The California Public Employees’ Retirement System (CalPERS) has engaged financial services company Jefferies about the potential of selling up to $6 billion of its private equity stakes, according Buyouts magazine. This comes just after CalPERS announced it would be increasing the percentage of its portfolio allotted to private equity to 13% from 8% in November.

CalPERS board member Margaret Brown told Secondaries Investor in November that the fund is considering investing in secondaries and divesting from some of its legacy private equity investments.

“We have some really old private equity that’s just sitting there and doing nothing,” she said.

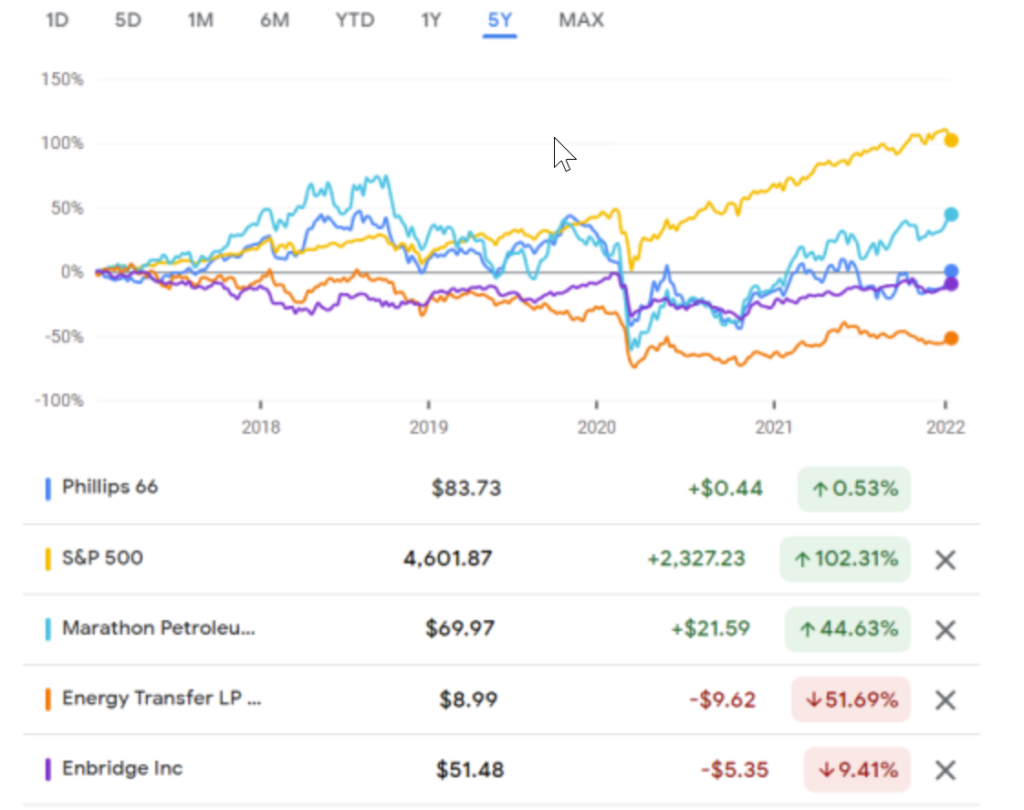

California’s two biggest pension funds have invested a staggering $43 billion in fossil fuel companies, and their opposition to divesting from the industry — including fighting legislation that would have stopped them investing in firms involved with the controversial Dakota Access Pipeline (DAPL) — has cost retirees and taxpayers billions, research shows.

The findings hammer home the fact that the divestment movement isn’t just about protecting the planet from the worst effects of climate change. With the oil, gas, and coal industries all on the decline, pension funds’ refusal to divest from fossil fuels is also endangering the retirement savings of teachers, government employees, and other rank-and-file public workers who have paid into these funds.

….

While it is common knowledge that fossil fuel stocks have underperformed the broader stock market, large bank stocks have been lackluster as well — including the banks that helped finance DAPL.

If CalPERS and CalSTRS had not opposed the original DAPL divestment legislation, they could have instead put pressure on the companies involved not to move forward with the pipeline, and such efforts might have been enough to stop the project, given the pipeline project’s turbulent history.

