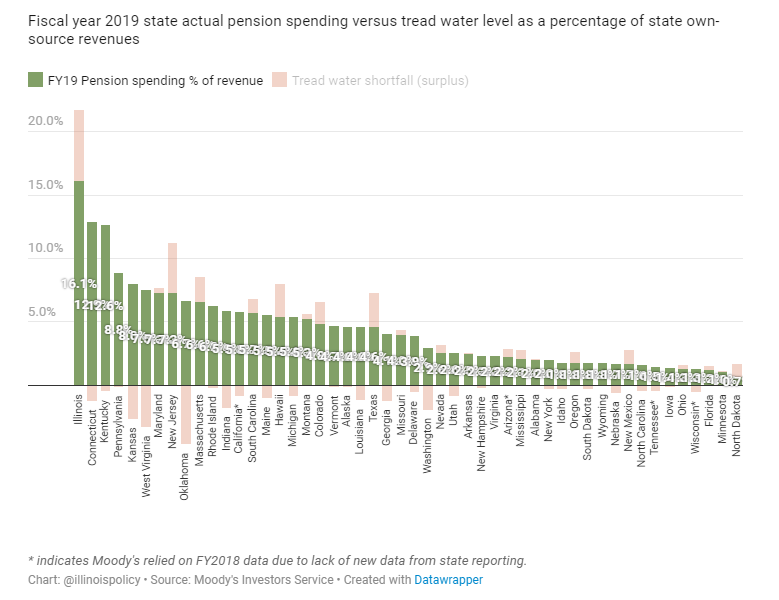

Despite the record increase in pension expenditures in the past several decades, Illinois’ pension system remains the nation’s worst by multiple measures. According to Moody’s Investors Service, Illinois’ pension debt was equal to 500% of the state’s revenues in fiscal year 2018 and almost 30% of the entire state economy, both the highest rates in the nation. At the same time, Illinois’ credit rating has been in precipitous decline and now sits at the lowest credit rating in the nation.

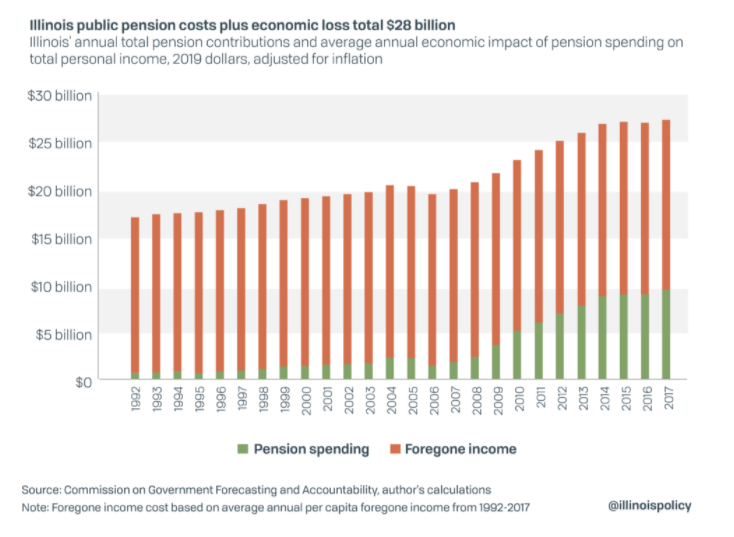

As pension debt continues to increase, so do required pension contributions. Pension contributions now consume 26.5% of the state’s general funds budget, up from less than 4% during the years 1990 through 1997.

Pension costs are already eating away at Illinois government services. The ballooning costs caused a nearly one-third cut since 2000 in core services such as child protection, state police, mental health and college money for low-income students.

Pension contributions accounted for less than 4% of Illinois’ general funds budget from 1990 through 1997 but have grown to consume 28.5% of the budget. Still, the pension debt has mushroomed to $144.4 billion by the state’s estimates, which more realistically was at an all-time high of $261 billion at the end of fiscal year 2020 according to Moody’s Investors Service calculations using more realistic assumptions. In any case, public pension debt is eating a larger chunk of Illinois’ gross domestic product than anywhere else.

