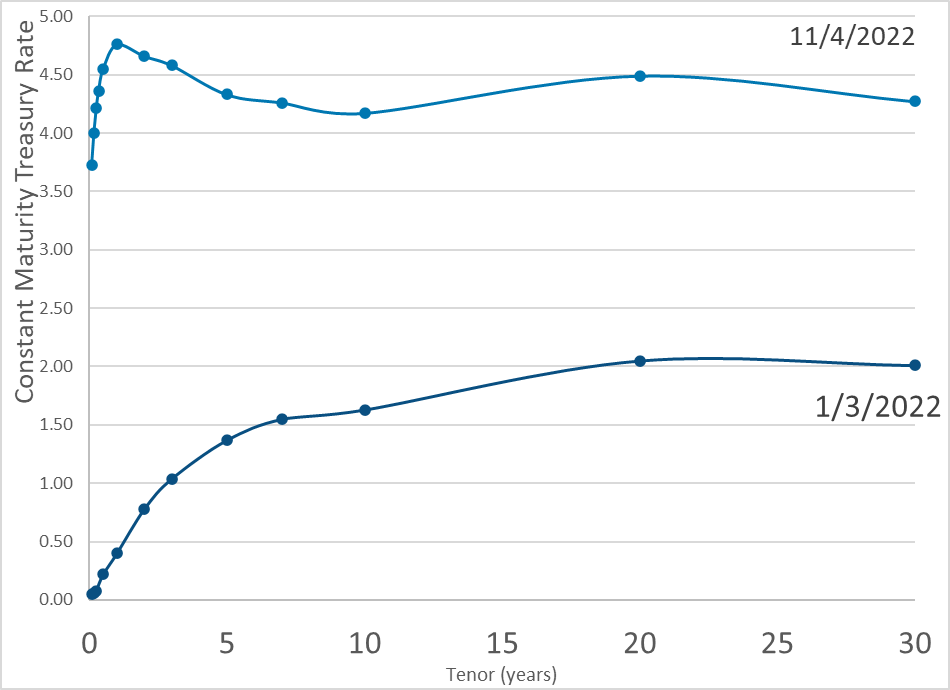

Graphic:

Publication Date: 4 Nov 2022

Publication Site: Dept of Treasury

All about risk

Graphic:

Publication Date: 4 Nov 2022

Publication Site: Dept of Treasury

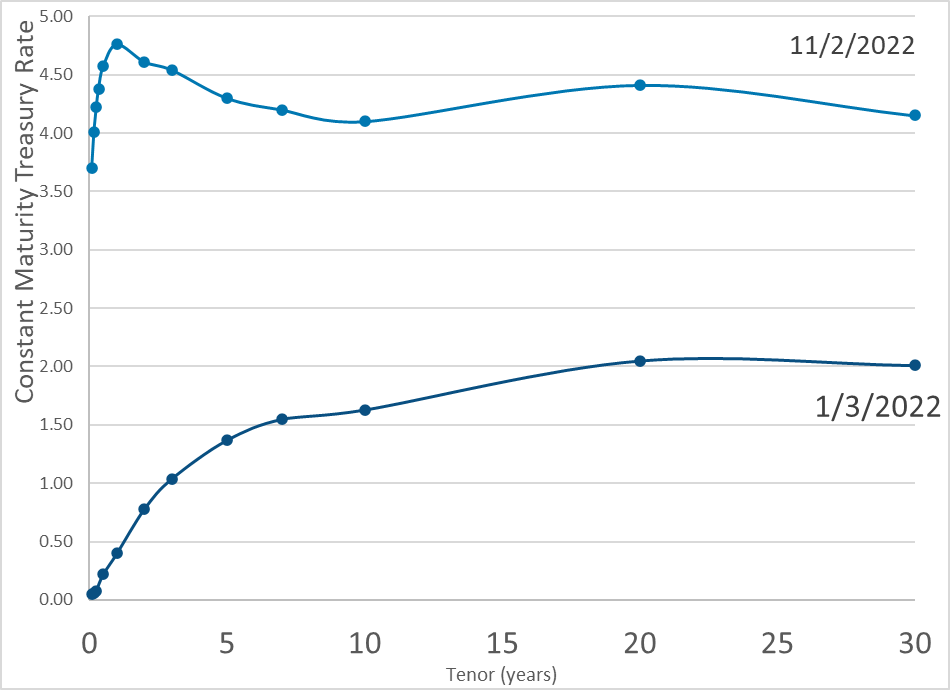

Graphic:

