Insurance companies that have long said they’ll cover anything, at the right price, are increasingly ruling out fossil fuel projects because of climate change – to cheers from environmental campaigners.

More than a dozen groups that track what policies insurers have on high-emissions activities say the industry is turning its back on oil, gas and coal.

The alliance, Insure Our Future, said Wednesday that 62% of reinsurance companies – which help other insurers spread their risks – have plans to stop covering coal projects, while 38% are now excluding some oil and natural gas projects. (The Insure Our Future report on re/insurers’ fossil fuel activities can be viewed here).

In part, investors are demanding it. But insurers have also begun to make the link between fossil fuel infrastructure, such as mines and pipelines, and the impact that greenhouse gas emissions are having on other parts of their business.

Liability-driven investment allows schemes to invest in the growth assets they need to close the funding gap while reducing the impact of interest rates on the liabilities. This is achieved by assigning a portion of a portfolio to an LDI fund. Rather than this fund just holding gilts, it holds a mixture of gilts and gilt repos.

A gilt repo is re-purchase agreement. The LDI manager sells a gilt to a counterparty bank while arranging to buy back that gilt at a later date for an agreed price. This gilt repurchase agreement provides cash to the pension scheme which it can then use to invest in other assets.

This mixture of gilts and gilt repos in an LDI fund uses leverage to provide capital to the pension fund. It is akin to using a mortgage to buy a house. Different levels of leverage were available in the funds – the more leverage, the greater the ratio of gilt repos to gilts in a fund.

The more leverage in a fund, the less capital a pension scheme had to lock up in government debt and the more it could use to invest in assets which could help to close its funding gap. This was helpful when interest rates were low but became problematic when gilt yields rose.

The relatively puny amounts of actual purchases show that the BOE is trying to calm the waters around the gilts market enough to give the pension funds some time to unwind in a more or less orderly manner whatever portion of the £1 trillion in “liability driven investment” (LDI) funds they cannot maintain.

The small scale of the intervention also shows that the BOE is not too upset with the gilts yields that rose sharply in the run-up to the crisis, triggering the pension crisis, and have roughly remained at those levels. The 10-year gilt yield today at 4.44% was roughly unchanged from yesterday and just below the September 27 spike peak.

And it makes sense to have these kinds of yields in the UK, and it would make sense for these yields to be much higher, given that inflation has spiked to 10%, and yields have not kept up with it, nor have they caught up with it. And to fight this raging inflation, the BOE will need to maneuver those yields far higher still:

So today, BOE Governor Andrew Bailey, speaking at the Institute of International Finance annual meeting in Washington D.C., warned these pension fund managers that the BOE will only provide this level of support, however little it may be, through the end of the week, to smoothen the gilt market and give the pension funds a chance to unwind in a more or less orderly manner the portions of their LDI funds that they cannot maintain.