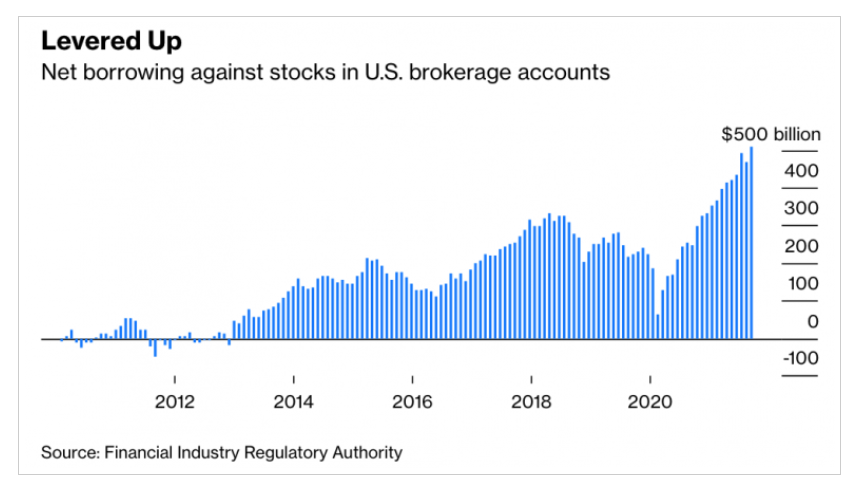

The financial press has gone into a round of hand-wringing over CalPERS’ efforts to chase higher returns in a systematically low-return market, now by planning to borrow at the CalPERS level on top of the leverage employed in many of its investment strategies, in particular private equity and real estate.

These normally deferential publications are correct to be worried. Not only is this sort of leverage on leverage dangerous because it can generate meltdowns and fire sales, amplifying damage and potentially creating systemic stresses, but the debt picture at CalPERS is even worse than these accounts they depicted. They failed to factor in yet another layer of borrowing at private equity funds and some real estate funds called subscription line financing, which we’ll describe shortly.

…..

CalPERS tells other less obvious fibs, such as trying to depict private equity as so critical to success that it need to put more money on that number on the roulette wheel. Remember, the name of the game in investment-land isn’t absolute performance but risk adjusted performance. Not only has private equity not generated the additional returns to compensate for its extra risk at least as long as we’ve been kicking those tires (since 2012), academic experts such as Ludovic Phalippou, Richard Ennis and Eileen Appelbaum have concluded private equity has not even beaten stocks since the financial crisis.

Let us stress that unlike German investors, who have a pretty good handle on all the leverage bets in their investment portfolios and thus can make a solid estimate of how much risk they are adding via borrowing across all their investments, CalPERS is flying blind with respect to private equity. It does not have access to the balance sheets of the portfolio companies in its various private equity funds.

And while having balance sheet would be a considerable improvement over what is has now, it doesn’t give the whole picture. CalPERS would also need to factor in operating leverage. When I was a kid at Goldman, whenever we analyzed leverage (as in all the time), we had to dig into the footnotes of financial statements, find out the amount of operating lease payments, and capitalize them, as in gross up the annual lease payments to an equivalent amount of borrowing so we could look at different companies on a more comparable basis.

Newport Beach City officials are advocating for policies aimed at increasing long-term sustainability in the state public employee pension fund, CalPERS, as Newport Beach continues to make significant progress in paying down its debt obligations to the system.

On November 16, the CalPERS Board of Administration decided to maintain the fund’s discount rate, or the expected rate of return of the pension fund investments, at the current 6.8 percent. The discount rate had been lowered from 7.0 percent to 6.8 percent in July through CalPERS’ Funding Risk Mitigation Policy, which automatically lowers the discount rate in years when investment returns are above the assumed rate of return. Prior to the recent discount rate change, Newport Beach had asked CalPERS to lower its discount rate to 6.5 percent or below, a more conservative number that could help further reduce future risk.

….

Newport Beach expects to eliminate its unfunded liability by 2030, thanks to an aggressive payment schedule. Beginning in 2018, the City Council decided to increase annual payments to $35 million a year, $9 million more than required. This fiscal year, for the second year in a row, the City will contribute $5 million more as an additional, discretionary payment, bringing the total contribution to $40 million.

The CalPERS board voted Monday to select a portfolio with a return of 6.8% and an expected volatility rate of 12.1%. This expected rate of return is two-tenths of a percentage point lower than last year’s target of 7%. The vote concluded a review of the pension fund’s assets, which occurs once every four years.

This expected reduction in the rate of return means that some employees will have to contribute more to their pension funds because the fund expects to earn less from its investment portfolio.

For employees hired after the implementation of the Public Employees’ Pension Reform Act (PEPRA) in January 2013, CalPERS estimates they will contribute an average of 1.2% to 1.5% more toward their pensions. These changes will go into effect for school employees, excluding teachers, in July 2022 and will be enacted for most other local government employees in July 2023.