Publication Date: 2 Nov 2022

Publication Site: Dept of Treasury

Link: https://www.ai-cio.com/news/why-bond-liquidity-may-be-headed-for-trouble/

Excerpt:

Reduced liquidity for bonds is getting to be a problem, according to Treasury Secretary Janet Yellen.

At a speech before the Securities Industry and Financial Markets Association annual meeting Tuesday, she reiterated an earlier observation that diminished ability to sell bonds is worrisome. Still, at SIFMA, she sought to temper her concern by adding that traders aren’t facing snags executing orders, with the biggest negative impact of lessened liquidity confined to higher transaction costs.

…..

The gauge for bond volatility, the Merrill Lynch Option Volatility Estimate, aka MOVE index, has jumped some 40% since mid-August. Other than a spike in March 2020 at the onset of the pandemic, the index (it launched in 2019) has been fairly placid—until 2022 and the beginning of big rate hikes. This all is reminiscent of the stock market’s fast-paced volatility lately.

Another related difficulty for bonds: the imbroglio resulting from the Federal Reserve’s interest rate increases and the resulting strong dollar risk worldwide. That has promoted a rush by other central banks to match the Fed and jack up rates. To Richard Farr, chief market strategist at Merion Capital, one risk of this trend is that Treasury bonds will end up hurt.

Author(s): Larry Light

Publication Date: 26 Oct 2022

Publication Site: ai-CIO

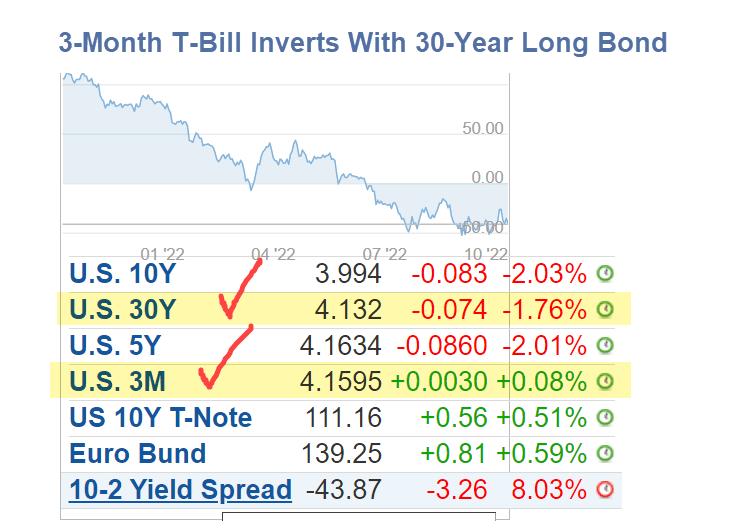

Link: https://mishtalk.com/economics/the-3-month-t-bill-yield-inverts-with-the-30-year-long-bond

Graphic:

Excerpt:

The 3-Month T-Bill yield hit 4.22% early this morning. At that time the 3-Month to 30-Year inversion was about 9 basis points.

The chart above still shows the inversion, just a bit less.

So much for the idea the Fed would steepen the curve.

