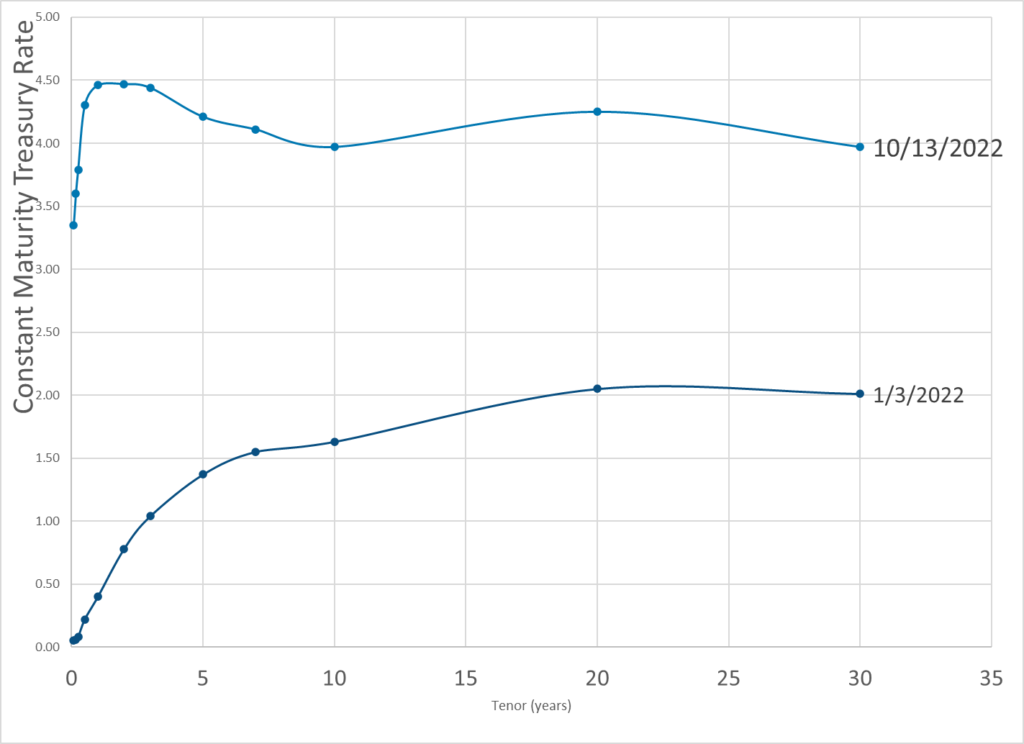

Graphic:

Publication Date: 13 Oct 2022

Publication Site: Dept of Treasury

All about risk

Graphic:

