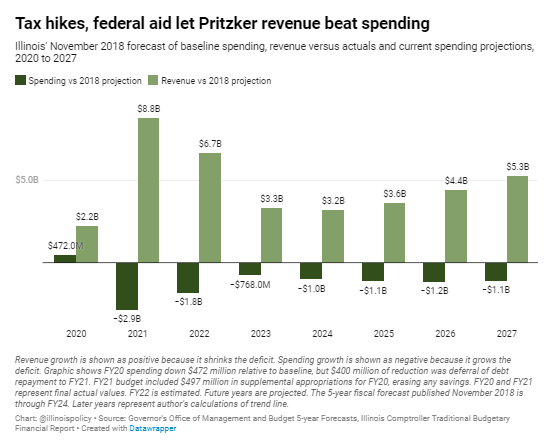

Spending in the state budget actually has increased – significantly – under Gov. J.B. Pritzker relative to baseline expectations in the state budget. Even if lawmakers and the governor make no further increases to spending in the fiscal year 2023 budget, which is unlikely given that Pritzker has proposed spending increases in each February budget address of his term, then total spending during Pritzker’s first term will be up nearly $5 billion, or 3% higher than when he took office.

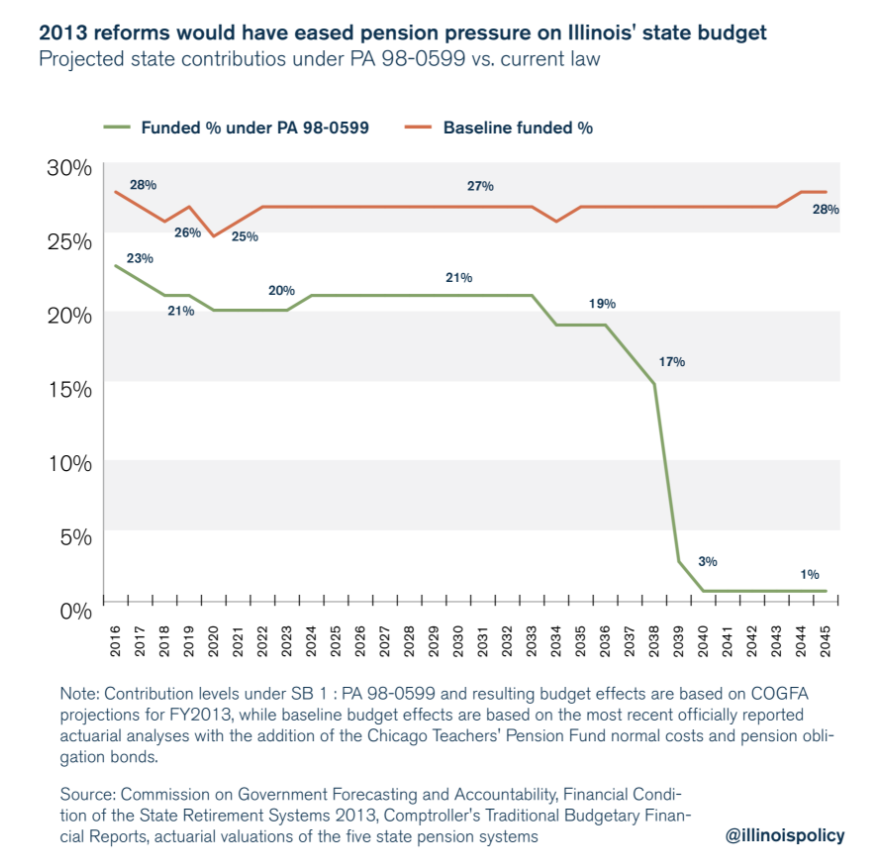

Illinois allocates more of its budget to pensions than any other state, but pension spending has only skyrocketed. A constitutional amendment is the only way to reform the state’s unsustainable and underfunded pension systems.

Daley College Professor Mike Crenshaw is far from retirement, but he constantly worries whether the State Universities Retirement System will be solvent for him.

“I have 20 years until I can retire, and my biggest fear is that the money’s not going to be there,” Crenshaw said.

….

Because pension benefits are defined in the Illinois Constitution, only a constitutional amendment approved by voters could change pension structures. Amending the constitution would open the door to changing the compounding raises to simple inflationary adjustments – protecting the systems for retirees and ending the excessive drain on taxpayers.