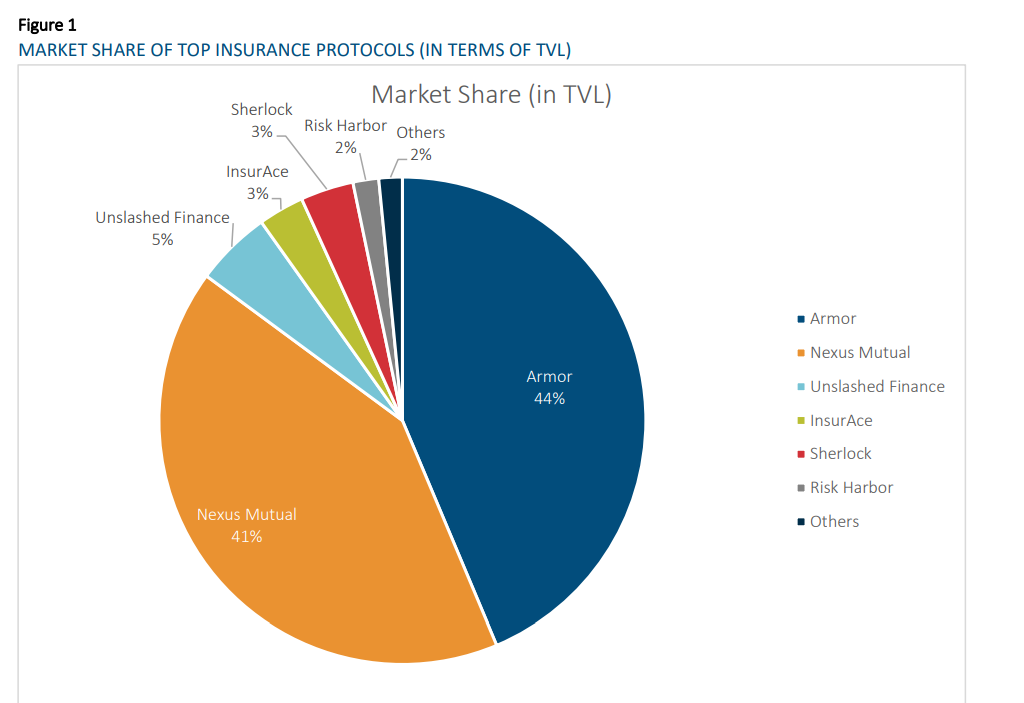

The DeFi ecosystem has been expanding rapidly in the past few years, growing from less than USD $1 billion in 2020 to USD $61.6 billion as of June 2022 as measured by Total Value Locked (TVL), the amount of crypto asset deposited in the DeFi protocols.

With continuous innovation in product design and delivery, the potential of DeFi adoption is massive. However, the rise of DeFi is marred by security issues. Nearly 200 blockchain hacking incidents have taken place in 2021 with approximately USD $7 billion in stolen funds (Cointelegraph, 2021). These hacking events have a wide range of causes including, but not limited to, the following:

Smart contract vulnerabilities exploited by hackers to steal funds

Manipulation of oracles to cause price feed deviation

Attack on governance where a small group of individuals took over the protocol’s governance decisionmaking mechanism

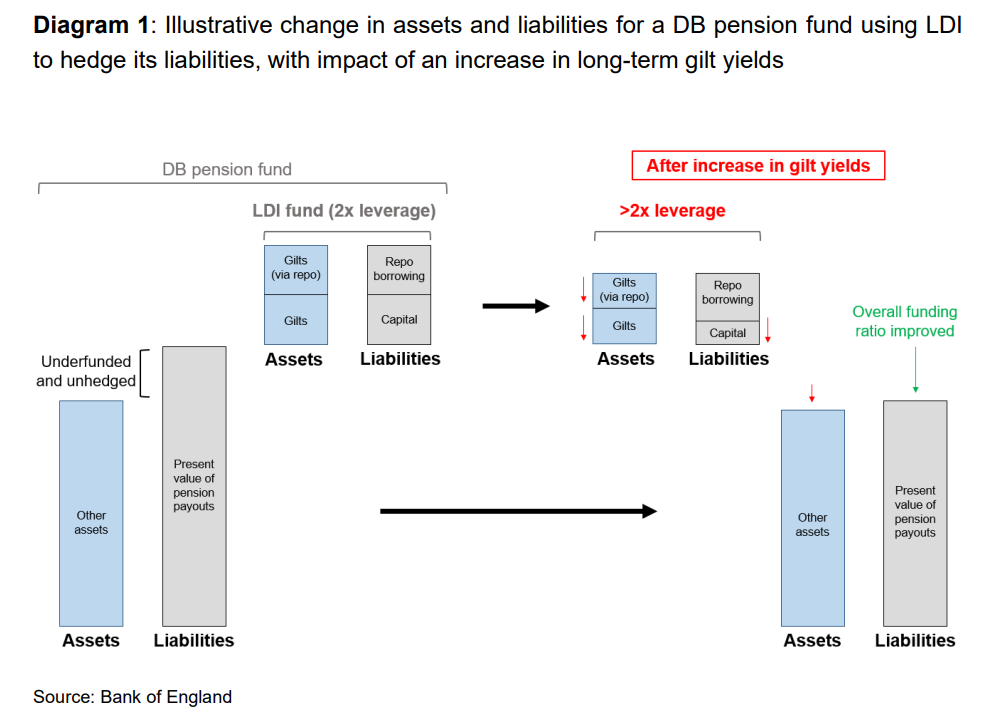

LDI strategies enable DB pension funds to use leverage (i.e. to borrow) to increase their exposure to long-term gilts, while also holding riskier and higher-yielding assets such as equities in order to boost their returns. The LDI funds maintain a cushion between the value of their assets and liabilities, intended to absorb any losses on the gilts. If losses exceed this cushion, the DB pension fund investor is asked to provide additional funds to increase it, a process known as rebalancing. This can be a more difficult process for pooled LDI funds, in part because they manage investment from a large number of small and medium sized DB pension funds.