Publication Date: 13 Oct 2022

Publication Site: Dept of Treasury

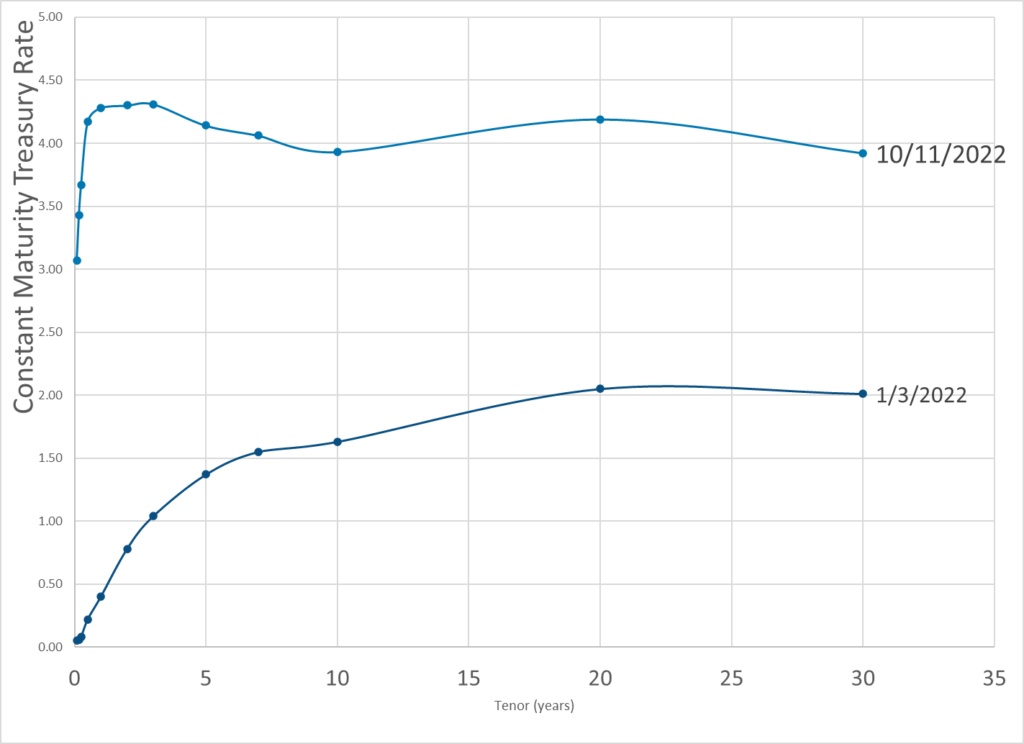

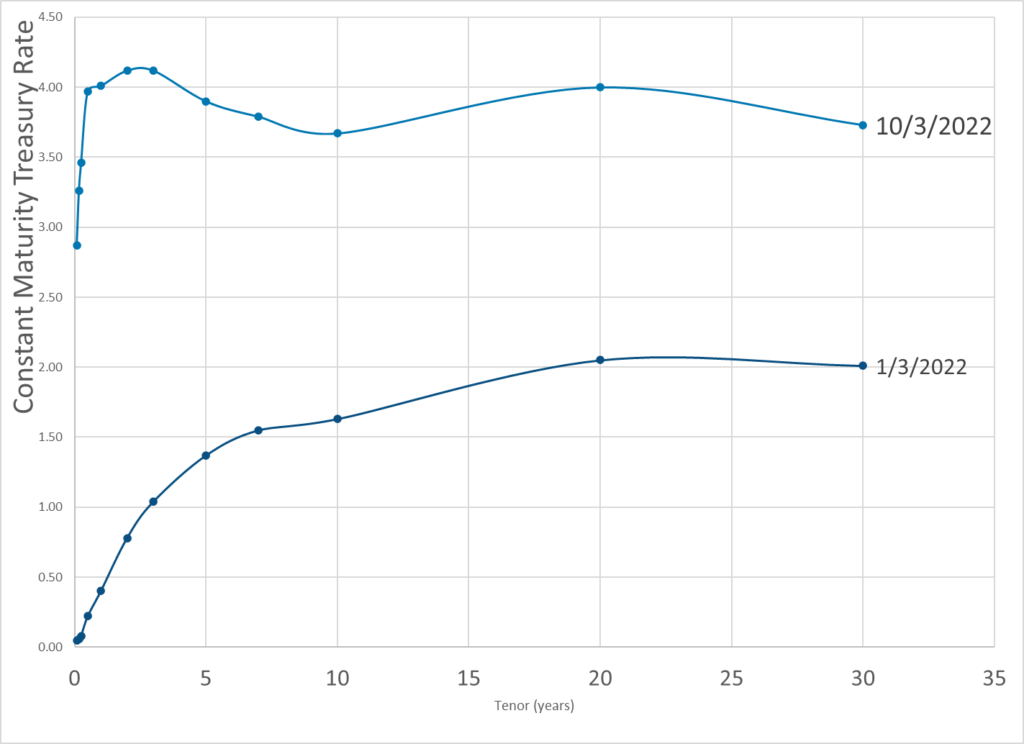

Graphic:

Publication Date: 11 Oct 2022

Publication Site: Dept of Treasury

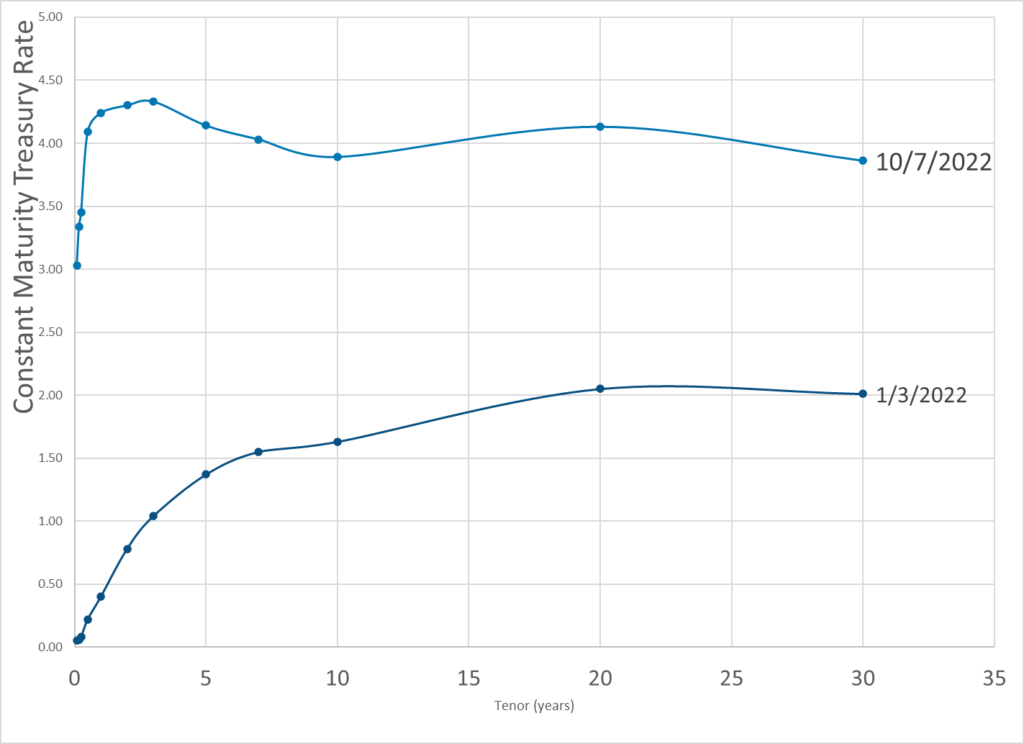

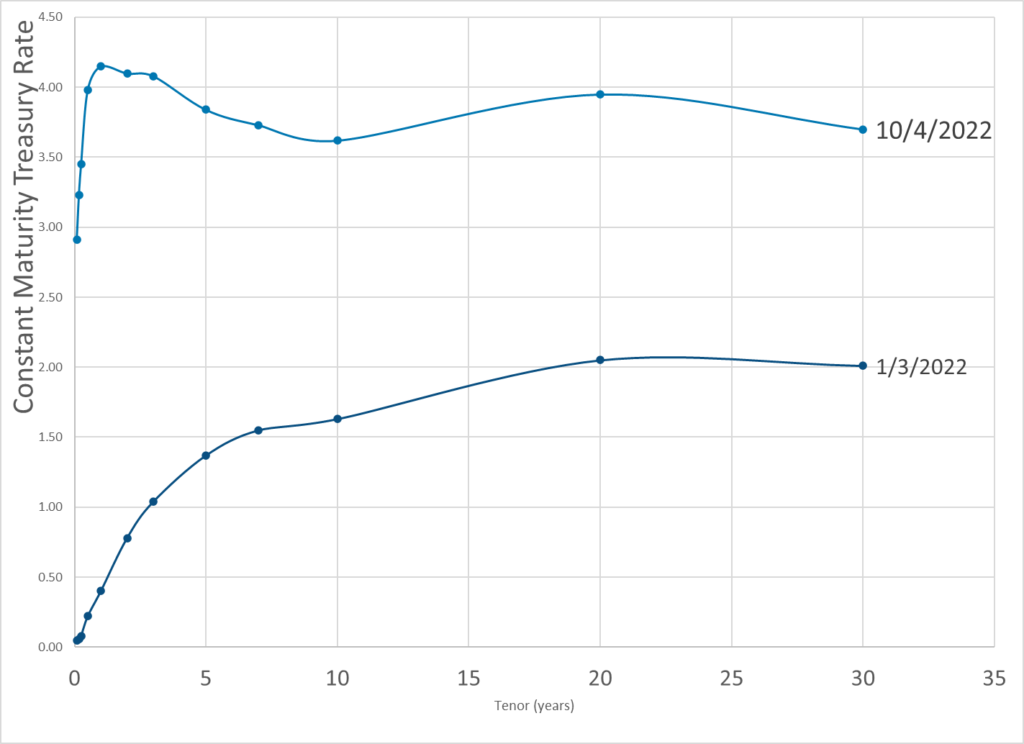

Graphic:

Publication Date: 7 Oct 2022

Publication Site: Dept of Treasury

Excerpt:

The Bank of England told lawmakers that a number of pension funds were hours from collapse when it decided to intervene in the U.K. long-dated bond market last week.

The central bank’s Financial Policy Committee stepped in after a massive sell-off of U.K. government bonds — known as “gilts” — following the new government’s fiscal policy announcements on Sept. 23.

The emergency measures included a two-week purchase program for long-dated bonds and the delay of the bank’s planned gilt sales, part of its unwinding of Covid pandemic-era stimulus.

The plunge in bond values caused panic in particular for Britain’s £1.5 trillion ($1.69 trillion) in so-called liability-driven investment funds (LDIs). Long-dated gilts account for around two-thirds of LDI holdings.

…..

