Graphic:

Excerpt:

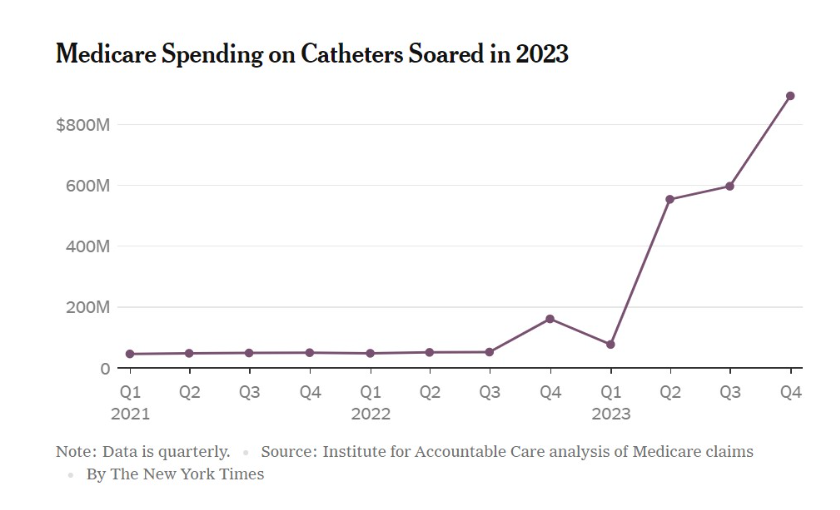

The New York Times reported recently about a sharp spike in Medicare spending on catheters, amid numerous signs that scammers have targeted that benefit to bilk the government out of taxpayer funds. With Medicare rapidly approaching insolvency, the problem is twofold: Criminals still consider the program such an easy source of cash — because the feds do such a poor job at finding and catching the crooks.

Times reporters interviewed several seniors explaining how they had been billed for catheters they never received and do not need or use. It also noted that the number of Medicare beneficiary accounts billed for catheters rose roughly nine-fold last year, from 50,000 to 450,000.

The pattern of Medicare spending on catheters echoes the increase in beneficiaries billed. Based on this graph from the Times story, it doesn’t take a doctorate in economics to realize that something fishy has happened regarding payments for catheters — and that, assuming most or all of the increase is due to fraud, Medicare has already given the scammers billions of dollars.

Over and above whether and when the feds can catch the scammers, the real question is: How did this happen? Or, given the federal government’s history of permitting fraud in federal health care programs, how does this keep happening?

Author(s): Christopher Jacobs

Publication Date: 16 Feb 2024

Publication Site: The Federalist