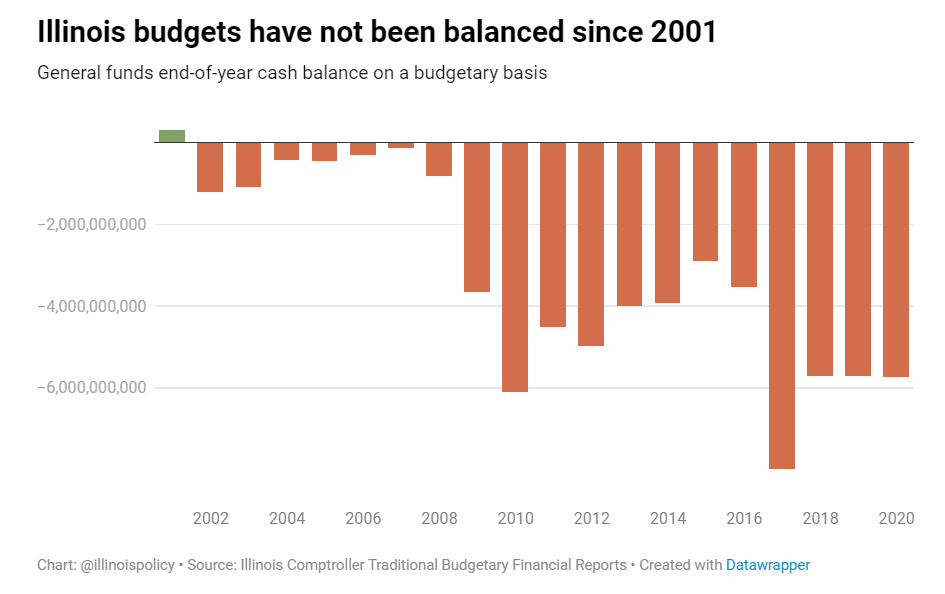

Bad accounting has helped Illinois politicians avoid balancing the budget for 20 years, despite a constitutional requirement to pass a balanced budget each year. Government accounting standards that fail to offer transparency and accuracy in financial reporting have also contributed to the state’s $260 billion pension crisis, the primary reason Illinois has the lowest credit rating any state has ever received.

The Governmental Accounting Standards Board has proposed changes it calls “improvements” to the accounting standards for governments. However, watchdog groups such as Truth in Accounting have criticized the proposed changes and urged the adoption of more stringent standards that would require governments to balance their budgets the way most businesses are required to do. Illinois has grown accustomed to using lax accounting methods to hide its budget deficits, racking up debt year after year. The state’s taxpayers would benefit from tougher standards that impose fiscal discipline.

