Link: https://www.illinoispolicy.org/over-100-of-danville-municipal-property-taxes-consumed-by-pensions/

Graphic:

Excerpt:

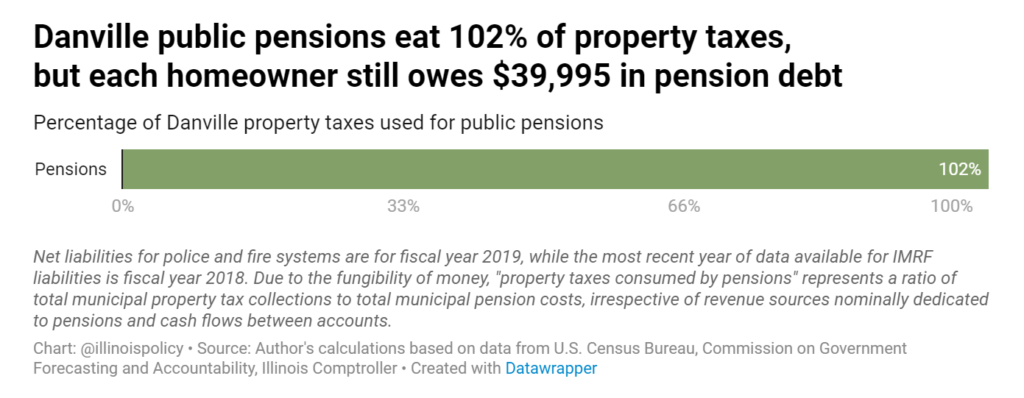

The average Danville household owns nearly $40,000 in state and local pension debt.

Illinois’ worst-in-the-nation pension debt has become a well-known problem. Over $144 billion in pension debt for the five statewide retirement systems breaks down to nearly $30,000 in debt for each household, which must be paid with further tax hikes or further cuts to core government services.

Less well known is the nearly $75 billion of pension debt held by local governments in Illinois, which is the primary reason for Illinois’ second-highest in the nation property taxes. Combined with the state’s pension debt, politicians who mismanaged the pension system dug a $219 billion hole.

In Danville, the average household owns nearly $40,000 in state and local pension debt, with over $10,000 of that debt stemming from local systems for police, firefighters and municipal workers. To pay off that pension debt, a Danville household would have to give up 110% of an entire year’s $36,172 median annual income.

Author(s): Adam Schuster, Perry Zhao

Publication Date: 20 Sept 2021

Publication Site: Illinois Policy Institute