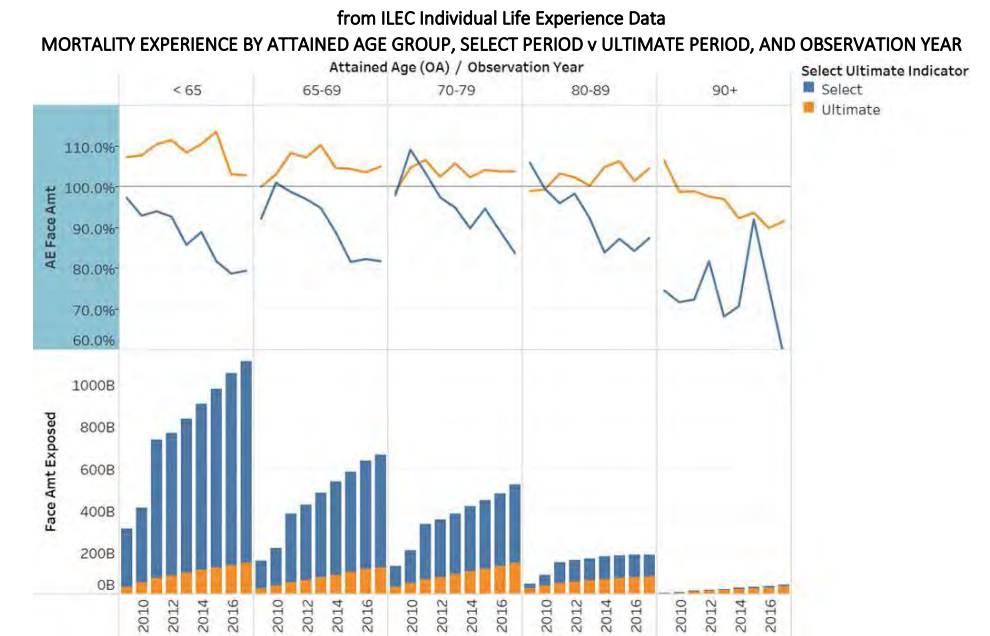

The Society of Actuaries (SOA) Research Institute released a report that examines older age mortality (OAM) with a focus on attained ages 70 and above. The report helps determine whether refinements were needed in the 2015 Valuation Basic Tables. Analysis was performed by sex, issue age and attained age, issue year cohorts, smoking risk classification, benefit band, select vs ultimate period, and interactions.

Author(s):

Old Age Mortality Subgroup of the Individual Life Experience Committee

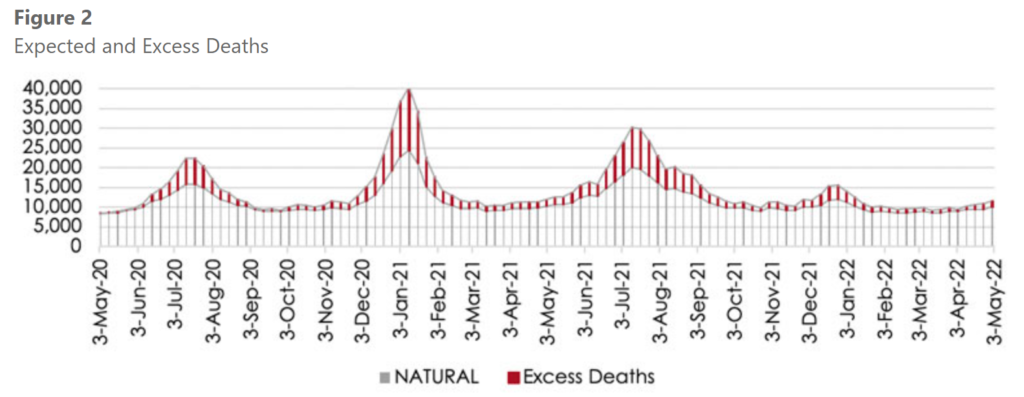

The impact of Covid-19 in South Africa in terms of excess deaths was substantial, when considering the reported excess deaths as published by the South African Medical Research Council (SAMRC).[4] Please note that in this article we will not further consider whether all excess deaths can be directly attributed to Covid-19, however, as per the article “Correlation of Excess Natural Deaths with Other Measures of the Covid-19 Pandemic in South Africa,”[5] it is estimated that 85 percent to 95 percent of excess natural deaths are attributable to Covid-19.

