The Senate parliamentarian approved provisions in Joe Biden’s $1.9 trillion pandemic-relief bill aiding multi-employer pensions and providing laid-off workers with health-care premium subsidies.

….

Senate parliamentarian Elizabeth MacDonough has found that provisions bailing out multi-employer pensions and providing laid-off workers with health-care premium subsidies are eligible for the simple-majority process Democrats are using to pass the pandemic-relief bill.

“This economic crisis has hit already struggling pension plans like a wrecking ball, and the retirement security of millions of American workers depends on getting this package across the finish line,” Senate Finance Chair Ron Wyden said in a statement after his office said the parliamentarian made the two approvals.

Ontario Municipal Employees Retirement System, one of Canada’s largest pension funds, posted its worst result since the global financial crisis after suffering big losses in its private equity and real estate holdings.

The pension fund, known as Omers, lost 2.7% on its investments last year, pushing assets to C$105 billion ($84 billion). It’s the worst result since 2008, when it lost 15.3%.

….

The pension fund fell far short of its 6.9% return benchmark, and also trailed the average 10% increase of Canadian pension plans, as estimated by Bank of New York Mellon Corp.

The New York State Common Retirement Fund, the third-largest U.S. public plan, said it’s pressing companies to boost their ethnic and gender diversity, and will vote against directors who fail to act.

“Companies must root out racial inequality, just as they would root any other systemic problem that puts their long-term success at risk,” New York State Comptroller Thomas P. DiNapoli said in a statement Thursday. “Corporate America must join in the national reckoning over racial injustice and confront institutionalized racism.”

The New York pension, which has $248 billion of assets, plans to file shareholder proposals supporting increased diversity on corporate boards. It also will seek better disclosures about the gender and ethnic breakdown of companies’ employees. The fund said it will vote against board members who ignore these requests.

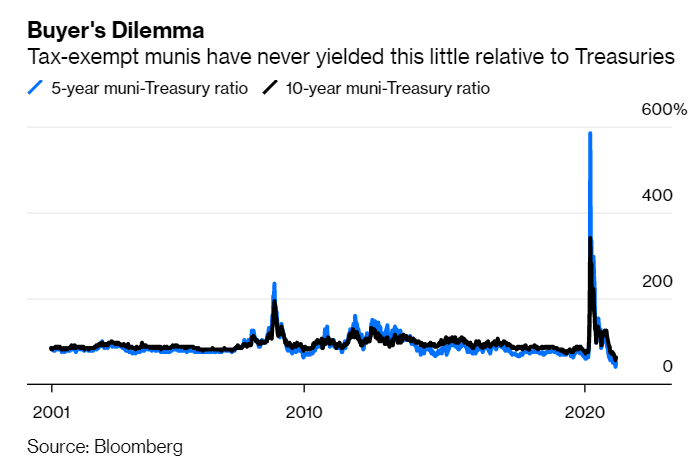

A flood of money pouring in? Check: Muni bond funds added about $2 billion in the week ended Feb. 17, according to Refinitiv Lipper US Fund Flows data, building upon a $2.6 billion inflow in the prior period that was the fourth-largest on record. Scarce supply? You bet: Some analysts estimate that states and cities in 2021 will bring to market the smallest amount of tax-exempt bonds in 21 years. Fiscal stimulus supporting its case? Indeed: The prospect of $350 billion in aid to state and local governments should help stave off any widespread credit stress.

Perhaps most remarkably, though, muni investors appear to have fully embraced the “HODL” mentality of the crypto crowd. In typical times, February’s sharp selloff in U.S. Treasuries, which has sent the benchmark 10-year yield up almost 30 basis points to 1.35% (for a monthly loss of almost 2%), would have reverberated by now across the market for state and local bonds. Instead, tax-exempt yields have been borderline immovable; they only finally started to budge toward the end of last week.

By that time, municipal bonds became arguably the most expensive asset class anywhere. As Bloomberg News’s Danielle Moran noted, yields had fallen so low on top-rated tax-free debt that even after accounting for the exemption from federal taxes, it still made more sense for investors to purchase Treasuries instead. It’s certainly fair to argue that Bitcoin isn’t worth more than $50,000, or that shares of Tesla Inc. shouldn’t be trading at more than 1,000 times earnings. But it’s at least possible to make the case that they should. It’s not every day that a corner of the bond market rallies to such an extent that it’s objectively a bad deal.