The 30-year gilt yield fell more than 100 basis points after the bank announced its emergency package on Wednesday Sept. 28, offering markets a much-needed reprieve.

Cunliffe noted that the scale of the moves in gilt yields during this period was “unprecedented,” with two daily increases of more than 35 basis points in 30-year yields.

“Measured over a four day period, the increase in 30 year gilt yields was more than twice as large as the largest move since 2000, which occurred during the ‘dash for cash’ in 2020,” he said.

Author(s): Elliot Smith

Publication Date: 6 Oct 2022

Publication Site: CNBC

Link: https://www.pionline.com/pension-funds/uks-ldi-related-turmoil-could-spread-experts-say

Graphic:

Excerpt:

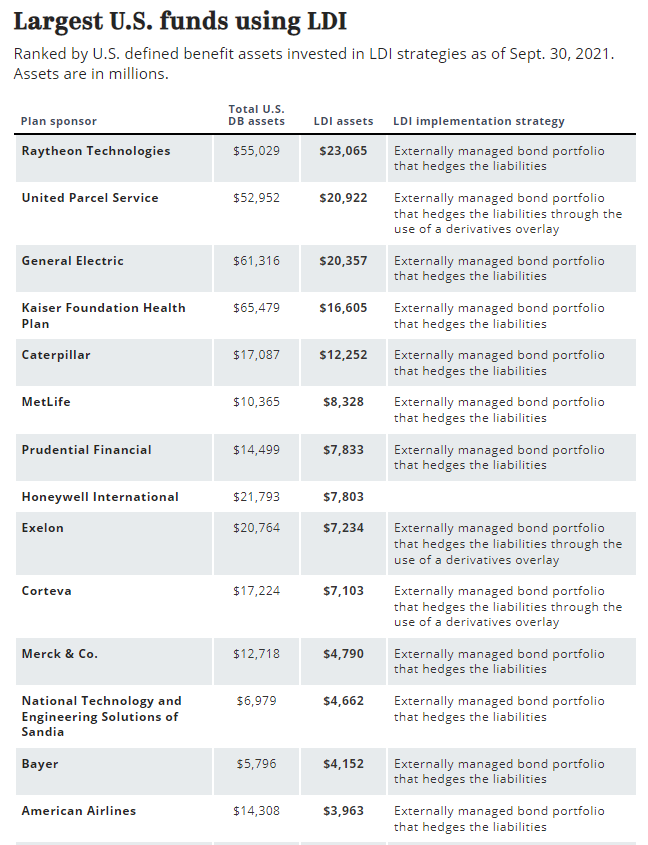

The Bank of England’s emergency bond-buying last week helped shore up U.K. pension funds and threw a spotlight on a popular strategy among corporate plans known as LDI – or liability-driven investing.

Total assets in LDI strategies in the U.K. rose to almost £1.6 trillion ($1.8 trillion) at the end of 2021, quadrupling from £400 billion in 2011, according to the Investment Association, a trade group that represents U.K. managers. Many LDI mandates allow for the use of derivatives to hedge inflation and interest rate risk.

….

Here’s how LDI works: Liability-driven investing is employed by many pension funds to mitigate the risk of unfunded liabilities by matching their asset allocation and investment policy with current and expected future liabilities. The LDI portion of a pension fund’s portfolio utilizes liability-hedging strategies to reduce interest-rate risk, which could include long government and credit bonds and derivatives exposure.

Jeff Passmore, LDI solutions strategist at MetLife Investment Management, said the situation with U.K. pension plans “has been challenging, and the heavy use of derivatives in the U.K. LDI model has made the current situation worse than it would otherwise be.”

While most U.S. LDI portfolios rely on bonds rather than derivatives, ‘”those U.S. plan sponsors who have leaned heavily on derivatives and leverage should take a cautionary lesson from what we’re seeing currently across the Atlantic.”

….

The U.K. pension debacle “is a plain-and-simple problem of leverage,” Charles Van Vleet, assistant treasurer and chief investment officer at Textron, said in an email.

Many U.K. pension plans were interest rate-hedged at 70%, while also holding 60% in growth assets, suggesting 30% leverage, he said. The portfolio’s growth assets have lost around 20% of value if held in public equities and fixed income or about 5% down if held in private equity, he noted.

“Therefore, to make margin calls on their derivative rate exposure they had to sell growth assets – in some cases, selling physical-gilts to meet derivative-gilt margin calls,” Mr. Van Vleet said.

“The problem is worse for plans who gain rate exposure with leveraged ETFs. The leverage in those funds is commonly via cleared interest rate swaps. Margin calls for cleared swaps can only be met with cash – not posted collateral. Therefore, again selling physical-gilts to meet derivative-gilt margin calls.”