Diagram 1 gives a stylised example of how the gilt market dynamics last week could have affected a DB pension fund that was investing in an LDI fund. In this illustrative and simplified example, the left hand side of the diagram shows that the scheme is underfunded (in deficit) before any change in gilt yields, with the value of its assets lower than the value of its liabilities. More than 20% of UK DB pension funds were in deficit in August 2022 and more than 40% were a year earlier. In this example, the fund is holding growth assets to boost returns and has also invested in an LDI fund to increase holdings of longterm gilts, funded by repo borrowing at 2 times leverage (i.e. half of the holding of gilts in the LDI fund is funded by borrowing). The cushion (labelled ‘capital’) is half the size of the gilt holdings.

The right hand side of the diagram shows what would happen should gilt yields rise (and gilt prices fall). The value of the gilts that are held in the LDI fund falls, in this example by around 30%. This severely erodes the cushion in the LDI fund. If gilt prices fell further, it would risk eroding the entire cushion, leaving the LDI fund with zero net asset value and leading to default on the repo borrowing. This would mean the bank counterparty would take ownership of the gilts. It should be noted that in this example, the DB pension fund might be better off overall as a result of the increase in gilt yields. This is because the market value of its equity and shorter-term bond holdings (‘other assets’) would not fall by as much as the present value of its pension liabilities, as the latter are more sensitive to long-term market interest rates. The erosion of the cushion of the LDI fund would lead the LDI fund either to sell gilts to reduce its leverage or to ask the DB pension fund investors to provide additional funds.

In practice, the move in gilt yields last week threatened to exceed the size of the cushion for many LDI funds, requiring them to either sell gilts into a falling market or to ask DB pension plan trustees to raise funds to provide more capital.

Author(s): Sir John Cunliffe, Deputy Governor, Financial Stability

The central bank’s Financial Policy Committee stepped in after a massive sell-off of U.K. government bonds — known as “gilts” — following the new government’s fiscal policy announcements on Sept. 23.

The emergency measures included a two-week purchase program for long-dated bonds and the delay of the bank’s planned gilt sales, part of its unwinding of Covid pandemic-era stimulus.

The 30-year gilt yield fell more than 100 basis points after the bank announced its emergency package on Wednesday Sept. 28, offering markets a much-needed reprieve.

Cunliffe noted that the scale of the moves in gilt yields during this period was “unprecedented,” with two daily increases of more than 35 basis points in 30-year yields.

“Measured over a four day period, the increase in 30 year gilt yields was more than twice as large as the largest move since 2000, which occurred during the ‘dash for cash’ in 2020,” he said.

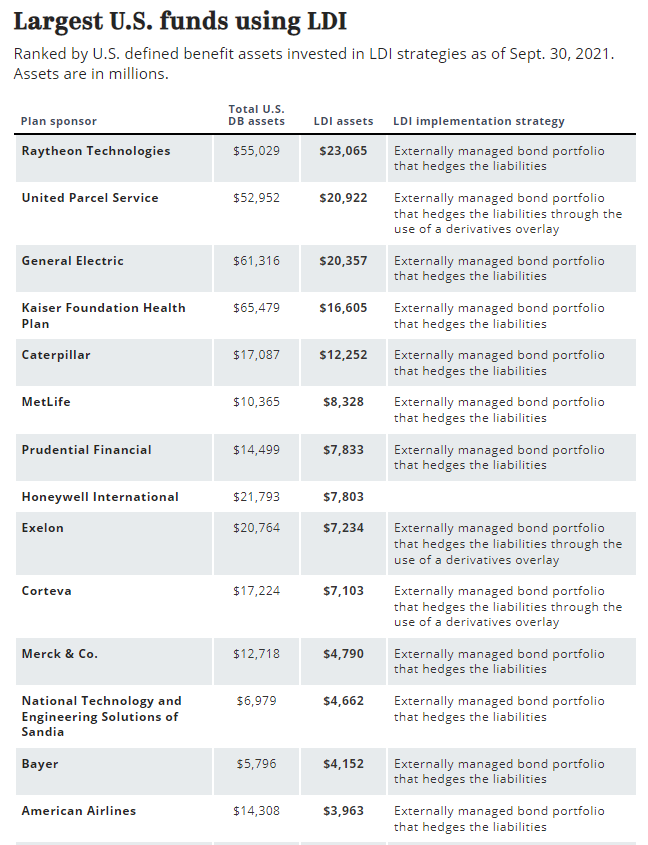

The Bank of England’s emergency bond-buying last week helped shore up U.K. pension funds and threw a spotlight on a popular strategy among corporate plans known as LDI – or liability-driven investing.