Author(s): Mike Shedlock

Publication Date: 1 Nov 2022

Publication Site: Mish Talk

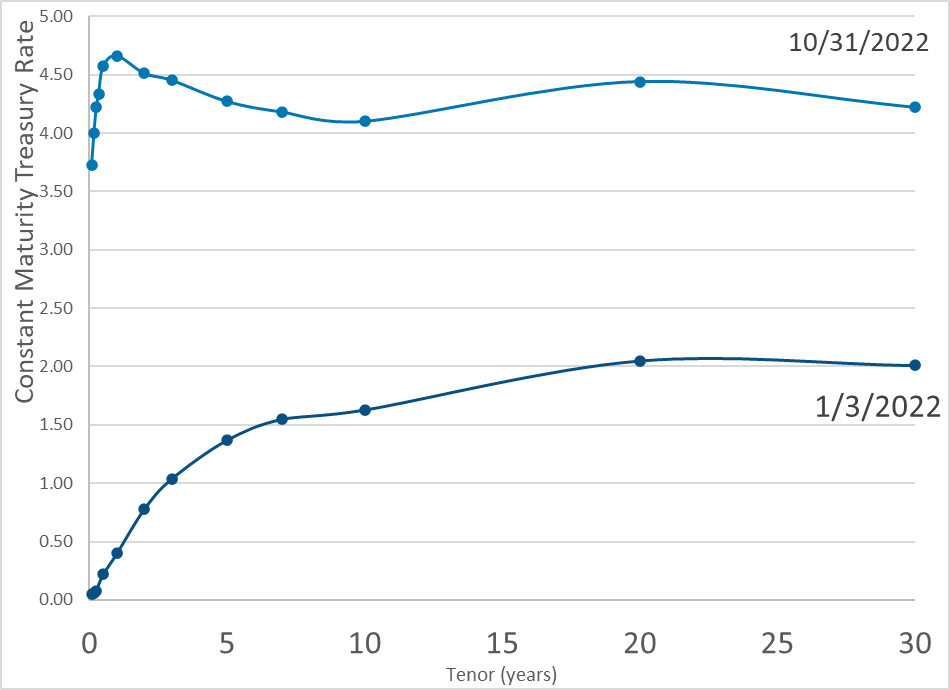

Graphic:

Publication Date: 31 Oct 2022

Publication Site: Treasury Dept

Graphic:

Publication Date: 28 Oct 2022

Publication Site: Dept of Treasury

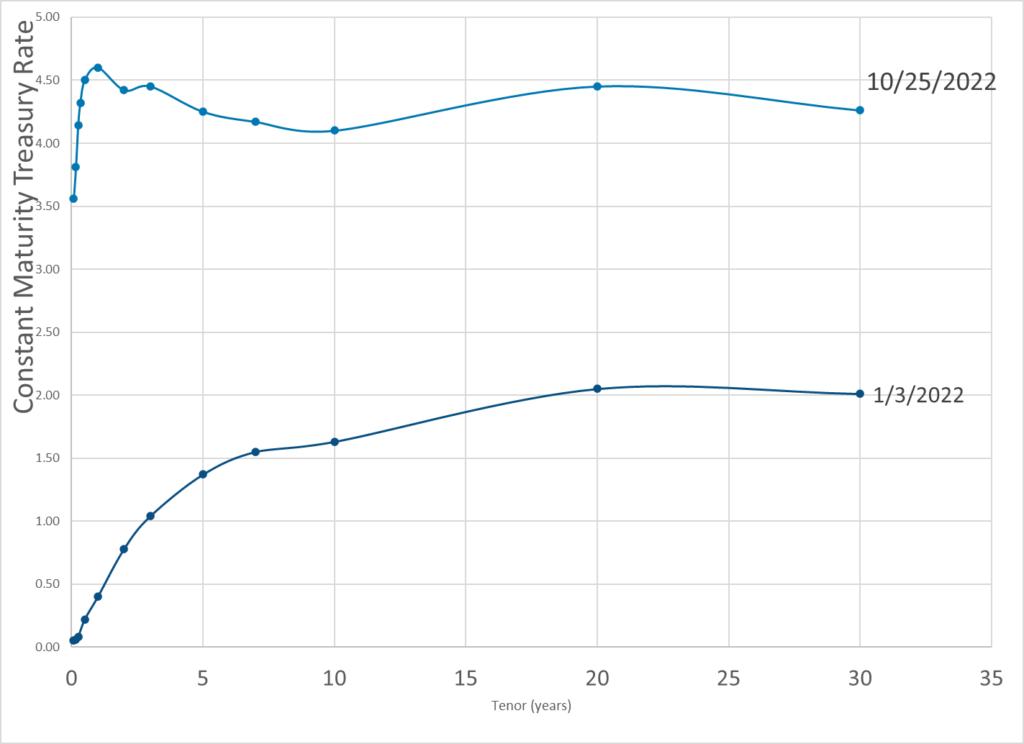

Graphic:

Publication Date: 25 Oct 2022

Publication Site: Dept of Treasury

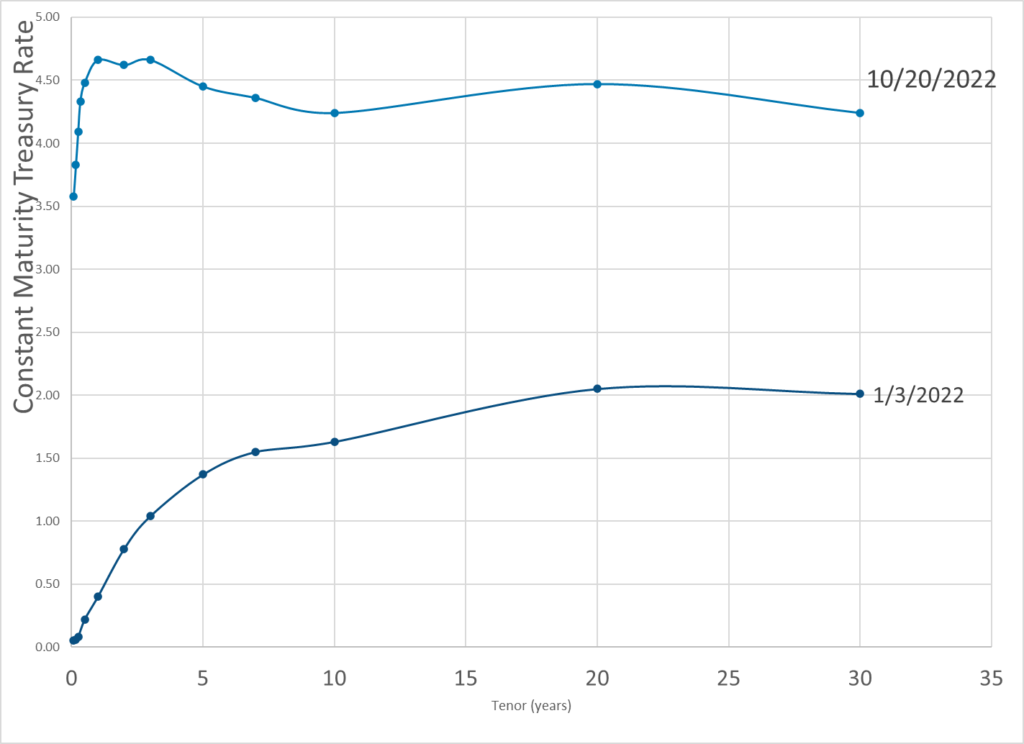

Graphic:

Publication Date: 20 Oct 2022

Publication Site: Dept of Treasury

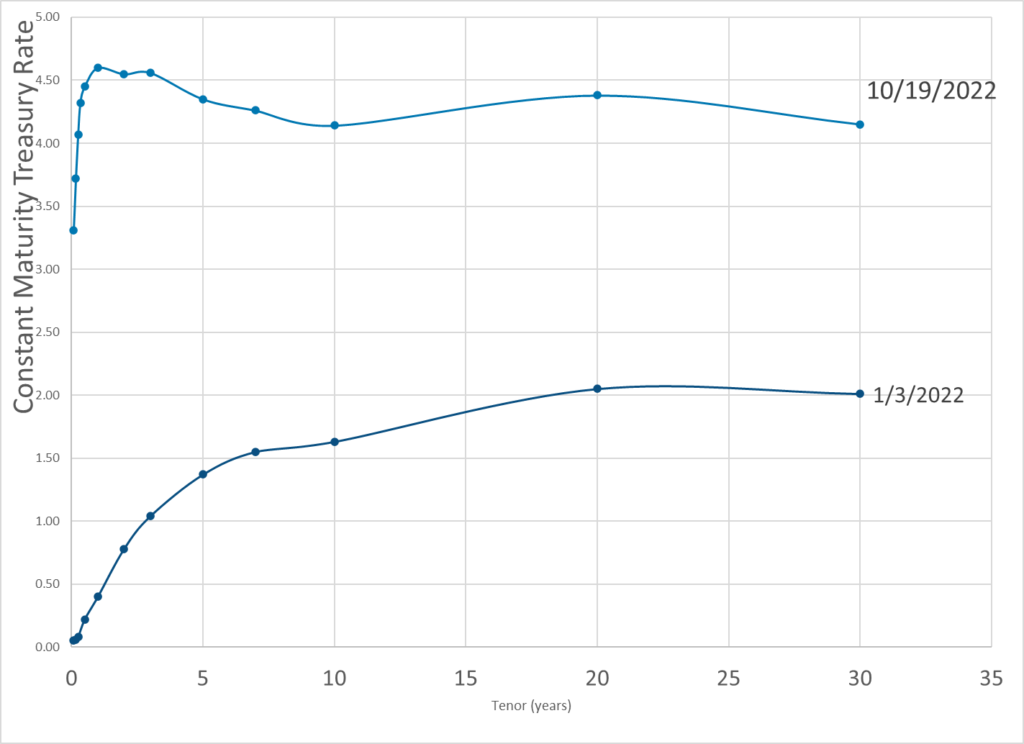

Graphic:

Publication Date: 19 Oct 2022

Publication Site: Dept of Treasury

Link: https://lotsmoore.co.uk/why-do-pension-schemes-use-liability-driven-investment/

Excerpt:

Liability-driven investment allows schemes to invest in the growth assets they need to close the funding gap while reducing the impact of interest rates on the liabilities. This is achieved by assigning a portion of a portfolio to an LDI fund. Rather than this fund just holding gilts, it holds a mixture of gilts and gilt repos.

A gilt repo is re-purchase agreement. The LDI manager sells a gilt to a counterparty bank while arranging to buy back that gilt at a later date for an agreed price. This gilt repurchase agreement provides cash to the pension scheme which it can then use to invest in other assets.

This mixture of gilts and gilt repos in an LDI fund uses leverage to provide capital to the pension fund. It is akin to using a mortgage to buy a house. Different levels of leverage were available in the funds – the more leverage, the greater the ratio of gilt repos to gilts in a fund.

The more leverage in a fund, the less capital a pension scheme had to lock up in government debt and the more it could use to invest in assets which could help to close its funding gap. This was helpful when interest rates were low but became problematic when gilt yields rose.

