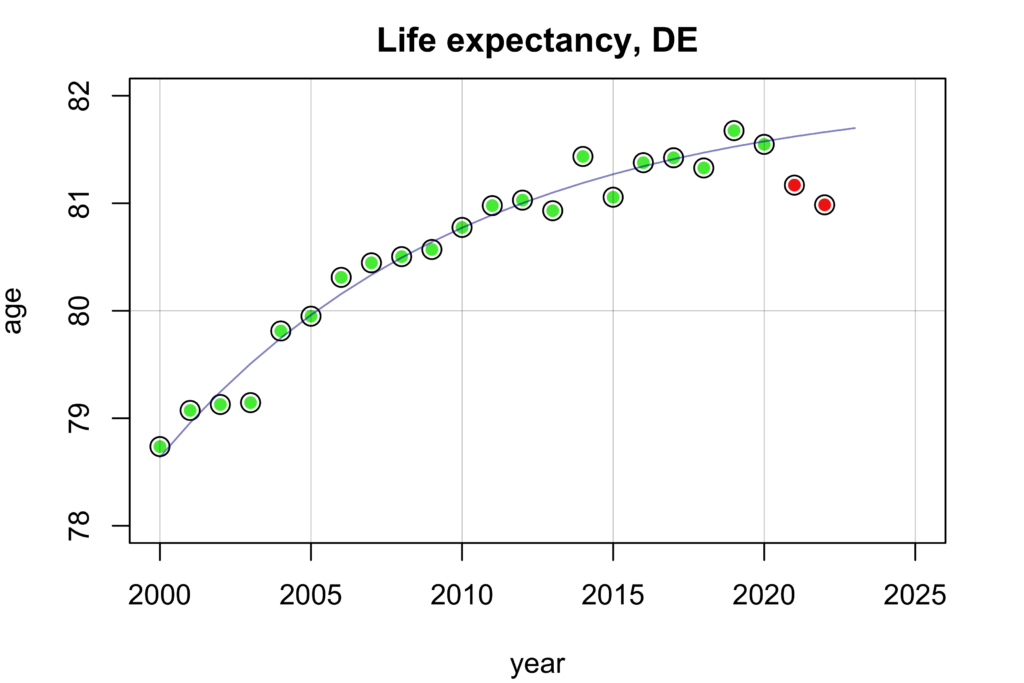

Fig. 1: Annual values of life expectancy in Germany with fit (blue). The fit did not respect the values for 2021 and 2022.

Excerpt:

Life expectancy is relatively difficult to calculate. The mortality risk has to be determined from death and population figures for each individual year of life. A hurdle is that data are often only available in age cohorts. So the missing values have to be interpolated. Using the mortality risks, a fictitious newborn cohort is projected forward year by year until all have died. A weighted average value is calculated from those who died each year in this modeled time series, yielding the life expectancy.

Life expectancy in Germany increased for many years until 2020, allthough this trend seemed to be gradually approaching a saturation point, which might be around 82 years (Fig. 1).

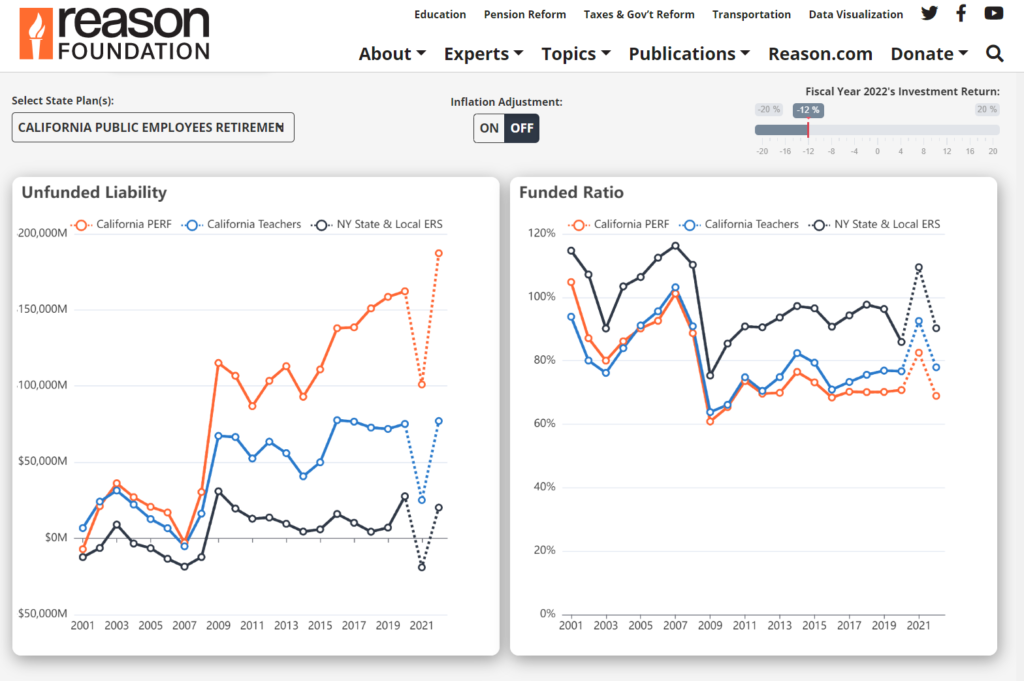

According to forecasting by Reason Foundation’s Pension Integrity Project, when the fiscal year 2022 pension financial reports roll in, the unfunded liabilities of the 118 state public pension plans are expected to again exceed $1 trillion in 2022. After a record-breaking year of investment returns in 2021, which helped reduce a lot of longstanding pension debt, the experience of public pension assets has swung drastically in the other direction over the last 12 months. Early indicators point to investment returns averaging around -6% for the 2022 fiscal year, which ended on June 30, 2022, for many public pension systems.

Based on a -6% return for fiscal 2022, the aggregate unfunded liability of state-run public pension plans will be $1.3 trillion, up from $783 billion in 2021, the Pension Integrity Project finds. With a -6% return in 2022, the aggregate funded ratio for these state pension plans would fall from 85% funded in 2021 to 75% funded in 2022.

Author(s): Truong Bui, Jordan Campbell, Zachary Christensen