The Chicago City Council approved a casino development in the River West neighborhood. The generated revenue will exclusively pay for pension debt, but only an estimated 9% of what the city needs.

The Chicago City Council approved a $1.7 billion casino in a 41-7 vote May 25. The River West development is being touted as a pension solution, but even the highest projections show only a drop in the bucket.

“This one casino project will pay for approximately 9% of our $2.3 billion pension contribution and reduce the likelihood that the city will need to raise property taxes in the future for pensions,” said Jennie Huang Bennet, chief financial officer for the city.

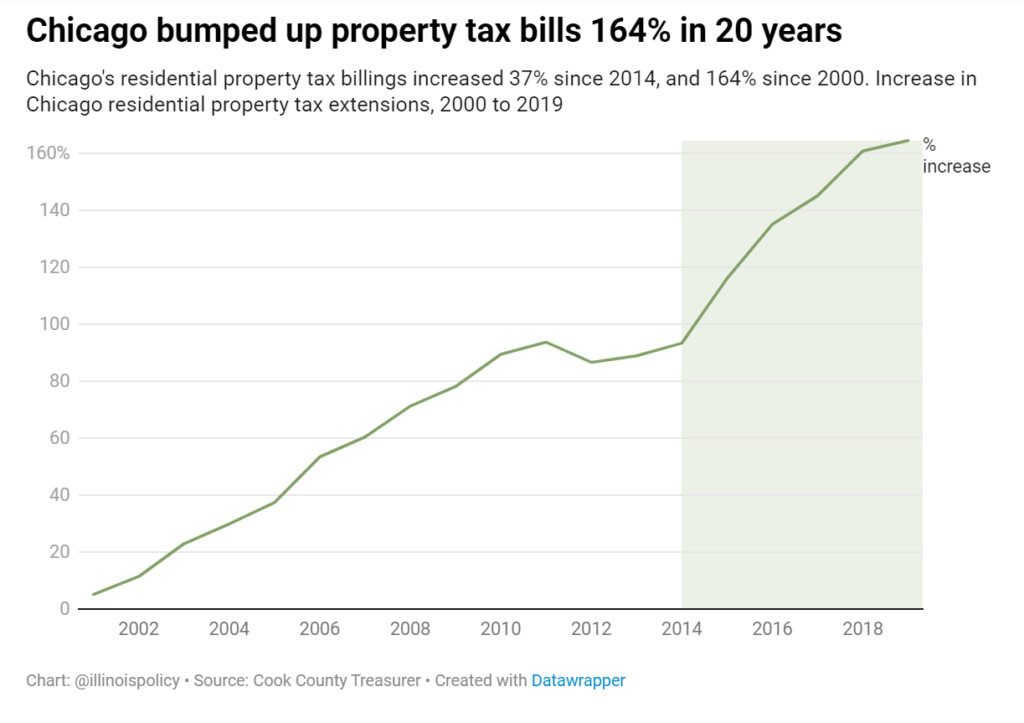

Chicago residential property tax collections across all units of government in the city were up 164% from 2000 to 2019.

Property taxes paid by homeowners within the city grew nearly 30% faster than property taxes in suburban Cook County during those 20 years. Suburban residential property taxes grew 116% while total residential property tax collections county-wide grew 133%.

While some of Chicago’s increase was driven by new property or growth in existing property tax values, the average homeowner still saw an 85% increase in their bill from 2000 to 2019. Since the record-setting 2015 property tax hike to pay for pension debt, the average Chicago bill has risen 27%. Prior to that hike, property taxes were on a lower trend from 2011 to 2014.

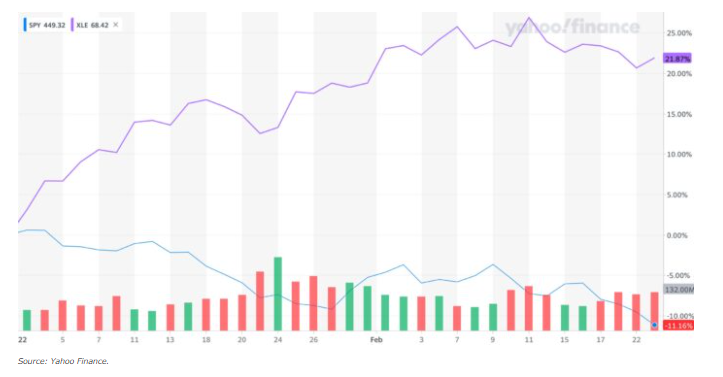

The timing on Wednesday was impeccable. I was looking at the price of oil, which was up four percent that day and about to pass $100/barrel. Energy stocks were up over one percent despite a horrible day for the rest of the market.