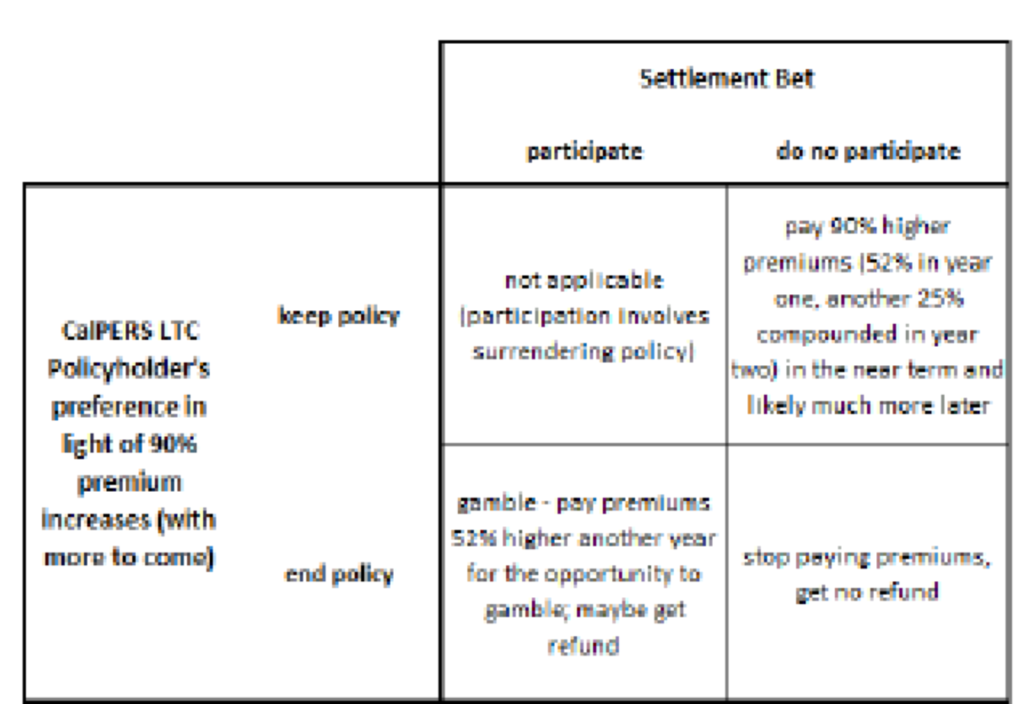

The graphic “Settlement Bet” shows options that policyholders have to choose from in the Settlement. The graphic “Settlement Happens??” shows the consequences of the “Settlement Bets” if the Settlement happens or not.

Policyholders not wanting to terminate their CalPERS policies will select not to participate (“opt out”) in the Settlement (as participation will end policyholders’ policies if the Settlement is approved).

Policyholders whose preference in light of announced rate increases would be to terminate because of the new CalPERS rate increases can be divided into two groups in light of the Settlement options: (1) those that wish simply to terminate and stop paying premiums; and (2) those who wish to terminate but are prepared to gamble with CalPERS to get a refund.

In making these choices, all policyholders are being forced to gamble a lot of money. Why the Settlement is structured as a gamble is unclear, but it is. That seems incredibly unfair to policyholders who can ill afford more financial losses after their losses already caused by CalPERS LTC.

The ongoing CalPERS long-term care insurance program crisis continues to unravel. It is also revealing overarching behavior which is both unethical and contrary to law.

CalPERS announced insurance premium increases of 52%-90% that become effective very shortly, at the same time that CalPERS has agreed to a class action lawsuit settlement over its last 85% rate increase. (In my next article I will discuss why I suspect the settlement is another con job by CalPERS.) But here I first must address a shocking revelation previously unreported about CalPERS long-term care insurance program (LTC) which needs to be recognized before moving on to the issues of the proposed settlement.

There is new and truly disturbing information about the CalPERS long-term care insurance program from a recent review of the enabling legislation prepared by a former California Deputy Attorney General and Court of Appeal Attorney, Linda J. Vogel.

According to Vogel’s analysis, the CalPERS long-term care insurance program since inception in 1991 has operated contrary to law.

But we also have Meng’s unreported stock trades. And Meng’s arrival happened to coincide with a big spike in personal trading violations, which CalPERS attempted to minimize by saying they came mainly from one person.

What if it turns out that the Olson report showed that Meng was a very active trader the entire time he was there? There is no way CalPERS could suppress this information, since it was required to have been reported on the Forms 700.

This would be hugely embarrassing to CalPERS, in that it would show it had hired a CIO who didn’t have his full attention on his very big ticket say job. And it would be vastly worse if Meng as head of the investment operation had been routinely violating SEC requirements for trade pre-approvals to prevent insider trading.

