Link: https://www.swissinfo.ch/eng/unions-contest-pension-reform-plans-with-bern-demonstration/46959184

Excerpt:

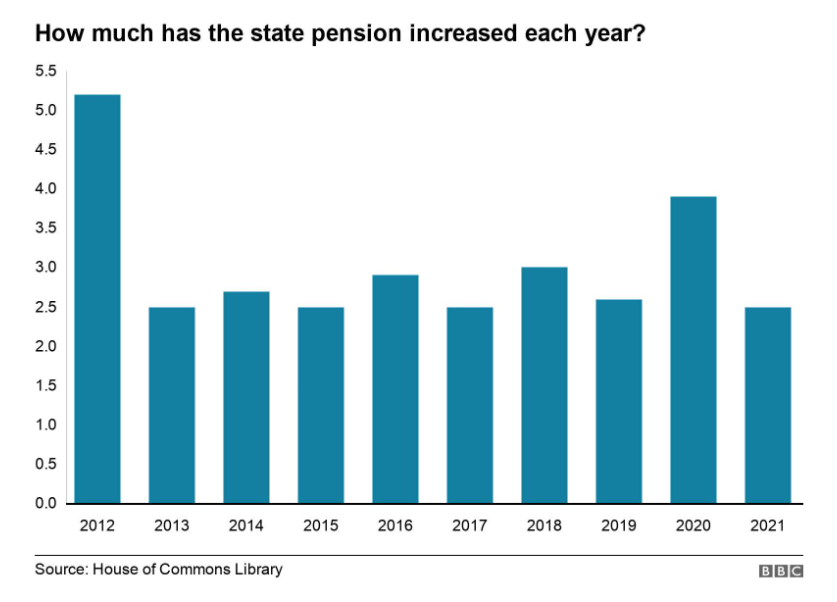

Thousands marched in Bern on Saturday against a proposed reforms of the Swiss old-age pension scheme, notably the plan to raise the retirement age for women from 64 to 65.

The demonstration, which was authorised by Bern authorities, was attended by some 15,000 people, according to the trade unions who organised it; the police have not (yet) released estimates.

The protest took place under the slogan “hands off our pensions”, and was clearly aimed at parliamentarians currently discussing an overhaul of the country’s three-pillar system.

A press release by the Trade Union Federation said that the current pension system is “no longer enough to live on” and that politicians should be raising payments rather than trying to cut them; as for making women work a year longer, this is a non-runner, it says, given the years of part-time and unpaid work they do during their active lives.

Publication Date: 18 Sept 2021

Publication Site: Swiss Info