So, with inflation raging, gasoline moving towards $4.00/gallon and Russia murdering Ukrainians with the help of American oil purchases, Chicagoans can take comfort knowing that the city will refuse to invest in oil and other fossil fuel production and thereby “will be sending a message that Chicago is permanently leaving dirty energy in the past and welcoming a clean energy future for generations to come.”

That’s from Chicago Treasurer Melissa Conyears-Ervin. She and members of the City Council, with Mayor Lori Lightfoot’s support, are pushing for an ordinance to mandate that the city divest its funds from fossil fuel companies, as Crain’s reported.

In fact Conyears-Ervin had already made oil and gas divestment office policy. The new ordinance would make the change permanent going forward. Her office has already removed $70 million in fossil fuel-associated bonds from the city’s portfolio, she says.

How wise has it been lately to be shunning fossil fuel investments? Here’s a chart comparing performance year-to-date of the S&P 500 to XLE, an ETF basket of mostly oil and gas companies. While the market in general is down some 10% the oil and gas stocks are up over 21%.

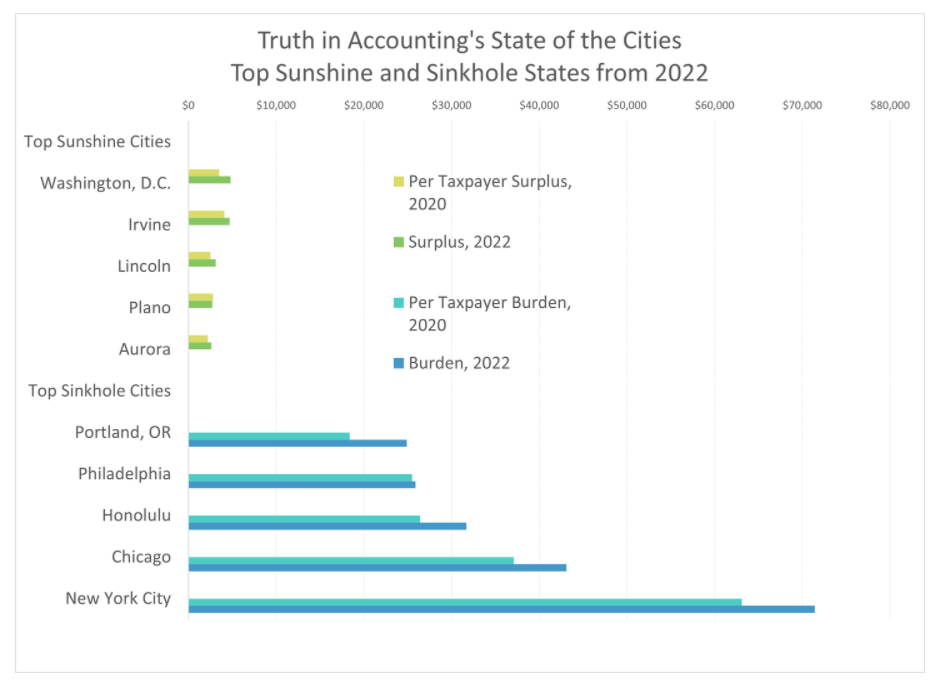

Chicago once again earned a failing grade from Truth in Accounting in their latest Financial State of the Citiesreport thanks to over $38 billion in debt – $43,100 for each taxpayer.

Every Chicagoan would have to send the city that amount just for Chicago to pay the bills it owes. Chicago has just $9.9 billion available to pay $48.6 billion in bills. The Windy City came in 74th out of 75 cities studied in the report, only besting New York City’s massive $204 billion debt with a per-taxpayer burden of $71,400.

The city’s financial failings stem from pension promises the city cannot afford to keep. “Chicago’s financial problems stem mostly from unfunded retirement obligations that have accumulated over the years. The city had set aside only 23 cents for every dollar of promised pension benefits and no money for promised retiree health care benefits,” the report notes.

