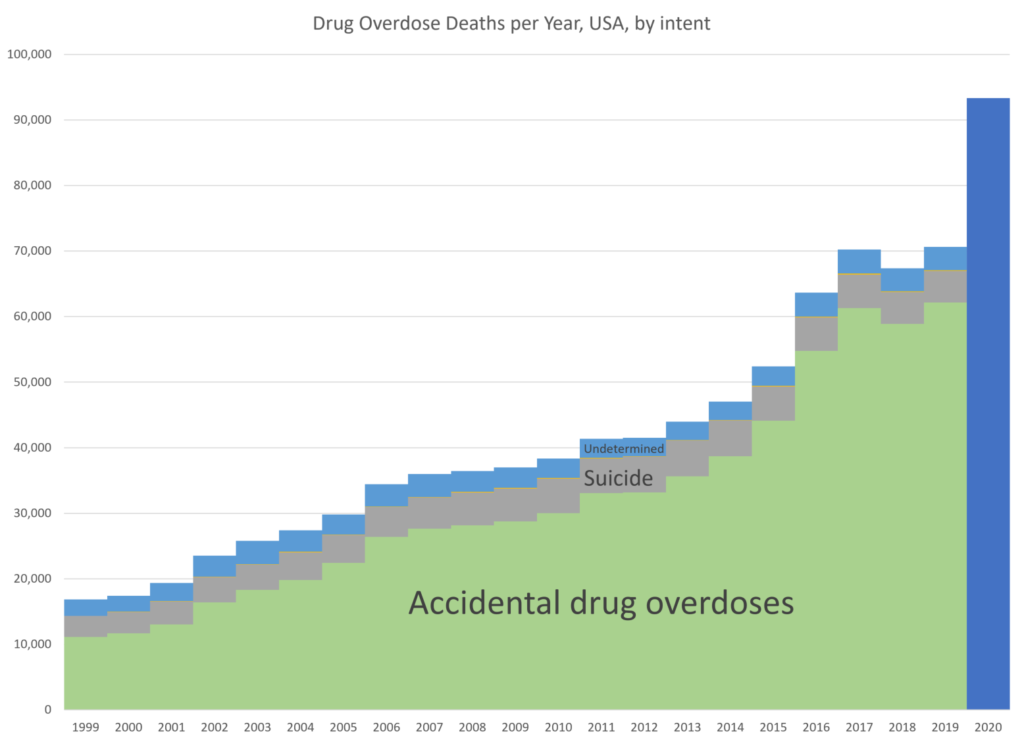

In 2020, there were over 93K deaths due to drug overdoses — a 30% increase over 2019.

This is super-bad, and worse than what I have seen for increases in other causes of death. I knew it was going to be bad, but I didn’t realize it was going to be this bad.

In the pre-computer days, people used these approximations due to having to do all calculations by hand or with the help of tables. Of course, many approximations are done by computers themselves — the way computers calculate functions such as sine() and exp() involves approaches like Taylor series expansions.

The specific approximation techniques I try (1 “exact” and 6 different approximation… including the final ones where I put approximations within approximations just because I can) are not important. But the concept that you should know how to try out and test approximation approaches in case you need them is important for those doing numerical computing.

Author(s): Mary Pat Campbell

Publication Date: 3 February 2016 (updated for links 2021)

Publication Site: LinkedIn, CompAct, Society of Actuaries

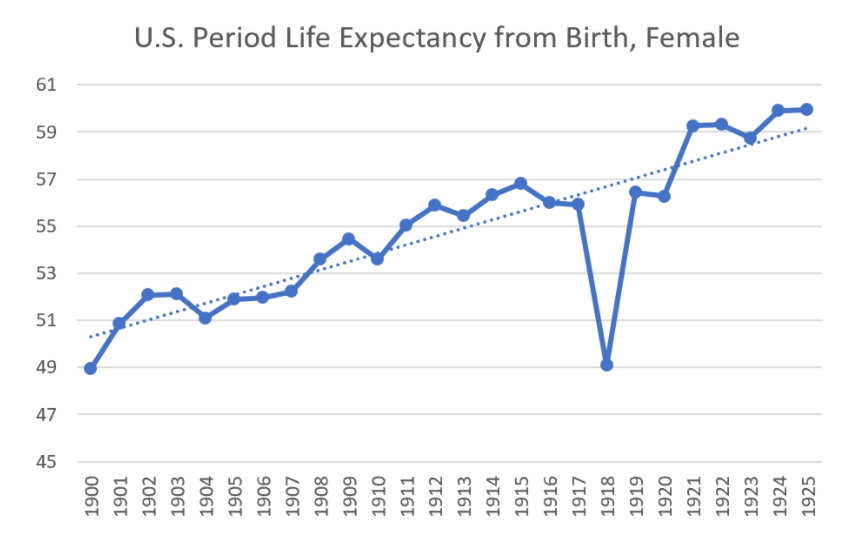

The Spanish flu pandemic gives us the demonstration of what happens when there is a short-term large increase in mortality.