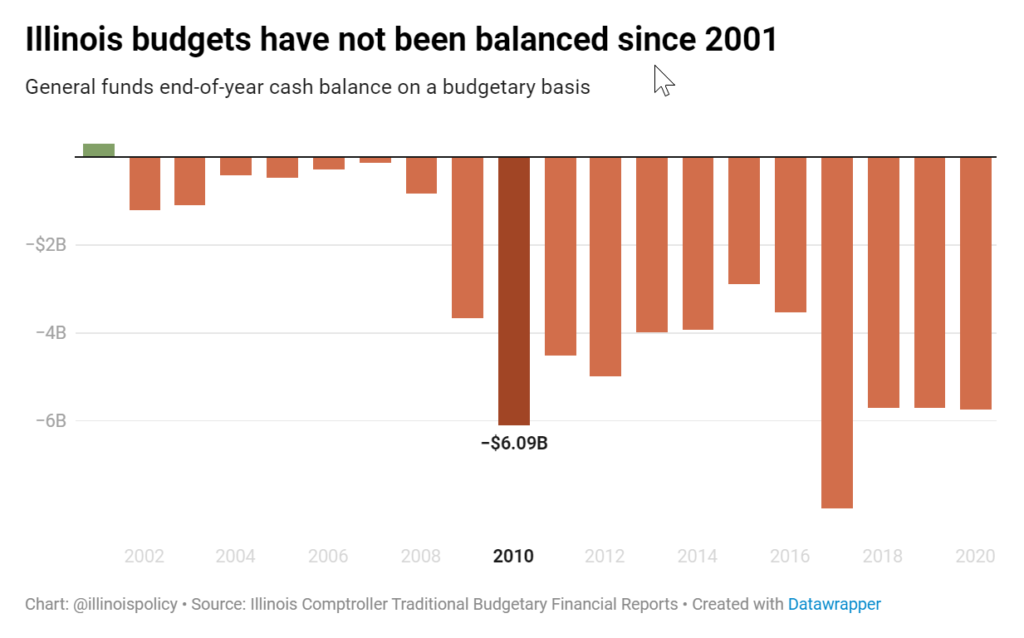

From 2005-2019, Illinois revenues totaled just 94% of expenses. The state ran deficits in each of the 15 years prior to the COVID-19 pandemic. Only New Jersey overspent more.

Illinois was one of only eight states to see spending outpace its revenues from 2005-2019, leaving it fiscally ill-prepared to deal with the tumultuous COVID-19 pandemic, according to new data from The Pew Charitable Trusts.

Illinois ranked No. 2 for overspending.

According to the report, Illinois took in just 94.1% of the revenues it needed to cover its expenses from 2005-2019. That number was second worst in the nation, coming in just ahead of similarly troubled New Jersey.

It is bad Illinois has the nation’s worst pension crisis, but state politicians have made it worse by using risky debt to delay the day of reckoning, and done so to the point that Illinois now owes 30% of the nation’s pension obligation bonds.

Pension obligation bonds are a form of debt used by state or local governments to fund their pension deficits. Illinois holds $21.6 billion of the nation’s $72 billion pension obligation bond debt.

The theory behind the bonds is that if a pension system can borrow money at a lower rate by selling bonds and earn a higher percentage from investing those funds, then it has realized a net gain using them. The issue is the gamble rarely works out that way, as the Government Finance Officers’ Association points out. Pension obligation bonds place taxpayer money at risk and often leave governments saddled with more debt rather than less. They often do not achieve a high enough return to justify their use.