The kinds of messages that are welcomed are “innovative” in terms of telling you that you don’t have to do the thing you really don’t want to do (put more money into the pensions, promise less, cut back on many things, tax more, etc.)

Illinois State Senator Robert Martwick (D-Chicago) is pushing ahead with legislation that, according to a Bloomberg report, could increase Chicago’s police pension obligations by another $3 billion in total through 2055. An earlier city estimate put the cost at $2.1 billion. Senate Bill 2105 would do that by removing a birthdate restriction on eligibility at age 55 for a 3% automatic annual increase in retirement annuity.

Where would Chicago get money to cover the additional liability? No answers.

….

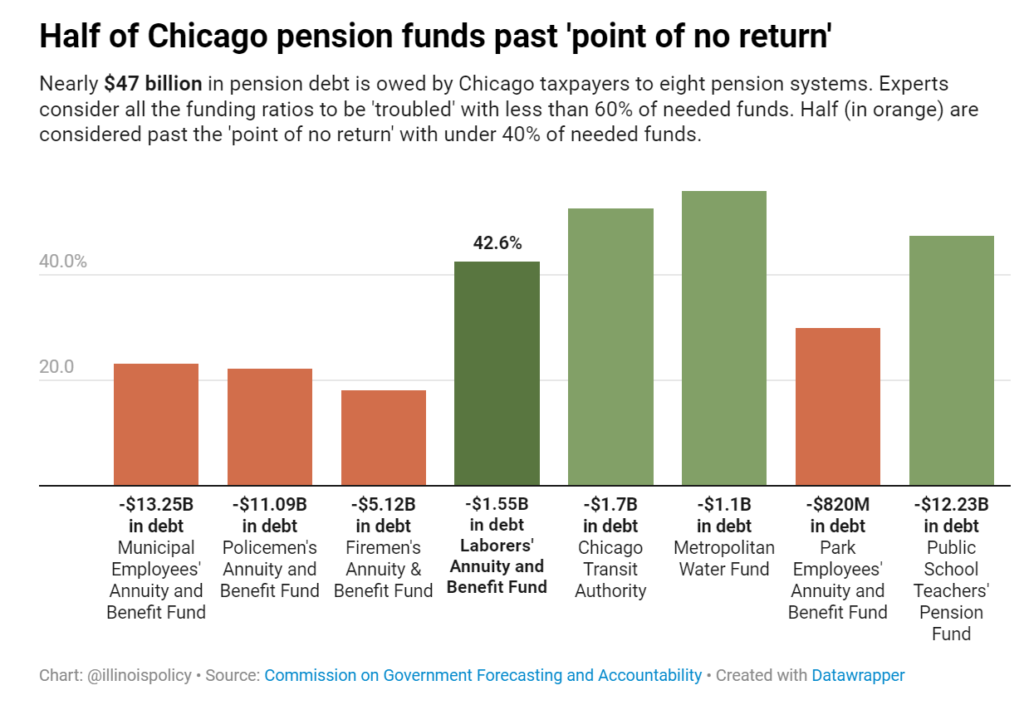

Chicago’s police and firefighter pensions already are in utterly abysmal shape, having just 18% and 23%, respectively, of the assets their actuaries say they should have. Together with two other pensions sponsored by the city, Chicago officially reports about $33 billion of unfunded pension liabilities. But using more realistic assumptions, Moody’s estimates the total unfunded liability at $60 billion. Moody’s also reports the city of Chicago’s total debts as a percentage of annual revenues are at 735%, the highest of any major city in the country.

….

It’s as if Martwick is saying, “We rob banks routinely so you might as well make it legal for us to rob banks.”

Chicago Public Schools’ $872 million of junk-rated paper met with a more fickle high-yield audience this week, underscoring the district?s vulnerability to market volatility even as it inches closer to investment grade status.

At attractive spreads that offered a healthy yield kick with many maturities offering 4% coupons, the bonds were 2.2 times oversubscribed, CPS said in a statement. More than 40 institutional investors placed orders including some in excess of $150 million each.

The district will pay a true interest cost of 3.51% that ranks among the lowest paid by the Chicago Board of Education over the last two decades. The sale provides $500 million of new money for capital projects and the remainder refunds 2011 bonds.

