Insurance prices have surged across America in the past two years, with homeowner’s insurance climbing 21%, while CPI rose just 5%. (Source: Bloomberg)

Jerry Theodorou of R Street Institute is interviewed about Florida homeowners insurance.

The insurance industry is unique in that the cost of its products—insurance policies—is unknown at the time of sale. Insurers calculate the price of their policies with “risk-based rating,” wherein risk factors known to be correlated with the probability of future loss are incorporated into premium calculations. One of these risk factors employed in the rating process for personal automobile and homeowner’s insurance is a credit-based insurance score.

Credit-based insurance scores draw on some elements of the insurance buyer’s credit history. Actuaries have found this score to be strongly correlated with the potential for an insurance claim. The use of credit-based insurance scores by insurers has generated controversy, as some consumer organizations claim incorporating such scores into rating models is inherently discriminatory. R Street’s webinar explores the facts and the history of this issue with two of the most knowledgeable experts on the topic.

Author(s): Jerry Theodorou, Roosevelt Mosley, Mory Katz

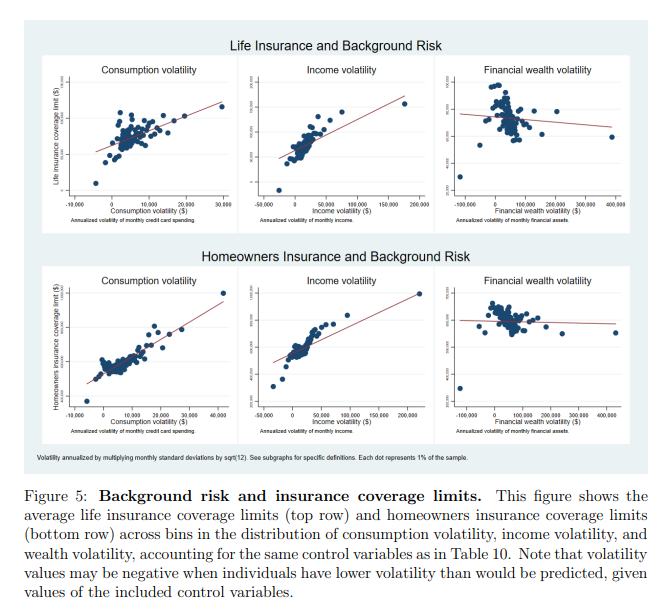

Theoretically, wealthier people should buy less insurance, and should self-insure through saving instead, as insurance entails monitoring costs. Here, we use administrative data for 63,000 individuals and, contrary to theory, find that the wealthier have better life and property insurance coverage. Wealth-related differences in background risk, legal risk, liquidity constraints, financial literacy, and pricing explain only a small fraction of the positive wealth-insurance correlation. This puzzling correlation persists in individual fixed-effects models estimated using 2,500,000 person-month observations. The fact that the less wealthy have less coverage, though intuitively they benefit more from insurance, might increase financial health disparities among households.