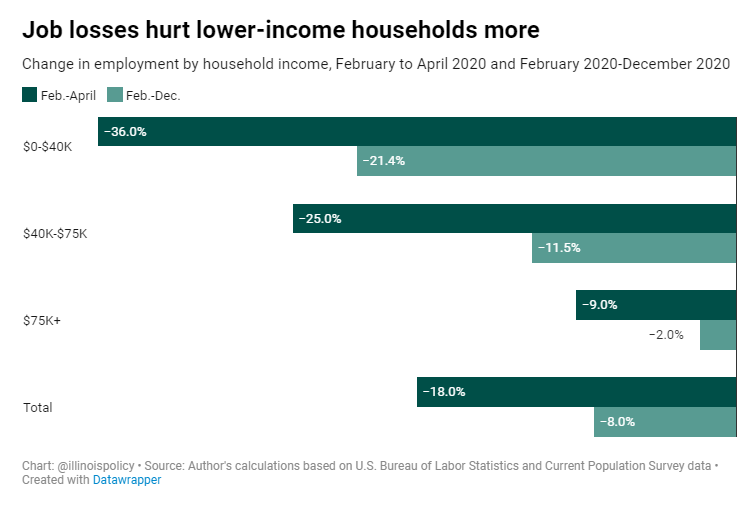

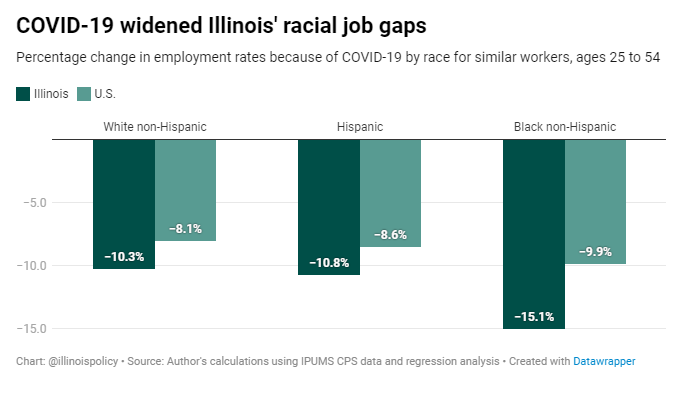

Illinois households earning less than $40,000 were four-times as likely to lose their jobs from February-April 2020 and nearly 11 times as likely to still be out of work compared to those earning $75,000 or more.

As Illinois tries to rebuild after the worst year for jobs in state history, low-income Illinoisans find themselves even farther behind than others. Job losses suffered during COVID-19 and state-mandated mitigation protocols disproportionately fell on these families.

Bad accounting has helped Illinois politicians avoid balancing the budget for 20 years, despite a constitutional requirement to pass a balanced budget each year. Government accounting standards that fail to offer transparency and accuracy in financial reporting have also contributed to the state’s $260 billion pension crisis, the primary reason Illinois has the lowest credit rating any state has ever received.

The Governmental Accounting Standards Board has proposed changes it calls “improvements” to the accounting standards for governments. However, watchdog groups such as Truth in Accounting have criticized the proposed changes and urged the adoption of more stringent standards that would require governments to balance their budgets the way most businesses are required to do. Illinois has grown accustomed to using lax accounting methods to hide its budget deficits, racking up debt year after year. The state’s taxpayers would benefit from tougher standards that impose fiscal discipline.

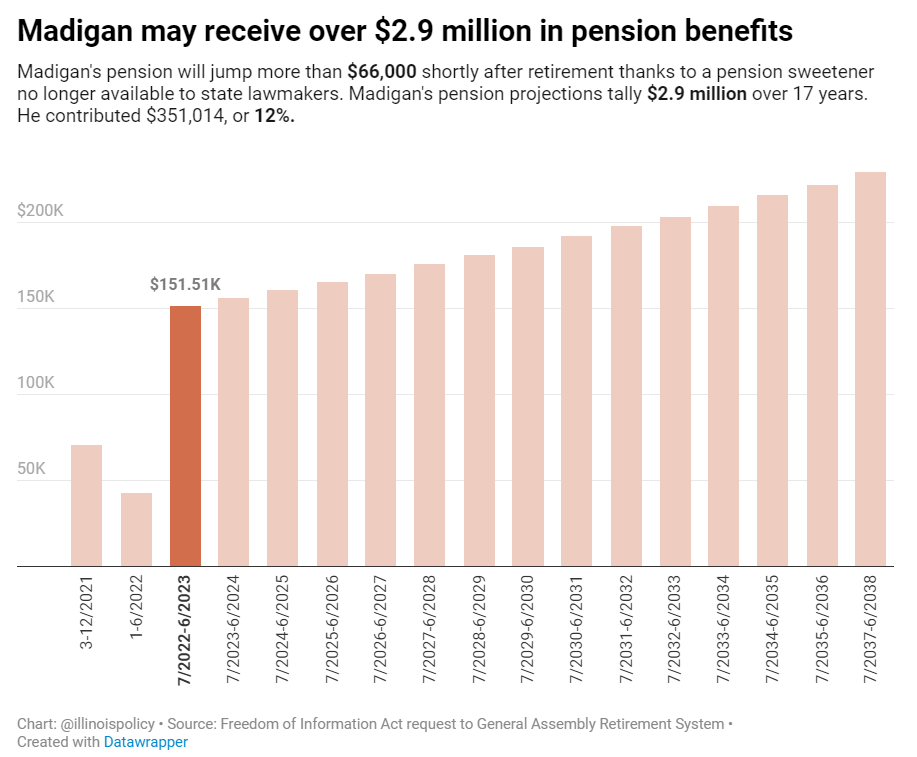

Because of a pension sweetener for politicians that Madigan helped create, the former speaker’s pension will spike more than $66,000 the year after his first full year of retirement, then grow 3% each year thereafter.

