Link:https://www.governing.com/finance/will-the-opeb-ostriches-ever-run-out-of-excuses

Graphic:

Excerpt:

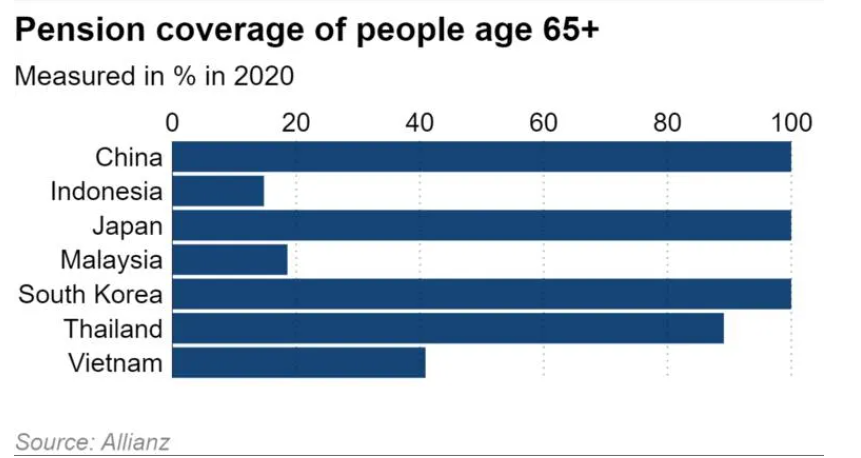

As one stalwart finance officer once told me, “Our pension funds basically sucked up all the new revenue we’d been hoping to set aside to properly fund OPEB.” Those and other priorities for spending each incremental revenue dollar continued to crowd out the opportunity to institute consistent actuarial funding for OPEB benefits; the path of least resistance for policymakers who lack foresight and a sense of fiscal responsibility has been to keep kicking the can.

So it is that between 2015 and 2019, the state and local sector had clearly sorted itself into three classes of employers: (1) those who had trimmed or modified their OPEB commitments and liabilities to sustainable levels, (2) those who had begun actuarial funding of an OPEB trust fund, and (3) those doing nothing and leaving the problem to their successors and future taxpayers.

Author(s): Girard Miller

Publication Date: 18 Jan 2022

Publication Site: Governing