This possibility seems even more likely when you look at the board transcript below. Marlene Timberlake D’Adamo droned on and on and on trying to justify CalPERS not having reviewed Meng’s Form 700 to see if it looked internally consistent and/or matched up with his trading records. At first I thought this was to exhaust the board and dissipate their energy so they’d not be as persistent about their issues when they finally got the mike. But it may also be that the compliance department was clearly remiss in not reviewing Meng’s Form 700 by virtue of him being an active trader. And if he indeed was the person who’d made the big personal trading violations, that would almost mandate reviewing his Form 700.

In fact, all of the damaging information that got Meng so upset that he quit was public, and it all came directly from or was generated by Meng.

Yet the CalPERS board acts as if it’s the victim of internal saboteurs. As the transcript shows, CEO Marcie Frost and her key allies on the board, Board President Henry Jones and board member Rob Feckner repeatedly and falsely present Meng as a victim of secrets having been tossed over the transom to the press. Not only was everything that embarrassed Meng out in the open for competent reporters to write up, but in at least one and arguably two cases, Meng’s defensiveness made his situation much worse.

As we’ll show, Frost used the bogus idea that CalPERS is full of traitors as an excuse for continuing to keep the board in the dark about crucial matters like Meng being investigated for his financial conflict of interest. Frost and Feckner also claim that Meng believed that his bad press was due to saboteurs. That suggests that Frost and other senior staffers stoked Meng’s paranoia and helped precipitate his departure.

Despite having the most heavily staffed and luxuriously paid investment office of any public pension fund, CalPERS scored the worst investment returns of any of 34 funds tracked by Pensions & Investments.

As you can see at the Pensions & Investments site, CalPERS return for fiscal year 2020-2021 was 21.3%. The next lowest was tiny Kern County, more than two and a half points higher, at 23.9%. CalPERS’ Sacramento sister CalSTRS delivered 27.8%. The stars were Texas County, at 33.7&. New York Common, at 33.6%. San Bernardino County, at 33.3%, Oklahoma Teachers, at 33%, and Oklahoma Firefighters at 31.8%. Mississippi PERS came it at 32.7%, but that was gross of fees. Nevertheless, five funds earned a full 10% in investment returns more than CalPERS, and the pension fund arguably the most similar to CalPERS in terms of scale did more that 6% better.

That extreme laggard result also fell short of CalPERS benchmark of 21.7%. Recall that investment expert Richard Ennis explained at length that public pension funds and their consultants devise their own benchmarks, and they not surprisingly wind up being unduly forgiving

An earlier paper by Ennis found that even though nearly all public pension funds generated negative alpha, as in they actively destroyed value, CalPERS was one of the worst, coming in at number 43 out of 46, with a stunning negative alpha of 2.4%.

A plan by the California Public Employees’ Retirement System (CalPERS) to run its own multibillion dollar private debt investment program is dead for now after the state’s Senate Judiciary Committee rejected a bill that would have allowed the pension system to keep borrowers’ closely guarded financial information confidential.

The rejection by the committee last week is a major setback for the $469 billion pension system. CalPERS officials had planned to give out as much as $23 billion to companies seeking loans in the private debt market in an effort to boost financial returns for the system.

A day after the legislative committee’s vote, CalPERS Board Vice President Theresa Taylor asked at a board meeting whether the pension system could create an asset allocation that would allow it to earn its assumed rate of return without the in-house private lending program. Its current rate of return is 6.8%.

CalPERS does not need legislative permission for its investment program, but it needed state lawmakers to carve out an exemption to the state’s public disclosure laws to create the private debt program.

Jelincic is challenging CalPERS’ dubious denials of two different Public Records Act requests he made. One focuses on impermissible secret board discussions shortly after Chief Investment Officer Ben Meng’s sudden resignation last August. The filing not only calls for these records to be made public but also demands that board members be released to discuss all the matters that CalPERS impermissibly covered in the August “closed session”. The second involves CalPERS’ continuing efforts to hide records showing how it overvalued real estate investments by $583 million. Yet CalPERS not only has said nary a peep about bogus valuations are larger than the total amount it was slotted to invest in a mothballed solo development project, 301 Capitol Mall, but it continues to publish balance sheets that include the inflated results.

We predicted that CalPERS would be be even more inclined than usual to fight these Public Records Act requests because the filing seeks remedies beyond release of the records. First, it requests that CalPERS be found to have violated the Bagley-Keene Open Meeting Act. Second, to the extent that the judge rules that the board discussed items in closed session that should have been agendized for and deliberated in open session, the suit asks that board members be permitted to disclose the contents of those particular discussions in public. Third, the filing calls on the court to require that CalPERS make video and audio recordings of all closed sessions and keep them for five years (this is something that CalPERS currently does but this obligation is meant to shut the door to “the dog ate my disk” pretenses down the road.)

{kind=link}