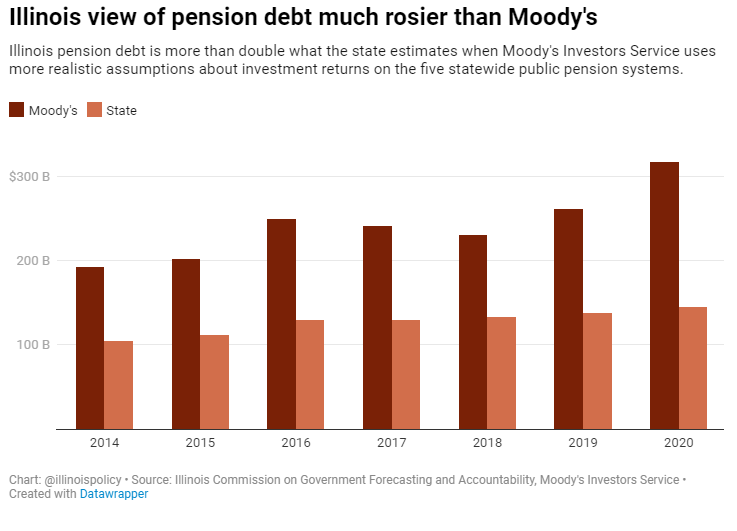

Illinois’ five statewide retirement systems hold $144 billion in debt, according to official state reporting based on optimistic investment estimates. But Moody’s Investors Service says the true debt is $317 billion, which it calculates using more accurate methods common in the private sector.

Illinois missed the September deadline to repay a $4.2 billion federal unemployment loan. Employers warn inaction by state lawmakers could ‘cripple’ businesses and the COVID-19 economic recovery.

Illinois state leaders missed the Sept. 6 deadline to repay a $4.2 billion federal loan to the state’s unemployment insurance fund, which leaves Illinois taxpayers on the hook to pay $60 million in annual interest on that loan.

The unemployment fund has been depleted during the COVID-19 economic downturn. Between the loan and failure of state leaders to replenish the fund, potentially by using federal COVID-19 bailout funds, the deficit stands at $5.8 billion.

Business leaders warn a failure to repay the debt would result in automatic tax hikes on Illinois’ employers starting at $500 million, further waylaying the state’s stagnant job recovery. There would also be automatic benefit cuts of the same amount. Employers could be subjected to further, discretionary tax hikes by the state legislature if those automatic solvency measures fail to fill the hole.

Author(s): Adam Schuster, Patrick Andriesen, Perry Zhao

A new report shows Illinois holds 30% of the nation’s pension obligation bond debt.

A pension obligation bond is a form of debt that some states use to make payments to state-run pension funds. A pension obligation bond gets paid out by a third party and the state then pays back that loan with interest. Financial experts often advise against the use of pension obligation bonds, said Adam Schuster of the Illinois Policy Institute.

….

The interest on the pension obligation bonds continues to climb and is leaving Illinois in a worse spot than it was previously in. The state has borrowed a total of $17.2 billion since 2003, but repayment cost is now $31 billion. Pension obligation bonds can save taxpayers money if the interest rates on the bonds is lower than the rate of return on the pension investments. If the rate of return drops below the interest rate on the bonds, then taxpayers are on the hook for the difference. This is a strategy that Schuster said is the same as gambling with the state’s money.

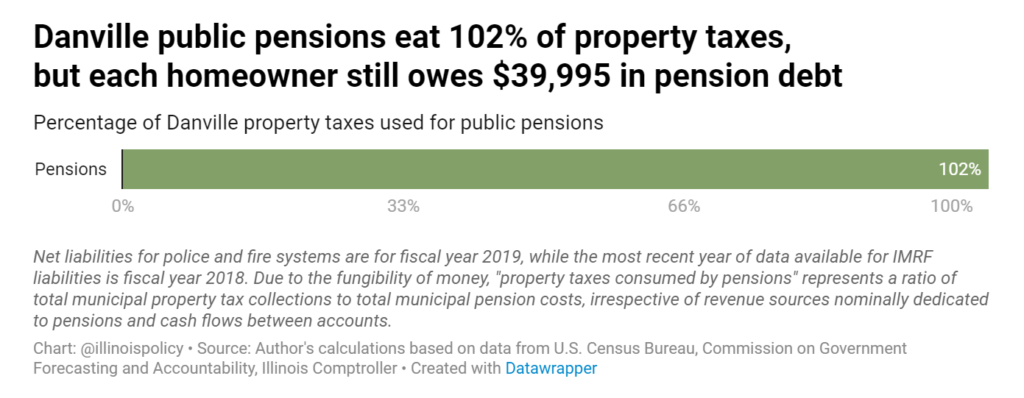

The average Danville household owns nearly $40,000 in state and local pension debt.

Illinois’ worst-in-the-nation pension debt has become a well-known problem. Over $144 billion in pension debt for the five statewide retirement systems breaks down to nearly $30,000 in debt for each household, which must be paid with further tax hikes or further cuts to core government services.

