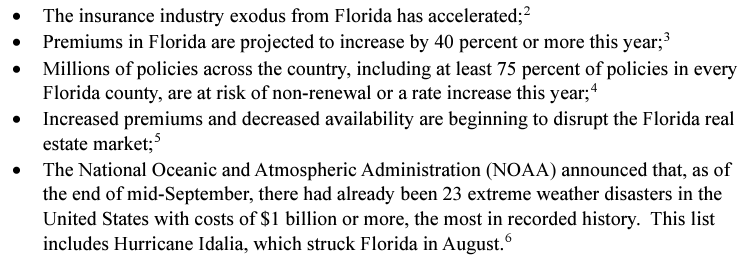

Insurance prices have surged across America in the past two years, with homeowner’s insurance climbing 21%, while CPI rose just 5%. (Source: Bloomberg)

Jerry Theodorou of R Street Institute is interviewed about Florida homeowners insurance.

Most insurance companies at that time assessed hurricane exposure in their portfolios by simply multiplying customer premiums by a rough factor of supposed risk, rather than tracking actual property replacement costs. “They were just very crude formulas,” she said.

So in 1987, Clark had started her own company, Applied Insurance Research, or AIR, to develop software that better estimated the potential losses from catastrophic events. Unlike the rest of the industry, she used granular data and sophisticated analyses, an approach now called catastrophe modeling. Her first computer model estimated that a Category 5 hurricane hitting Dade County could cause losses almost 10 times more than previously believed. She warned her customers about the risk in Florida, but until Hurricane Andrew, no one listened.

The federal government has launched an investigation into Florida’s largest home insurance company.

Citizens Insurance, the governor, and other state leaders received a letter informing them that a Senate budget committee is looking into the state-run company.

Citizens insure $586 billion worth of property, and they have just over $15 billion in their reserves to pay out on claims. If a major hurricane hit the state, they could be short over $571 billion, leaving everyone in the state on the hook to pay the shortfall.

The letter from the Senate committee investigating the state backed company expresses concern it may be unable to cover its losses. A claim the governor confirmed while visiting Fort Myers last year.

….

Mark Friedlander with the Insurance Information Institute said a private insurer would not be allowed to operate in the State of Florida with those financial dynamics.

Seven private companies went insolvent in the last year and a half in Florida.

“Citizens, unlike a private insurer, could never go insolvent,” Friedlander noted.

That’s because the state could initiate a hurricane tax to cover its costs which would require everyone who owns property or a car to pay a hurricane tax.

As of 2022, Citizens’ market share for homeowners multi-peril policies was approaching 20 percent, having more than doubled since 2020. As private insurers in Florida continue to go insolvent or exit the state, Citizens’ market share will likely continue to grow. At 20 percent market share, Citizens’ losses could be as high as $36 billion in the scenario studied by Swiss Re or $162 billion in the scenario studied by Cambridge and Munich Re (assuming that 60 percent of total losses are insured). If Citizens had to raise $162 billion to cover losses, that would result in an approximately $20,000 assessment for every homeowners insurance policyholder in Florida.

….

To that end, please respond to the following requests for information and documents by December 21, 2023:

1. What modeling or other analysis has Citizens done to estimate its total potential exposure to various worst case hurricane scenarios? What is the upper range of Citizens’ potential losses? Please provide all documents and communication relating to modeling, analysis, and estimates of Citizens’ potential losses.

2. What modeling or other analysis has Citizens done to estimate its market share over the next decade? What does Citizens project its market share to be in each of the next 10 years? Please provide all documents and communication relating to modeling, analysis, and estimates of Citizens’ future market share.

3. What modeling or other analysis has Citizens done to determine its ability to fully pay out claims resulting from various loss scenarios? Please provide all documents and communication relating to modeling, analysis, and estimates of Citizens’ financial position and (in)solvency under such scenarios.

4. What are Citizens’ current assets? What is Citizens’ total reinsurance coverage? What are the maximum total claims Citizens would be able to pay out without having to levy an assessment on Florida policyholders? Please provide all documents and communication relating to modeling, analysis, and estimates of Citizens’ current assets, reinsurance, and ability to pay claims.

5. What communications has Citizens had with Governor DeSantis, Insurance Commissioner Michael Yaworsky, their staffs, or any other state officials regarding Citizens’ current or future solvency? Please provide copies of these communications.

6. What communications has Citizens had with Governor DeSantis, Insurance Commissioner Yaworsky, their staffs, or any other state officials regarding what Citizens and/or the State would do if Citizens were unable to cover its losses? Please provide copies of these communications.

7. Has Citizens contemplated asking for a federal bailout if it were unable to cover its losses? Has Citizens discussed the possibility of a federal bailout with Governor DeSantis, Insurance Commissioner Yaworsky, their staffs, or any other state officials? Please provide copies of these communications.

In a typical year, about 100 storms and tropical disturbances develop in the Atlantic Ocean, Caribbean Sea and Gulf of Mexico. Some of these turn into tropical storms, and on average, two each year become hurricanes that make landfall in the U.S.40 Between 1851 and 2016, 289 hurricanes affected the continental U.S. Of these, 63 made landfall in Texas.41

….

Of course, hurricanes and other major storms affect the entire country, not just the Gulf Coast. Exhibit 6 lists the most destructive storms affecting the U.S. in the last half-century.

Hurricane Katrina, which caused $161.3 billion in damages, still ranks as the costliest storm in American history; Hurricane Harvey is expected to rank second, with total estimated damages of about $125 billion.45

Publication Date: February 2018, accessed April 2023

Publication Site: Fiscal Notes, Comptroller of Texas

Logging and landscaping are the most dangerous jobs in America, a new study finds.

The risk of death for loggers is more than 30 times higher than for all U.S. workers. Tree care workers also encounter hazards at rates far higher than a typical worker.

….

For the study, the researchers combed a U.S. Occupational Safety and Health Administration database for deaths from tree felling between 2010 and the first half of 2020.

Over the period, Michael’s team found 314 deaths. The leading cause of fatal accidents was being struck by a tree, most often in the head.

….

Years such as 2012, 2017 and 2018 with abnormally high damage from Atlantic storms saw high numbers of landscaping deaths that might be tied to storm damage, while 2014 and 2015 had quiet hurricane seasons and few deaths.