Link:https://marypatcampbell.substack.com/p/revisualizing-the-financial-state

Graphic:

Excerpt:

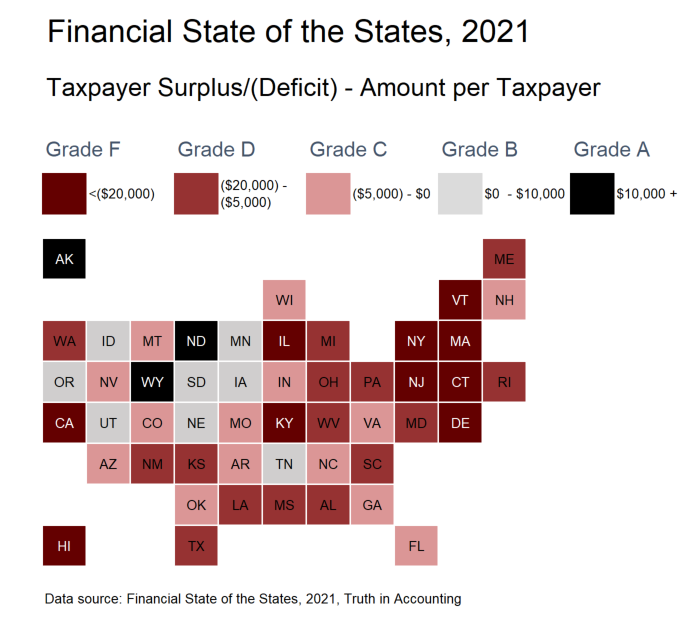

One large benefit of a tile grid map is you can see the geographically small states, which are often more obscured when you a geographically accurate map.

When viewed in this way, with the states colored by their grades, you can see that there’s a Northeastern Rogue’s Gallery, in addition to the expected stinkers of Illinois, Kentucky, and California (also, Hawaii, but many people don’t expect that one.)

But I want to point out that a lot of “red” states, in the political sense, also have crappy finances.

Texas is a particularly bad offender here, with a taxpayer deficit of -$13,100 per taxpayer. It’s not just the “expected” states where pensions are grossly underfunded — mind you, pretty much every single taxpayer sinkhole here has grossly underfunded state-level pensions — but it is a widespread problem.

Author(s): Mary Pat Campbell

Publication Date: 29 Sept 2021

Publication Site: STUMP at substack