Using Social Security records of period life expectancy, there was a huge drop in life expectancy in 1918…. and then a huge increase in 1919. But going from 1917 to 1919 wasn’t really that big of a difference.

The period life expectancy drop was 12% for females, 13% for males in 1918.

Then there was an increase of 15% for females, 20% for males in 1919. The Spanish flu hit the U.S. hard in 1918, and let up in 1919.

If you compare 1919 against 1917, the life expectancy from birth increase was 1% for females, and 4% increase for males — male life expectancy was down in 1917 compared to 1916, probably related to World War I.

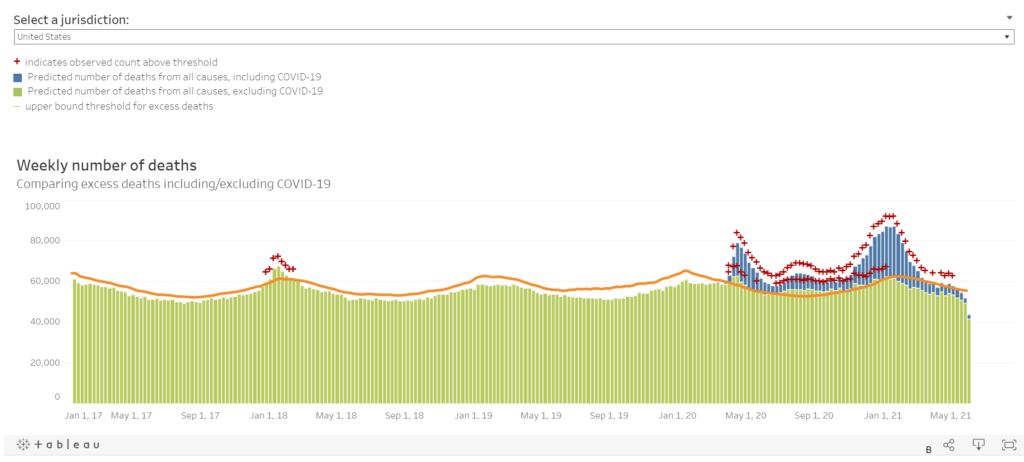

I want you to notice something — the blue bars are the “with COVID” portion of deaths, and the chartreuse bars are the ones “without COVID”. The bars are weekly counts of deaths when they occurred. Ignore the most recent weeks because they don’t have full data reported yet.

The red pluses indicate excess mortality, defined as exceeding the 95th percentile for expected mortality for that week (so it includes seaonality). You can see the excess mortality from the 2017-2018 flu season, which was bad for a flu season.

The non-COVID mortality has been in excessive mortality range for almost all 2020 after March. But since the beginning of 2021, it has dropped off…. and COVID mortality has also dropped off.

I think we may be almost in “normal” range soon. We shall see!

Welcome to another episode of Positivity with Paul, where I find Fellow Actuaries – pun intended – for a conversational Q&A on their life. The focus is on their journey along the actuarial exam path and beyond, some of the challenges they faced, and how those challenges helped shape them to become who they are today.

To give some brief context on becoming an Actuary, there’s a number of actuarial exams that one has to go through. These exams are very rigorous and typically, only the top 40% pass at each sitting, They cover complex mathematical topics like statistics and financial modelling but also insurance, investments, regulatory and accounting. Candidates can study up to 5 months per sitting and they will take 7 to 10 years on average to earn their Fellowship degree. To that end, I launched this series of podcasts because I was curious about what drove my guests to surmount trials and tribulations to get to the end goal of becoming an Actuary.

My guest in this interview is Mary Pat Campbell. Mary Pat is an actuary working in Connecticut, investigating life insurance and annuity industry trends. She has been interested in exploring mortality trends, public finance and public pensions as an avocation. Some of these explorations can be found at her blog: stump.marypat.org. Mary Pat is a fellow of the Society of Actuaries and a member of the American Academy of Actuaries. She has been working in the life/annuity industry since 2003. She holds a master’s degree in math from New York University and undergraduate degrees in math and physics from North Carolina State University. In this podcast, Mary Pat discusses similarities in concepts between physics and actuarial science, the current low interest rate environment and lessons learnt in the insurance sector from the financial crisis in 2008-2009. Hope you enjoy this all-inclusive interview! Paul Kandola