Author(s): Charlotte Moore

Publication Date: 17 Oct 2022

Publication Site: Lots Moore

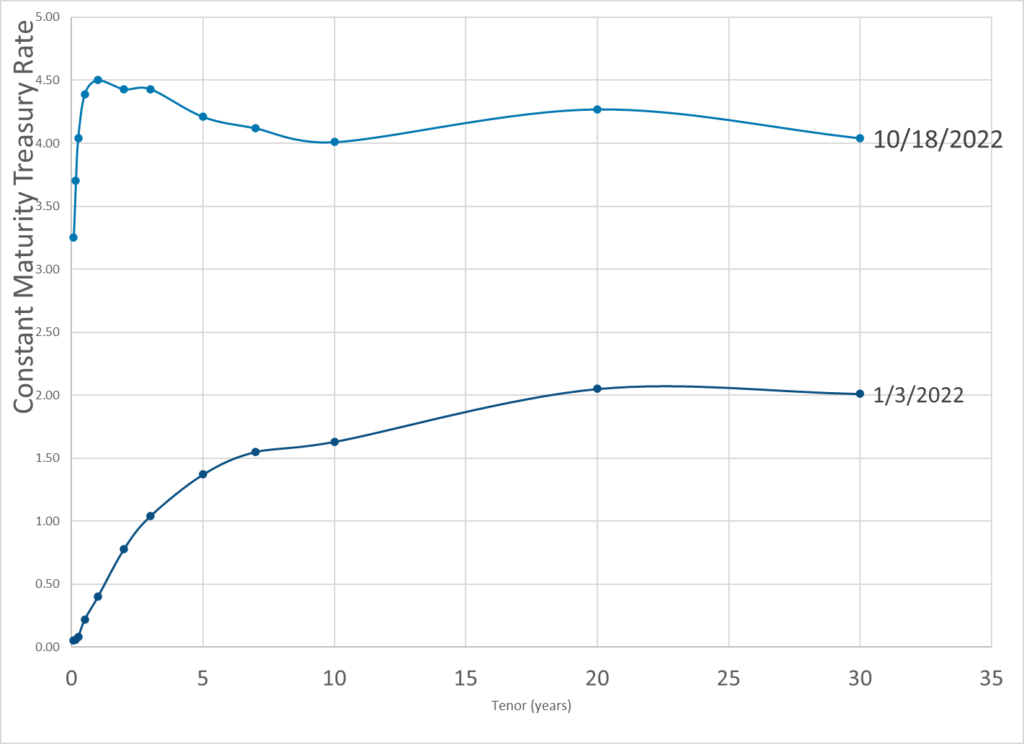

Graphic:

