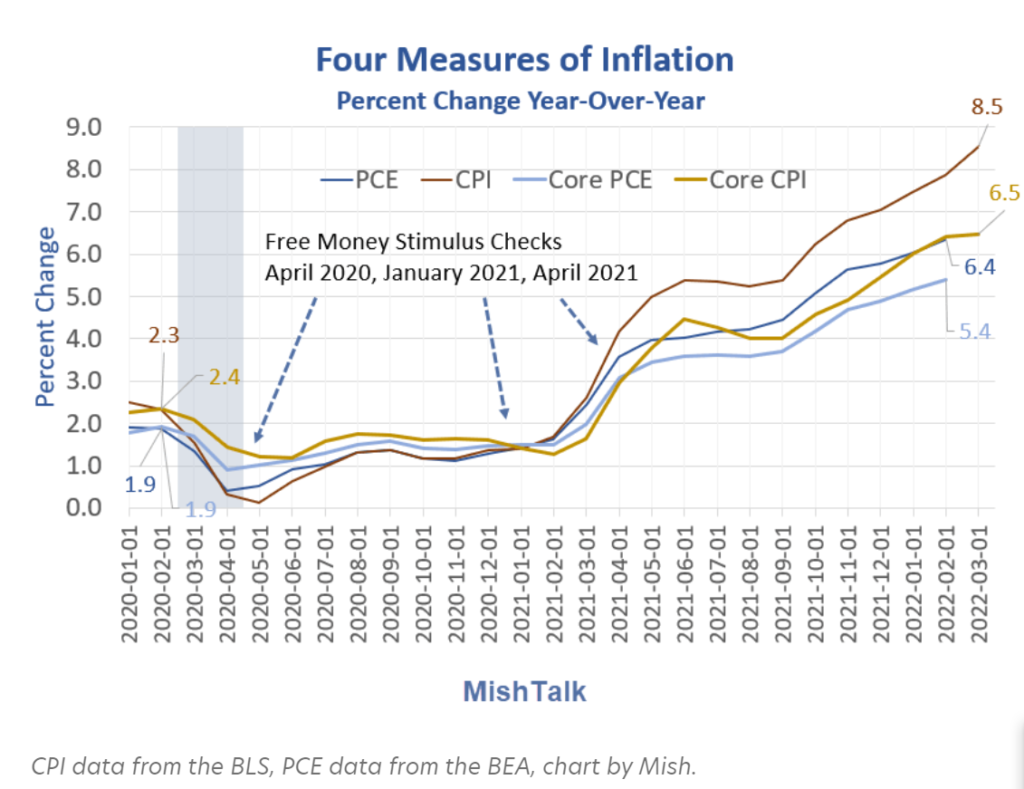

PCE stands for Personal Consumption Expenditures. Those numbers come from the Bureau of Economic Analysis (BEA)

CPI stands for Consumer Price Index. Those numbers come from the Bureau of Labor Statistics (BLS)

The key difference is the PCE includes prices paid on behalf of consumers (e.g. Medicare and Medicaid), whereas the CPI only contains prices directly paid by consumers.

The PCE tends to overweight medical expenses while the CPI tends to overweight rent.

The Fed’s preferred measure of inflation is PCE.

CPI and PCE Both Seriously Flawed

Neither measure directly incorporates home prices. Economists explain this away by stating homes are a capital expense.

OK, so what? The fact is, rising home prices (asset prices in general), are a direct reflection of inflation.

By ignoring asset prices, the Fed helped blow the biggest economic bubble yet. Now the Fed struggles to contain the serious inflation it helped create.

At the ECB, you better be gung-ho pro-EU. You better believe negative interest rates are a good idea. And you must back the idea that targeting 2% inflation makes sense.

Finally, if somehow you find yourself at the ECB disagreeing with any of those things, you are expected to shut your mouth so the consensus view never shows any dissent.

….