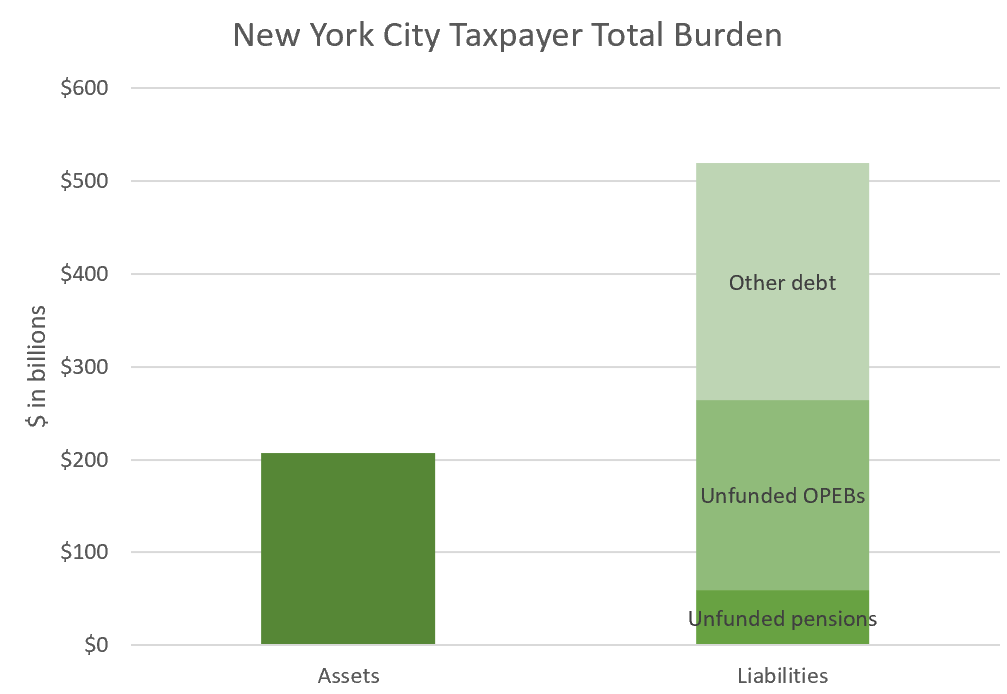

NPPC, I recommend you think through what will actually inform and protect your members. The TIA folks are not distorting the message, except to the extent that state and local governments are undervaluing their pension and OPEB promises.

Complaining about TIA will not make the pensions better-funded. Complaining about TIA will not prevent the worst-funded pensions from running out of assets, which will not be supportable as pay-as-you-go, as the asset death spiral before that will show that the cash flows were unaffordable for the local tax base.

And don’t look to the federal government to save your hash. So far bailout amounts have been puny compared to the size of the promises.

Reviewing the recent Society of Actuaries report on preliminary mortality results in U.S. population, with a focus on increased mortality from non-COVID causes. U.S. Population Mortality

Observations, Preview of 2020 Experience Society of Actuaries research:

In particular, it is pretty clear to me that specifically in the U.S., the non-COVID excess mortality has been very high. I do not think that’s under-counted COVID deaths. I think it’s due to other causes. We’ve already seen that car accident deaths were up, even though total miles driven was down by a lot.

So yay for their statistics in grabbing the excess deaths, but boo for assuming all those excess deaths were COVID.

Now, results of COVID and COVID policies, sure, I’d go with that. But do you want to start digging into the stats of suicides, drug overdoses, “accidental” deaths, and more? How about deaths of neglect? I bet that is involved in a bunch of non-COVID elderly deaths.

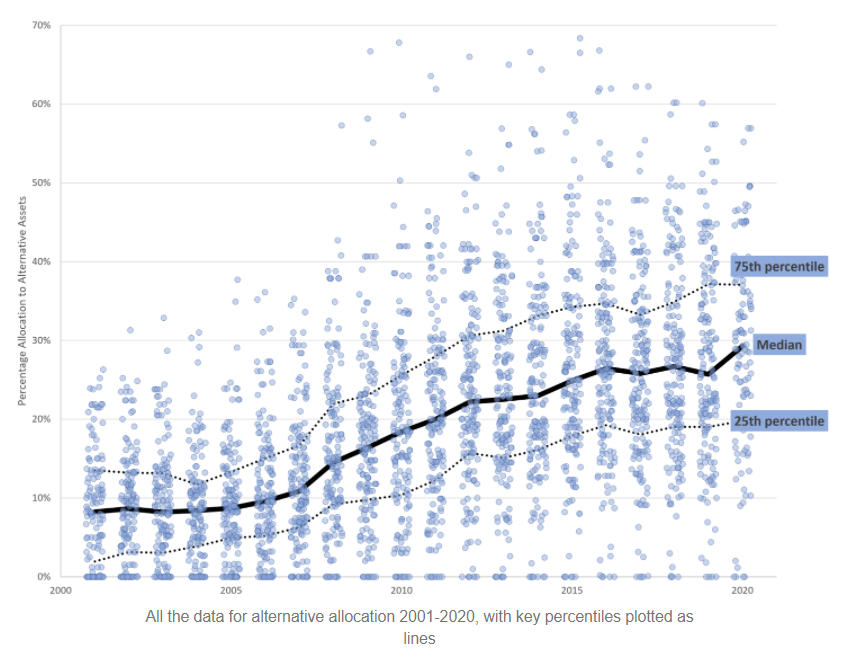

All the data for alternative allocation 2001-2020, with key percentiles plotted as lines

Excerpt:

What you see in that graph is a data point for each of the plans I know their asset allocation for, with the median, 25th percentile, and 75th percentiles marked out so you can see the allocations increasing.

That pattern does not make me feel good.

Allocating more to alternatives doesn’t seem to get asset managers higher returns. But the group is generally sliding upwards in their allocations, and I’m very unhappy about this.