Publication Date: 18 Oct 2022

Publication Site: Dept of Treasury

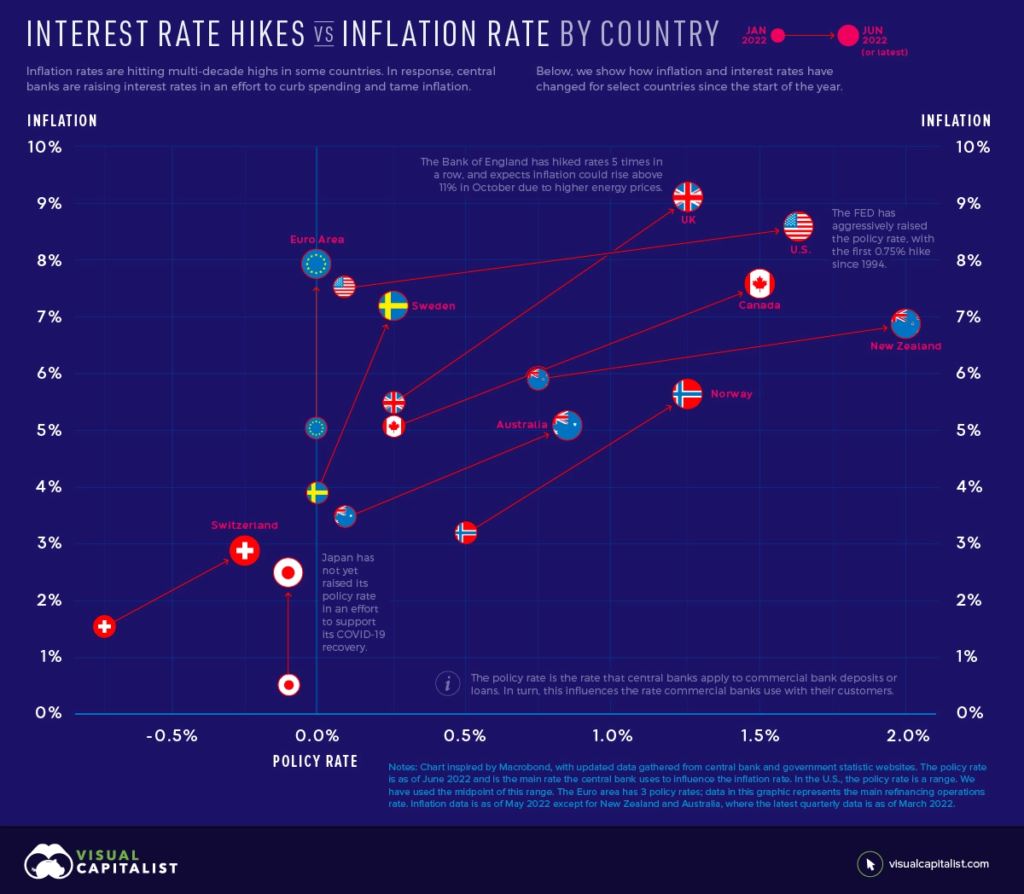

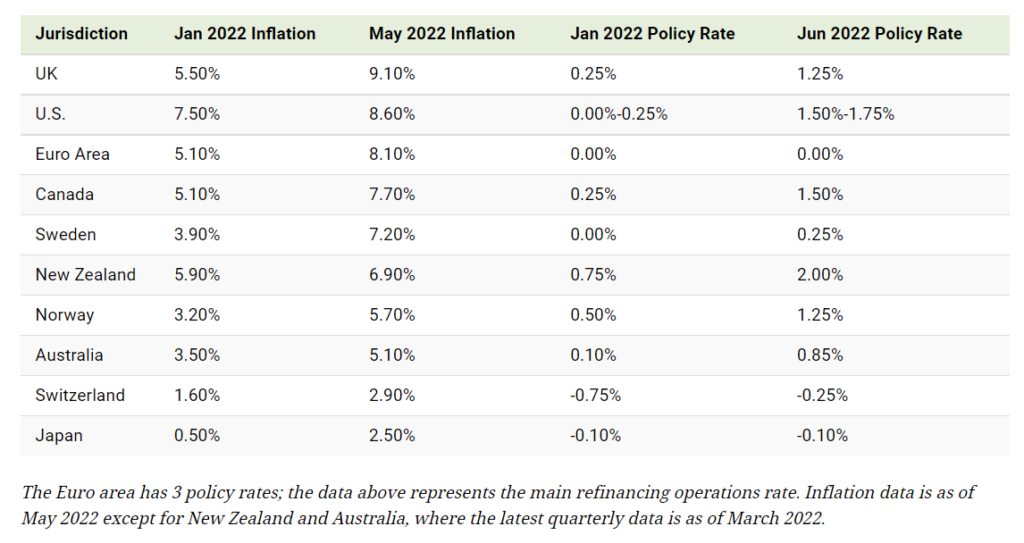

Link: https://www.visualcapitalist.com/interest-rate-hikes-vs-inflation-rate-by-country/

Graphic:

Excerpt:

To understand how interest rates influence inflation, we need to understand how inflation works. Inflation is the result of too much money chasing too few goods. Over the last several months, this has occurred amid a surge in demand and supply chain disruptions worsened by Russia’s invasion of Ukraine.

In an effort to combat inflation, central banks will raise their policy rate. This is the rate they charge commercial banks for loans or pay commercial banks for deposits. Commercial banks pass on a portion of these higher rates to their customers, which reduces the purchasing power of businesses and consumers. For example, it becomes more expensive to borrow money for a house or car.

Ultimately, interest rate hikes act to slow spending and encourage saving. This motivates companies to increase prices at a slower rate, or lower prices, to stimulate demand.

Author(s): Jenna Ross, Nick Routley

Publication Date: 24 June 2022

Publication Site: Visual Capitalist