Based on the SAMRC excess deaths, taking the expected plus excess deaths as Actual and expected natural deaths as per their methodology as Expected, we observe an Actual versus Expected (AvE) ratio of 116 percent in 2020, a ratio of 131 percent in 2021, and a ratio of 113 percent in 2022 up to May 1. When we look at the AvE for each wave, we can see that the 2nd wave (predominantly Beta variant) and the 3rd wave (predominantly Delta variant), had the most severe impact on the general population (see figure 2 and figure 3)

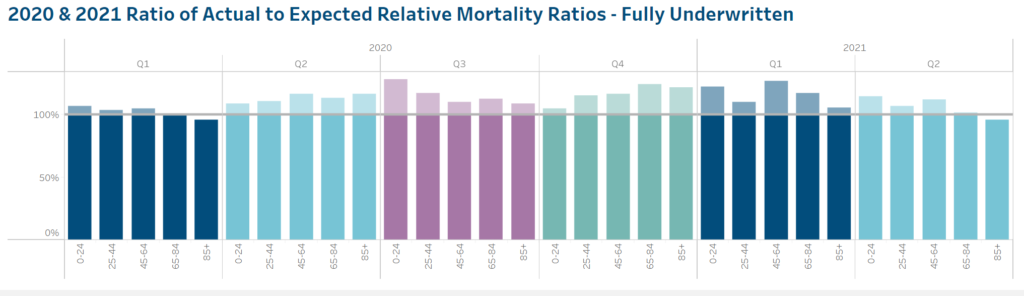

LIMRA, Reinsurance Group of America (RGA), the Society of Actuaries (SOA) Research Institute, and TAI have collaborated on an ongoing effort to analyze the impact of COVID-19 on the individual life insurance industry’s mortality experience and share the emerging results with the insurance industry and the public. The Individual Life COVID-19 Project Work Group (Work Group) was formed as a collaboration of LIMRA, RGA, the SOA Research Institute, and TAI to design, implement, and create the study and to produce and distribute a variety of analyses. This report is the fifth public release from this collaboration and contains the results of the study of excess mortality for individual life insurance to include the second quarter of 2021. Data from 31 companies representing approximately 72% of the industry face amount in force have been included in the analysis in this report. A total of 3.0 million death claims from individual life policies from 2015 through June 30, 2021 make up the basis of the analysis.

Highlights for the 2nd Quarter

The second quarter of 2021 showed a significant realignment of the actual to expected relative mortality ratios, across many different cuts of the data.

It is worth noting that the third quarter 2021 results will likely not be as favorable due to the impact of the COVID-19 Delta variant whose impact first started in July 2021 and peaked around mid- September

All age groups improved in the second quarter compared to the first quarter of 2021, but the improvement was more dramatic in the older ages. While the three age groups shown under age 65 were still significantly over the trend established by 2015-2019, the age 65-84 group was within the 95% confidence bands and the age 85+ group was significantly better than the 2015-2019 trend (p < 0.05).

Whereas the pandemic experience so far had showed substantial variations across different regions, this appears to have moderated during the 2nd quarter of 2022.