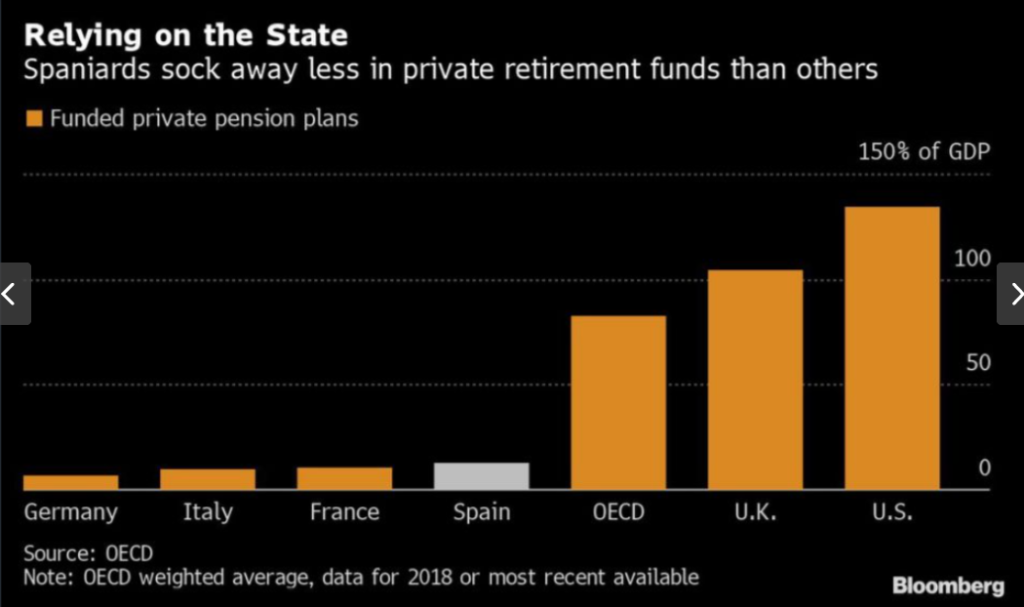

Spain is hoping to entice people to prepare for retirement with a voluntary saving plan as it tries to wean them off relying solely on state pensions.

The aim is to set up a fund run by private investment companies by the end of the year, offering Spaniards an affordable alternative to supplement their public pension. But unlike some other countries, the system will require workers to opt in rather than being automatically enrolled.

“We think there’s a group of middle- and low-income Spaniards who will be interested in a boost to their lifetime savings, which can complement their public pension,” Jose Luis Escriva, the social security minister for Spain’s Socialist-led government, said in an interview.

It was hardly the role Citigroup Inc.’s bankers signed up for when they helped Ron Perelman’s Revlon Inc. borrow US$1.8 billion in 2016. But, now a back-office blunder is leaving the financial behemoth faced with the prospect of becoming one of the biggest creditors to the troubled cosmetics empire.

A surprise ruling by a New York judge on Tuesday blocked Citigroup’s efforts to recover US$500 million it had mistakenly sent Revlon’s lenders last year as the so-called administrative agent on the company’s loan. While the bank says it will appeal the decision, a failure to overturn it will leave Citigroup holding the bag on the bulk of the US$900 million remaining on the loan that Revlon hasn’t itself paid.

“Revlon’s loan was never paid off. So if appeals fail, Citi will ultimately step into the shoes of the lenders and own US$500 million of that nearly US$900 million term loan.” said Philip Brendel, a senior distressed debt analyst at Bloomberg Intelligence.

The Federal Reserve Bank of New York on Wednesday released its quarterly report on household debt and credit for the final three months of 2020, with its strategists and statisticians deciding to dig deeper into mortgage originations, the types of homebuyers during the Covid-19 pandemic and to what extent Americans are taking out cash against their home equity. While much of what they found confirms many of the narratives about the housing market, it’s the sheer magnitude of the move that’s breathtaking and puts into context where the economy stands almost one year after the coronavirus crisis began in the U.S.

At the highest level, mortgage originations reached almost $1.2 trillion in the final three months of 2020, the highest quarterly volume in the history of the New York Fed’s data, which begins in 2000. Americans refinanced more mortgage debt last year than any time since 2003, while mortgages taken out to purchase a home surged to the highest since 2006. First-time buyers took on more debt than at any time in history, while mortgages for repeat buyers and those looking for a second home or an investment property reached the highest in more than a decade.

Meanwhile, home prices soared across the U.S., with the S&P CoreLogic Case-Shiller index jumping 9.5% in November, the most since 2014 (December’s figures will be released next week). This surge led to “a notable increase in cashout refinance volumes, which spiked in the fourth quarter of 2020 and show no sign of abating,” the New York Fed researchers said in a blog post. Collectively, homeowners withdrew $182 billion in home equity in 2020, or an average of about $27,000 for each household. Even those who chose not to take out extra cash saved an average of $200 a month on their mortgage payments.

First, wise public sector investments are better for the poor than one-time wealth transfers. The U.S. is still reaping the benefits of the great public health and public works achievements of the 20th century. Second, the most enduring and beneficial government-transfer programs, such as Social Security, have been built on sustainable majorities.

…..

It’s not as if there aren’t obvious candidates for alternative investment: green energy, broadband and public health infrastructure for the next pandemic, to name a few. Yes, I am familiar with the argument that spending the extra trillion or so now will make it possible to spend more trillions later, including on such policies. But whatever kind of complicated political story you might tell, the basic laws of economics have not been repealed. Increasing current expenditures does, in fact, involve foregone future opportunities.

Shuttering failing Australian pension funds and stopping new accounts being opened when changing jobs will add almost A$100,000 ($77,160) to the retirement savings of young workers.

Minister for Superannuation Jane Hume is shepherding new laws through Australia’s parliament to revamp the industry to weed out under-performing funds and make pension accounts automatically follow workers when they change employers.

It’s designed to protect the retirement savings of the most disengaged Australians — one-in-five of whom have never contacted their fund. Hume estimates that a young person going into a super fund for the first time will be around A$98,000 better off at retirement after the reforms.

Author(s): Matthew Burgess, Shery Ahn, and Paul Allen