Graphic:

Excerpt:

Many U.S. towns and cities are years behind on their pension obligations. Now some are effectively planning to borrow money and put it into stocks and other investments in a bid to catch up.

State and local governments have borrowed about $10 billion for pension funding this year through the end of August, more than in any of the previous 15 full calendar years, according to an analysis of Bloomberg data by Municipal Market Analytics. The number of individual municipalities borrowing for pensions soared to 72 from a 15-year average of 25.

Among those considering what is known as pension obligation borrowing is Norwich, a city in southeastern Connecticut with a population of 40,000. Its yearly payment toward its old pension debts has climbed to $11 million in 2022—four times the annual retirement contribution for current workers and 8% of the city’s budget. The city will vote in November on whether to sell $145 million in 25-year bonds to cover the pensions of retired police officers, firefighters, city workers and school employees.

….

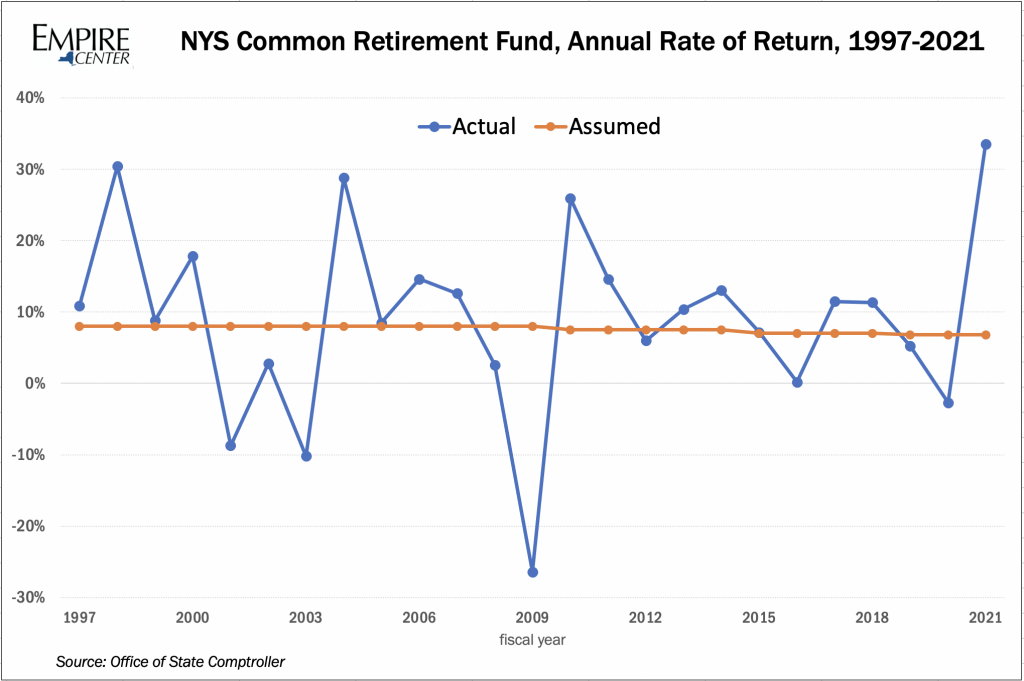

In 2009, Boston College’s Center for Retirement Research examined pension obligation bonds issued since 1986 and found that most of the borrowers had lost money because their pension-fund investments returned less than the amount of interest they were paying. A 2014 update found those losses had reversed and returns were exceeding borrowing costs by 1.5 percentage points.

Author(s): Heather Gillers

Publication Date: 4 September 2021

Publication Site: Wall Street Journal

{kind=link}