Author(s): Individual Life COVID-19 Project Work Group, SOA

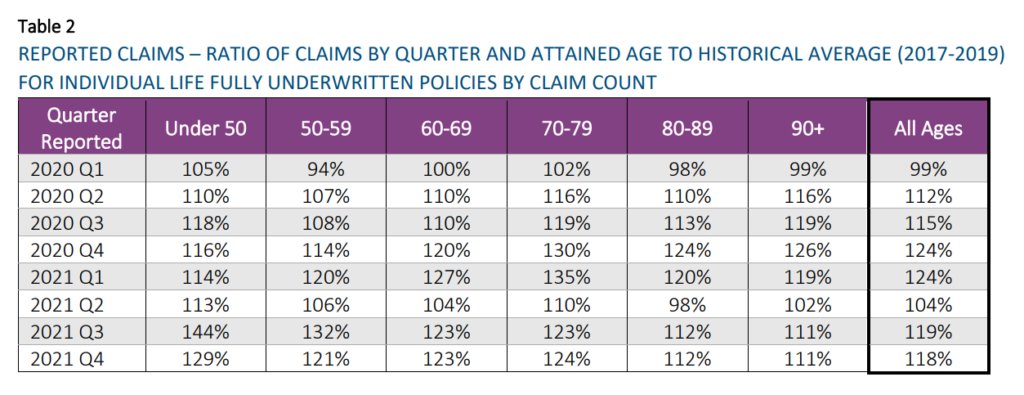

LIMRA, Reinsurance Group of America (RGA), the Society of Actuaries Research Institute (SOA), and TAI have collaborated on an ongoing effort to analyze the impact of COVID-19 on the individual life insurance industry’s mortality experience and share the emerging results with the insurance industry and the public. This report documents a high-level analysis of the claims that have been reported through December 31, 2021. The results presented here are based on data from 32 companies representing approximately 72% of the individual life insurance in force for the experience period of the study.

Author(s): Individual Life COVID-19 Project Work Group

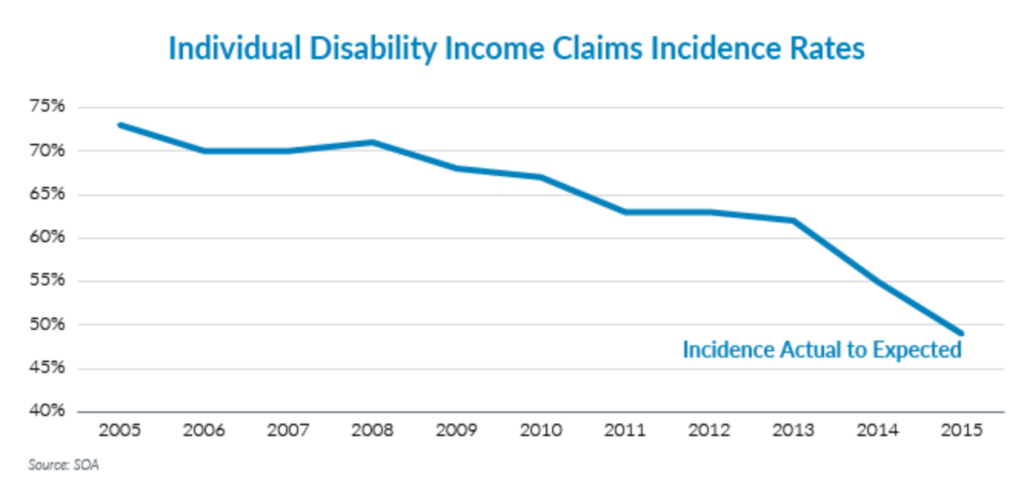

Second, one of the key drivers of these stable and low benefit ratios has been steady-to-declining rates of claims incidence. In a recent paper published by the SOA and co‑authored by Gen Re’s Jay Barriss, Individual Disability incidence rates were shown to have steadily improved over the 2005 to 2015 period, relative to the latest Individual Disability Valuation Table (IDIVT) incidence rate expectations.10 The favorable incidence rate trends have likely continued into at least into 2020 as Gen Re analysis on our reinsured blocks of disability business show continuing-to-stable incidence trends since 2015.