Total assets in LDI strategies in the U.K. rose to almost £1.6 trillion ($1.8 trillion) at the end of 2021, quadrupling from £400 billion in 2011, according to the Investment Association, a trade group that represents U.K. managers. Many LDI mandates allow for the use of derivatives to hedge inflation and interest rate risk.

….

Here’s how LDI works: Liability-driven investing is employed by many pension funds to mitigate the risk of unfunded liabilities by matching their asset allocation and investment policy with current and expected future liabilities. The LDI portion of a pension fund’s portfolio utilizes liability-hedging strategies to reduce interest-rate risk, which could include long government and credit bonds and derivatives exposure.

Jeff Passmore, LDI solutions strategist at MetLife Investment Management, said the situation with U.K. pension plans “has been challenging, and the heavy use of derivatives in the U.K. LDI model has made the current situation worse than it would otherwise be.”

While most U.S. LDI portfolios rely on bonds rather than derivatives, ‘”those U.S. plan sponsors who have leaned heavily on derivatives and leverage should take a cautionary lesson from what we’re seeing currently across the Atlantic.”

….

The U.K. pension debacle “is a plain-and-simple problem of leverage,” Charles Van Vleet, assistant treasurer and chief investment officer at Textron, said in an email.

Many U.K. pension plans were interest rate-hedged at 70%, while also holding 60% in growth assets, suggesting 30% leverage, he said. The portfolio’s growth assets have lost around 20% of value if held in public equities and fixed income or about 5% down if held in private equity, he noted.

“Therefore, to make margin calls on their derivative rate exposure they had to sell growth assets – in some cases, selling physical-gilts to meet derivative-gilt margin calls,” Mr. Van Vleet said.

“The problem is worse for plans who gain rate exposure with leveraged ETFs. The leverage in those funds is commonly via cleared interest rate swaps. Margin calls for cleared swaps can only be met with cash – not posted collateral. Therefore, again selling physical-gilts to meet derivative-gilt margin calls.”

Author(s):

BRIAN CROCE COURTNEY DEGEN PALASH GHOSH ROB KOZLOWSKI

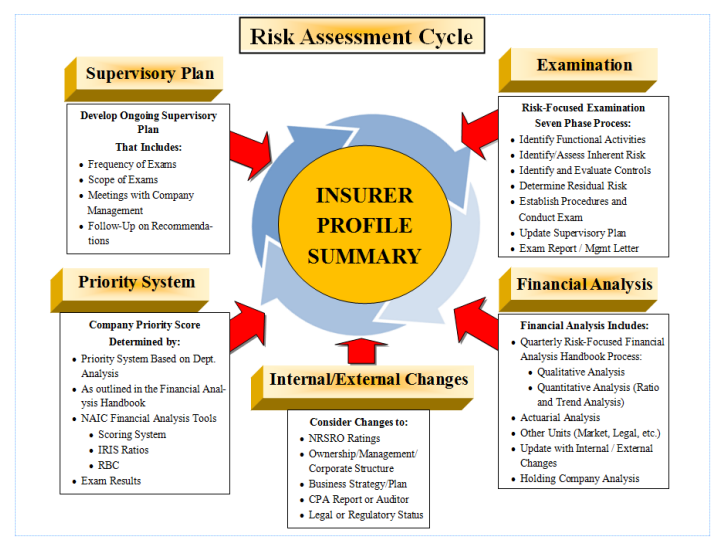

The risk-focused surveillance framework is designed to provide continuous regulatory oversight. The risk-focused approach requires fully coordinated efforts between the financial examination function and the financial analysis function. There should be a continuous exchange of information between the field examination function and the financial analysis function to ensure that all members of the state insurance department are properly informed of solvency issues related to the state’s domestic insurers.