Former Illinois House Speaker Michael J. Madigan will start receiving $7,100 in monthly pension benefits starting in March, but just more than a year later his benefits jump 78% to $12,600 per month.

Pension debt increased $7.1 billion to $144.4 billion in fiscal year 2020, according to the Commission on Government Forecasting and Accountability, or COGFA, the fiscal analysis unit for the General Assembly. The total cost of that debt burden to taxpayers in fiscal year 2022 will be nearly $11.6 billion, including:

$9.4 billion in direct contributions from general revenue sources

$1.1 billion in “other state funds”

$797.9 million in debt service costs on previously issued pension obligation bonds

$264.8 million towards the Chicago Teachers’ Pension Fund, or CTPF

Pensions will consume 28.5% of the budget. That is based on $38.5 billion in expected general revenue for fiscal year 2022, adding in that $1.1 billion from “other state funds” – which would go to critical programs were it not being used for pension debt.

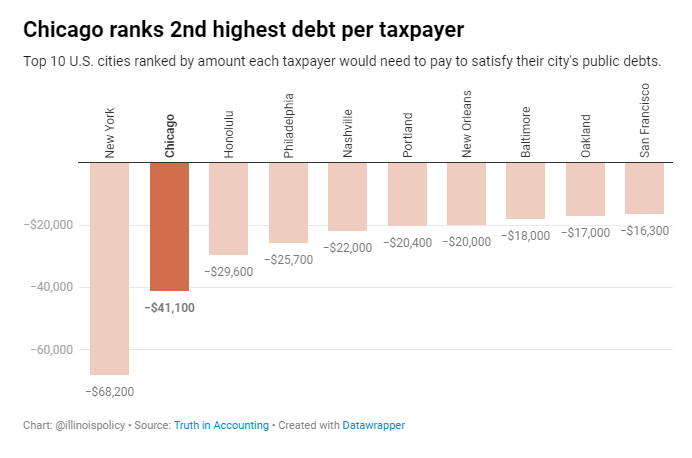

A new report from government finance watchdog Truth in Accounting gave the Windy City an “F” for financial health. Chicago’s massive $36 billion net debt stems primarily from pensions.

Chicago city taxpayers were just hit with $94 million in property tax increases and $38 million in higher fines and fees, including a policy for speed cameras to ticket drivers for going just 6 mph over the speed limit, to help close the city’s budget deficit. City leaders placed much of the blame on COVID-19’s impact on government revenues, but a recent report from fiscal watchdog Truth in Accounting shows Chicago’s problems existed long before the pandemic.

In addition to Illinois being home to the second-highest property taxes in the country, one of the most painful facts about owning a home here is that tax dollars don’t go to the services people expect and value.

Increase the public pensions funding target to 100% from 90% in accordance with actuarial best practices. The goal year for 100% funding would remain 2045.

Gradually increase retirement ages for current workers under age 45 by a maximum of five years.

Apply a pensionable salary cap of $100,000 that grows with inflation. Government workers could still earn more than $100,000, but their pensions could not be based on more than the cap. The cap would only apply to employees not currently receiving a retirement check.

Replace Tier 1 retirees’ 3% compounding benefit increase with true cost-of-living adjustments tied to inflation. Annual increases would be simple, not compounding, and rise with the consumer price index for urban consumers, as reported by the U.S. Bureau of Labor Statistics.

Increase Tier 2 COLAs from half of inflation to full inflation. This would end the unfair subsidization of older workers by younger workers and could prevent a potential lawsuit.

Implement COLA holidays to allow inflation to catch up to past benefit increases. If a worker has been retired for eight years or more, they would skip every other year for 16 years for a total of eight adjustment periods at 0%. If a retiree has been receiving benefits for seven years, they would skip one payment every other year for 14 years, and so on.

Enroll all newly hired employees in a defined contribution personal retirement account with a 4% guaranteed employer match. This would ensure the state never gets into pension trouble again. This would also provide state workers with a portable retirement benefit they could take with them from employer to employer, rather than being forced to stay with the state in order to maximize retirement benefits.