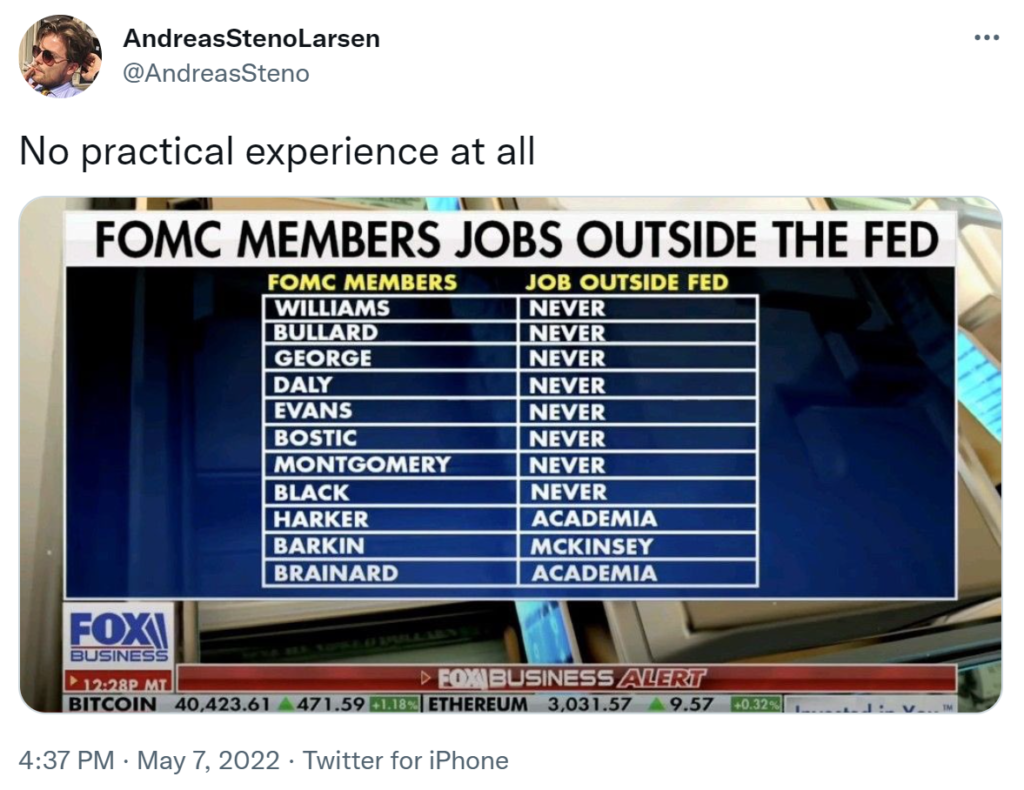

At FRBNY, I recall the people who ran Treasury markets, money markets, etc. literally had no relevant experience or expertise. The job of staff was to make them appear competent, but it didn’t really matter what they did because Fed can’t fail and they can’t get fired.

This creates a culture where anyone with talent or ambition GTFO ASAP. There are exceptions, but those who rise tend to be those who have no where else go. It’s a weird structure where the higher you go, the more incompetent you are.

The question is not as straight forward as it looks. The gap between spending and income isn’t constant.

Free money that goes to bottom rung households tends to immediately get spent. The higher the rung, the more the savings. This is complicated by the fact that most of the money was supposed to go to lower tiers, and further complicated by corporate fraud, especially in round one.

More importantly, personal spending does not count mortgage paydowns, stock market or Bitcoin purchases, capital expenses for businesses, drug money, other illegal uses, or money sent to relatives overseas.

….

The Peterson Foundation reports direct checks were $292 billion in round one, $164 billion in round two, and $411 billion in round three.

There was $850 billion of direct payments to taxpayers with the biggest and most unwarranted round the last.

Spending data suggests free money, at least most of direct payments, already did enter the economy.

However, that does not factor in unpaid rent via eviction moratoriums or SNAP (Supplemental Nutrition Assistance Program), formerly Food Stamps, which I will address in a separate post.

So yes, there still could be a pile of unspent stimulus savings, possibly much higher than my $2 trillion summation estimate, again with my caveats on investments, sending money overseas, etc.