Link: https://bellwethereducation.org/publication/retirement-systems-ranking

Graphic:

Excerpt:

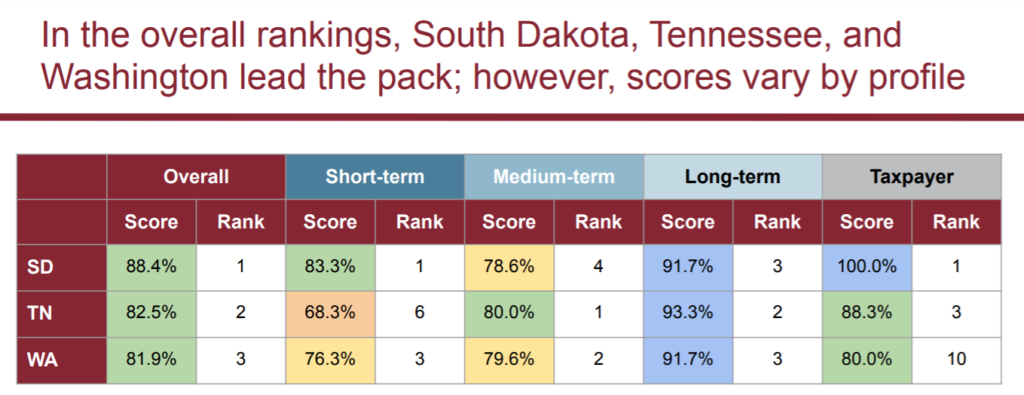

Teacher retirement plans are called “gold plated” by their proponents and critics alike, when in fact half of teachers will never see a pension at all. Only about one in five teachers gets a full pension. And in many cases retirement benefits shortchange teachers and make it harder for them to save for their retirement.

In Teacher Retirement Systems: A Ranking of the States, Bellwether Education Partners ranks how state retirement systems serve U.S. teachers and taxpayers:

….

Retirement programs don’t serve all teachers equitably. For teachers who work in the classroom for fewer than 10 years, 34 states receive an “F” for how well retirement plans prepare them for retirement. For teachers who work in the classroom for more than 10 years, but do not stay until retirement age, 23 states receive an “F” ranking.

Link to full report: https://bellwethereducation.org/sites/default/files/Teacher%20Retirement%20Systems%20-%20A%20Ranking%20of%20the%20States%20-%20Bellwether%20Education%20Partners%20-%20FINAL.pdf

Author(s):

MAX MARCHITELLO

ANDREW J. ROTHERHAM

JULIET SQUIRE

Publication Date: 31 August 2021

Publication Site: Bellwether Education Partners