The regulatory Risk-Focused Surveillance Cycle involves five functions, most of which are performed under the current financial solvency oversight role. The enhancements coordinate all of these functions in a more integrated manner that should be consistently applied by state insurance regulators. The five functions of the risk assessment process are illustrated within the Risk-Focused Surveillance Cycle.

As illustrated in the Risk-Focused Surveillance Cycle diagram, elements from the five identified functions contribute to the development of an IPS. Each state will maintain an IPS for its domestic companies. State insurance regulators that wish to review an IPS for a non-domestic company will be able to request the IPS from the domestic or lead state. The documentation contained in the IPS is considered proprietary, confidential information that is not intended to be distributed to individuals other than state insurance regulators.

Please note that once the Risk-Focused Surveillance Cycle has begun, any of the inputs to the IPS can be changed at any time to reflect the changing environment of an insurer’s operation and financial condition.

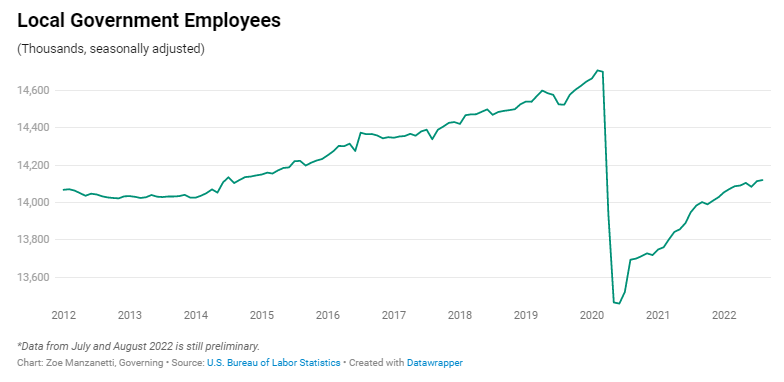

States and cities all over the country have seen a loss of workers over the past several years, and many are struggling to hire new ones. According to the Bureau of Labor Statistics, state and local governments lost more than 600,000 workers between the start of the pandemic and June of this year. Those shortages have begun to affect basic services, including many that are critical to safety and quality of life. According to a Center for American Progress report from March, there were 10,000 fewer water and wastewater treatment plant operators in 2021 than there were in 2019.

…..

The obvious reason why governments have struggled to hire and retain workers over the past few years, says Brad Hershbein, senior economist and deputy director of research at the W.E. Upjohn Institute for Employment Research, is that they can’t improve pay rates as quickly as the private sector can in response to worker demands for better wages. Another reason is that lots of government work has become newly politicized during the pandemic — public workers can be “heroes one day and villains the next,” he says. And a third factor is that staff shortages tend to make work that much more difficult for people who remain, contributing to unattractive working conditions.

“The burnout gets worse,” Hershbein says. “You get a spiral, where fewer people are stuck trying to handle the same amount of work and the whole thing collapses. That’s a real risk at a lot of agencies.”