Less well known is the nearly $75 billion of pension debt held by local governments in Illinois, which is the primary reason for Illinois’ second-highest in the nation property taxes. Combined with the state’s pension debt, politicians who mismanaged the pension system dug a $219 billion hole.

In Danville, the average household owns nearly $40,000 in state and local pension debt, with over $10,000 of that debt stemming from local systems for police, firefighters and municipal workers. To pay off that pension debt, a Danville household would have to give up 110% of an entire year’s $36,172 median annual income.

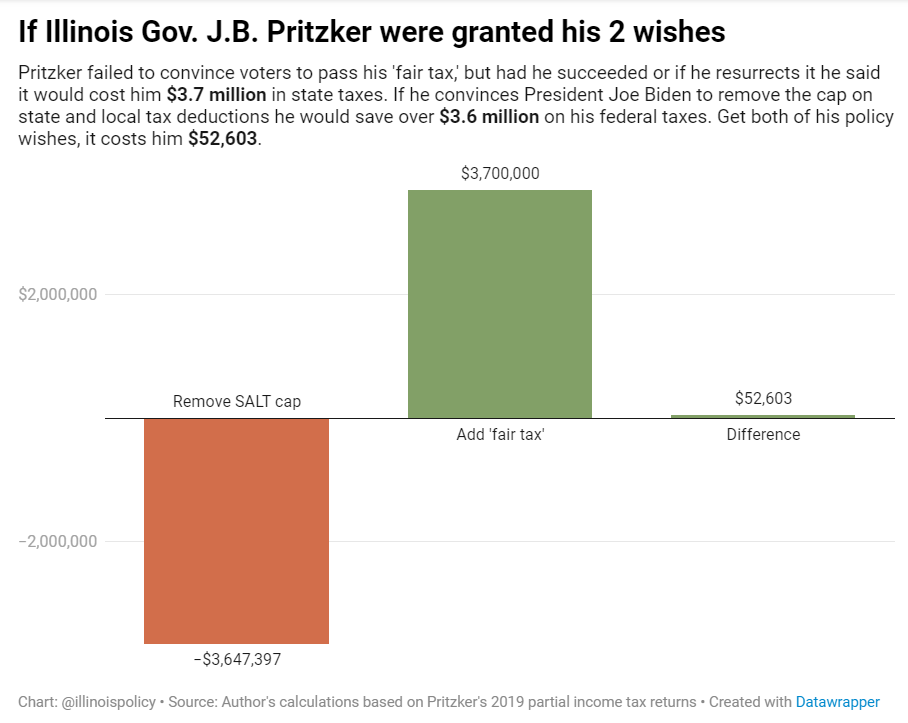

Of course, no one can know the true extent to which Pritzker has been able to reduce his tax bills through loopholes and carve-outs over the years, because he refuses to release his full tax returns. In recent years it has been revealed Pritzker went to great lengths to avoid paying taxes, removing toilets from his Gold Coast mansion to skimp on his property tax bill by $331,000 and establishing shell corporations in the Bahamas in a likely attempt to avoid U.S. income taxes. The toilet ploy earned him a federal investigation.

The letter, which pushes for tax reforms that would almost exclusively benefit the wealthy, comes less than six months after Pritzker’s progressive income tax amendment was rejected by voters and is a significant departure from his previous stance on taxation. In the letter, Pritzker claims the cap hurts middle-class taxpayers and is “untenable” during these dire economic times. Because the data is clear on who directly benefits from the SALT deduction, one can only assume the governor is implying higher taxes on the wealthy also hurt Americans with lower incomes.

That is precisely the argument opponents of the “fair tax” made after the governor first unveiled his tax-the-rich scheme in 2019.

Ousted Illinois House Speaker Michael Madigan collected his first public pension check March 24 for $7,093, or $85,117 a year, but he won’t have to worry about it becoming a fixed income.

A year from July Madigan’s state pension shoots up to $148,955 thanks to a pension sweetener no longer available to state lawmakers. That 75% bump results from a provision that once allowed lawmakers to “bank” 3% cost-of-living increases while still working for each year of service after 20 years or age 55, whichever comes first. Madigan “banked” 25 years of increases, according to the General Assembly Retirement System.