Author(s):

BRIAN CROCE

COURTNEY DEGEN

PALASH GHOSH

ROB KOZLOWSKI

Publication Date: 5 Oct 2022

Publication Site: Pensions & Investments

Graphic:

Publication Date: 6 Oct 2022

Publication Site: Treasury Dept

Graphic:

Publication Date: 4 Oct 2022

Publication Site: Dept of Treasury

Graphic:

Publication Date: 3 Oct 2022

Publication Site: Treasury Dept

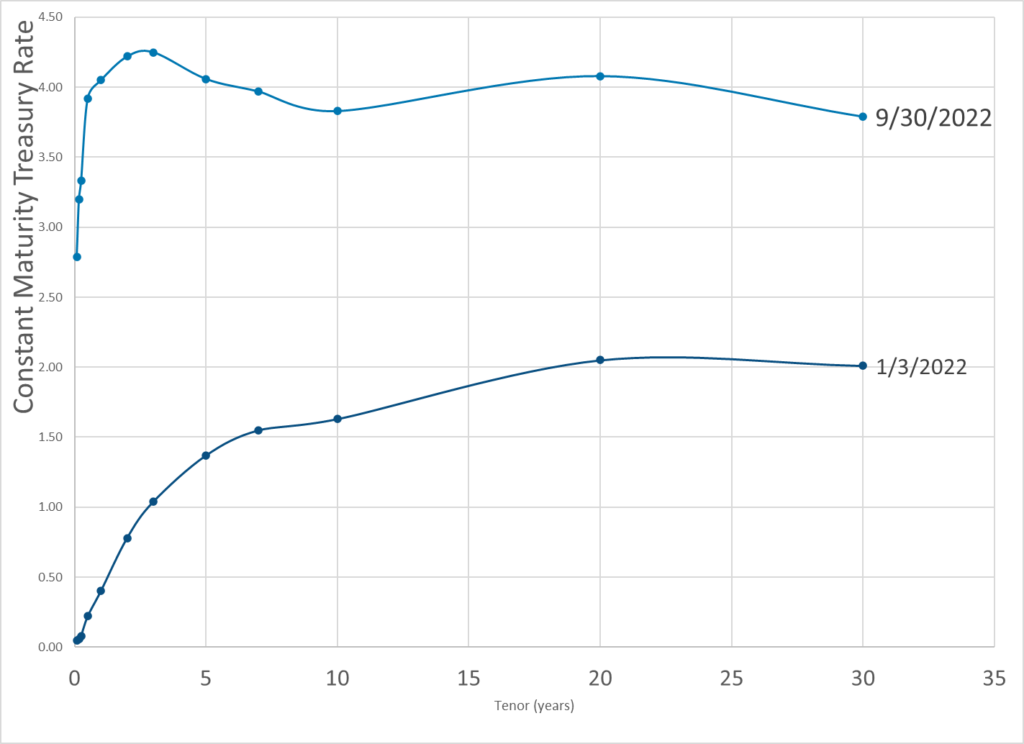

Graphic:

Publication Date: 30 Sept 2022

Publication Site: Dept of Treasury

Graphic:

Excerpt:

Interest rates cycle over long periods of time. The journey tends to be unpredictable, full of

unexpected twists and turns. This project focuses on the impact of interest rate volatility on life

insurance products. As usual, it brought up more questions than it answered. It points out the

importance of stress testing for a specific block of business and the risk of relying on industry

rules of thumb. Understanding the nuances of models could make the difference between safe

navigation of a stressed environment and a default. Proactive and resilient practices should

increase the odds of success.

Hyman Minsky had it right—stability leads to instability. We live in an era where monetary

policies of central banks steer free markets in an effort to soften the business cycle. Rates have

been low for over 20 years in Japan, reshaping the global economy.The primary goal of this paper is to explore rising interest rates, but that is not possible without

considering that some rates could stabilize at low levels or even decrease. Following this path,

the paper will look at implications of interest rate changes for the life insurance industry, current

stress testing practices, and how a risk manager can proactively prepare for an uncertain future.

A paper published in 2014 focused on why rates could stay low, and some aspects of this paper

are similar (e.g., description of insurance products). This paper also uses a sample model office

to help practitioners look at their own exposures. It includes typical interest-sensitive insurance

products and how they might perform across various scenarios, as well as a survey to establish

current practices for how insurers are testing interest rate risk currently.

Author(s): Max Rudolph, Randy Jorgensen, Karen Rudolph

Publication Date: July 2015

Publication Site: SOA Research Institute