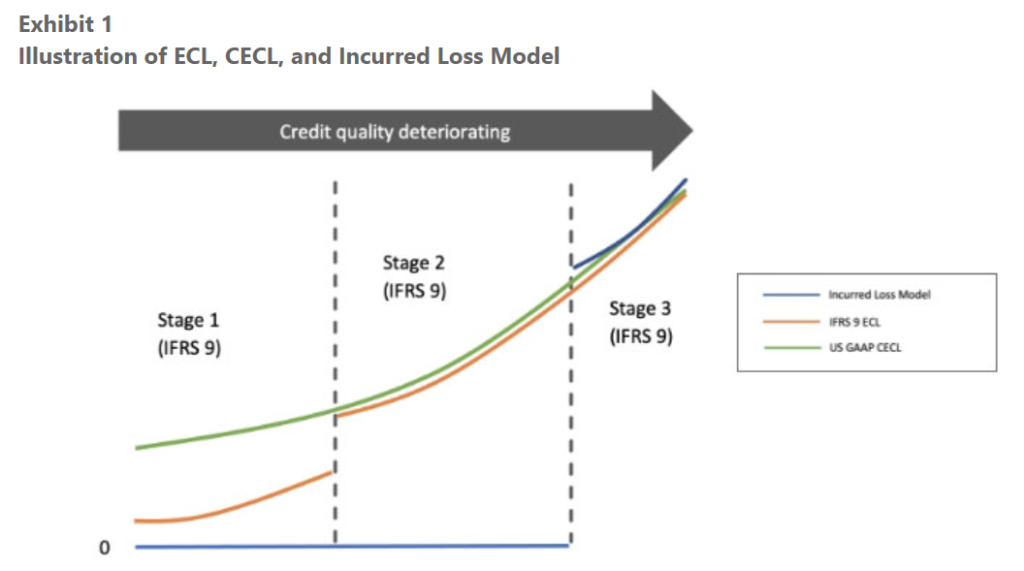

Under the old regime, the impairment was the incurred credit losses, in determining which only past events and current conditions are used. Credit losses were booked after a credit event had taken place, thus the name “incurred.” ECL and CECL require the incorporation of forward-looking information in addition to the past/current info in the calculation of impairment. There will be an allowance for credit losses since initial recognition regardless of the creditworthiness of the investment asset. The allowance can be perceived as the reserve or capital for credit risks. In practice, the allowance could be zero if there are no expected default losses for the instrument, US Treasury bonds, US Agency MBS, just to name a few.

ECL under IFRS 9 is typically calculated as a probability weighted estimate of the present value of cash shortfalls over the expected life of the financial instrument. It Is an unbiased best estimate with all cash shortfalls taking into consideration the collaterals or other credit enhancement. Four typical parameters underlying its calculation are: Probability of default (PD), loss given default (LGD, i.e., 1-Recovery Rate), exposure at default (EAD) and discounting factor (DF). Prepayments, usage given default (UGD) and other parameters can also play a role in the calculations. In the general approach the loss allowance for a financial instrument is 12-month ECL regardless of credit risk at the reporting date, unless there has been a significant increase in credit risk since initial recognition: The PD is only considered for the next 12 months while the cash shortfalls are predicted over the full lifetime; as the creditworthiness deteriorates significantly, the loss allowance is increased to full lifetime ECL in Stage 2, which should always precede stage 3 (credit impairment). Even without change of stages, any credit condition changes should be flowing into the credit loss allowance via updates in some of the underlying parameters. Exhibit 1 has an illustrative comparison between ECL, CECL, and incurred loss model.

CECL is similar to ECL except FASBs doesn’t have so-called staging as IFRS 9, which requires that only 12-month ECL is calculated in stage 1 (in the general model). In other words, CECL requires a full lifetime ECL from Day 1. There are also other differences: IFRS 9 requires certain consideration of time value of money, multiple scenarios, etc., in measurement of ECL while US GAAP CECL doesn’t.

Under US GAAP, different from CECL, currently the impairment for AFS assets, while also recorded as an allowance (with a couple exceptions), is only needed for those whose fair value is less than the amortized cost. Once it is triggered, the credit losses are then measured as the excess of the amortized cost basis over the probability weighted estimate of the present value of cash flows expected to be collected. Only the fair value change related to credit is considered in the calculation of AFS impairment. The quantitative calculation behind the probability weighted best estimate is like CECL/ECL. Both can use discounted cash flow methods with parameters such as PD although one is calculating expected cash shortfalls directly in CECL and the other is calculating the expected collectible cash payments and then is used to back out the impairment.

Interest rates cycle over long periods of time. The journey tends to be unpredictable, full of unexpected twists and turns. This project focuses on the impact of interest rate volatility on life insurance products. As usual, it brought up more questions than it answered. It points out the importance of stress testing for a specific block of business and the risk of relying on industry rules of thumb. Understanding the nuances of models could make the difference between safe navigation of a stressed environment and a default. Proactive and resilient practices should increase the odds of success.

Hyman Minsky had it right—stability leads to instability. We live in an era where monetary policies of central banks steer free markets in an effort to soften the business cycle. Rates have been low for over 20 years in Japan, reshaping the global economy.

The primary goal of this paper is to explore rising interest rates, but that is not possible without considering that some rates could stabilize at low levels or even decrease. Following this path, the paper will look at implications of interest rate changes for the life insurance industry, current stress testing practices, and how a risk manager can proactively prepare for an uncertain future. A paper published in 2014 focused on why rates could stay low, and some aspects of this paper are similar (e.g., description of insurance products). This paper also uses a sample model office to help practitioners look at their own exposures. It includes typical interest-sensitive insurance products and how they might perform across various scenarios, as well as a survey to establish current practices for how insurers are testing interest rate risk currently.

Author(s): Max Rudolph, Randy Jorgensen, Karen Rudolph