You may recall earlier this year when the General Assembly passed a bill that Gov. JB Pritzker signed to increase certain pension benefits for Chicago firefighters. The new law is expected to cost Chicago some $850 million and could drop the funded status from what was an already abysmal 18% down to an even-worse 16%.

Well, it appears that Illinois Senate leadership didn’t even bother to talk to Chicago Mayor Lori Lightfoot before mandating that additional burden.

The Chicago Tribune has released Lightfoot email and text messages it obtained on a number of matters. One went from Lightfoot to Senate President Don Harmon. “A courtesy call regarding the fire pension bill would have been helpful, particularly since there is no funding for it,” Lightfoot said. “When that pension fund collapses, I will be talking a lot about this vote.”

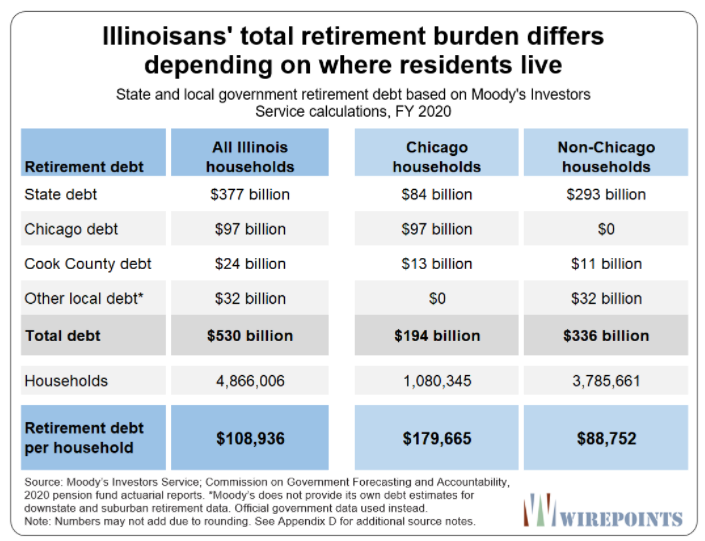

The $110,000 per household is an average across the entire state, but the precise burden for Illinoisans differs depending on where they live. The debt burden on Chicago’s one million households is larger because of the city’s deeper debt crisis. There, each household is on the hook for $180,000 for their share of state and local retirement debts.

Illinoisans living outside of Chicago, meanwhile, face an overall average burden of $90,000 per household. For comparison purposes, the burdens for Chicago and non-Chicago households, based on official state and local retirement debts, are $95,000 and $53,000, respectively.

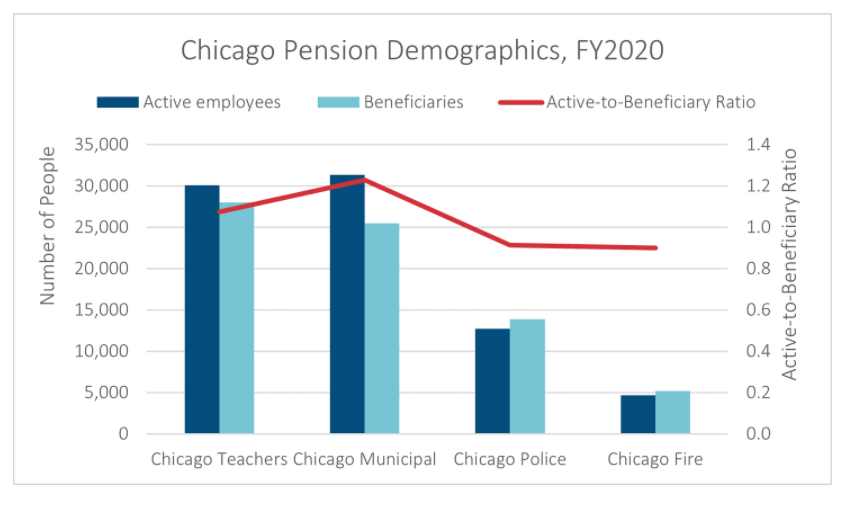

Both Chicago Police and Chicago Fire plans have active-to-beneficiary ratios of about 90%, and have been at that level for some years. Chicago Police, specifically, had such a ratio starting in 2012.

So, there are more people taking police pensions than are active employees already. If I take the numbers given, and shift 38% from active to beneficiaries, that gives one an active-to-beneficiary ratio of 52% (assuming you don’t get new actives, which you would, but still… this is a point-in-time estimate).