Because Madigan, 78, retired after Jan. 1, he will receive the benefits boost starting July 1, 2022. The sweetener will also allow former Senate President John Cullerton to retire with a pension that will spike to $128,000 just a couple of years into retirement. The perk was discontinued for lawmakers elected after 2002.

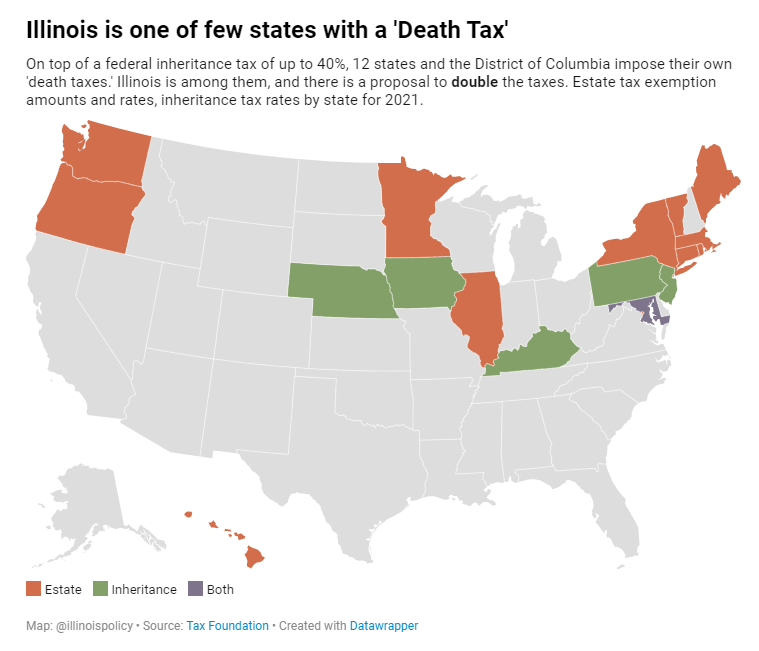

Many states have moved away from taxing assets after people die because of the harm to family businesses and farms, but a new proposal before state lawmakers would double Illinois’ estate tax.

House Bill 3920 would hike the existing state tax on estates of over $4 million to 9.95% from 4.95%. Unlike neighboring Wisconsin, Michigan, Indiana and Missouri, Illinois is one of just a dozen states that still have an estate or inheritance tax. Tax Foundation analyst Katherine Loughead noted, “The top marginal estate tax rate under this proposal would become the highest in the country at 21%.”

While the bill’s sponsors intend the extra revenues to be used to support Illinoisans with disabilities, hiking the estate tax would squeeze family farmers, reduce the accumulation of productive assets, encourage spendthrift behavior, fuel tax avoidance and evasion, and drive wealth to other states.

Tillman, of suburban Golf, centered his claims on Article IX Section 9(b) of the Illinois state constitution. Tillman argued that provision of the state constitution limits the state’s ability to borrow money.

The complaint particularly focuses on text requiring lawmakers to identify “specific purposes” for debt when issuing new long-term bonds. Tillman argues that “specific purposes” clause should be read to forbid state lawmakers from borrowing money to finance deficits or “plug holes” in the state’s budget, such as the shortfall faced by the state when funding pension obligations.

Tillman has argued lawmakers in both 2003 and 2017 failed to identify “specific purposes” when it issued bonds, and then unconstitutionally assigned to the state comptroller the power to decide how the borrowed money was spent.

Because the state systemically underestimates its pension debt, it also underestimates the taxpayer contributions necessary to keep the debt from growing each year. During the past decade, officially-reported growth in pension debt outpaced the state’s initial projections by $24 billion. Growth in annual taxpayer contributions exceeded state estimates by about 15% per year on average, causing taxpayers to contribute $7.6 billion more than projected during the decade. Still, that extra money has not slowed a mushrooming pension debt. The state’s regular upward revisions demonstrate Moody’s method, which is more in line with private sector standards, is more accurate.

Because employee contributions to the pension funds and benefits paid out are both fixed by state law, taxpayers must make up for any shortfall caused when investment returns miss rosy targets. For example, the largest of Illinois’ five state pension systems, the Teachers’ Retirement System, reported a 0.52% return on investment in fiscal year 2020, which included the first four months of the COVID-19 pandemic. That was far short of the TRS’s 7% return target and helped grow the debt.