Connecticut is poised to deposit an extra $3.6 billion in its cash-starved pension funds when the fiscal year closes in June, after tax revenues surged yet again on Friday.

Those supplemental payments would be on top of the $2.9 billion in required contributions Connecticut made this fiscal year to pensions for state employees and municipal teachers.

Those projections were included Friday in the latest monthly budget estimates from Gov. Ned Lamont’s administration, which also forecast a $3.8 billion surplus for the current fiscal year.

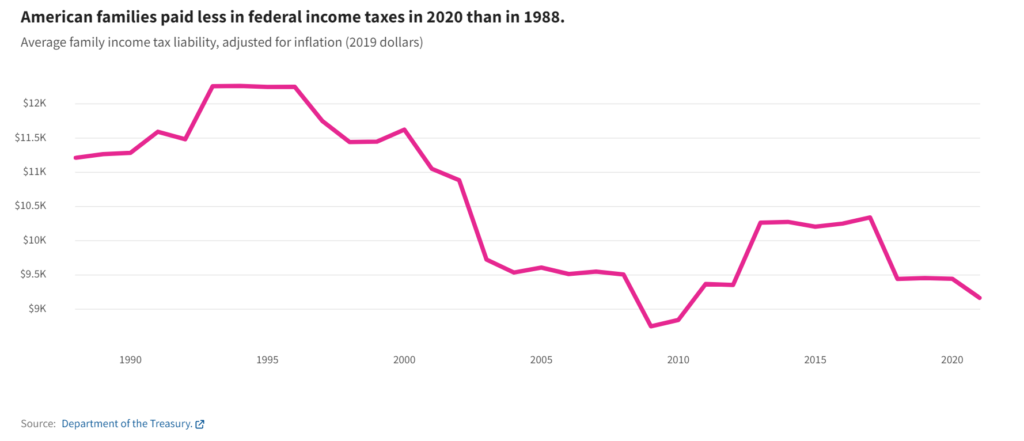

From 1988 to 1993, the average federal income tax bill for American families increased by over $1,000 in 2019 dollars. Families in the top 1%, the middle class and elderly families had increases in their federal income tax bills. But for middle-class families with children, tax bills over that time decreased.

The payroll tax changes caused the average payroll tax liability for employers and employees combined to increase by nearly $400. Payroll tax policy hasn’t changed significantly since the 1993 law.

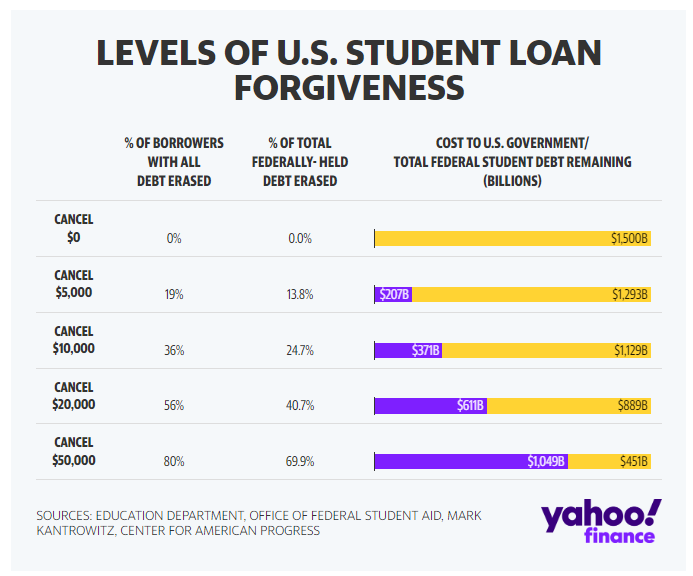

Pressley, alongside Senate Majority Leader Chuck Schumer (D-NY), and Senator Elizabeth Warren (D-MA) have repeatedly called on Biden to cancel $50,000 in student loan debt immediately via executive order on the premise that there is sufficient legal backing for the administration to do so.

The Fed researchers, using data from the New York Fed/Equifax Consumer Credit Panel, estimated the cost of two federal loan forgiveness proposals, one for $10,000 and another for $50,000. They found that limited forgiveness and placing income caps on who would be eligible would “distribute a larger share of benefits” to low-income borrowers while also reducing the cost of forgiveness.

Rep. Pressley has repeatedly stressed that women and people of color hold significant levels of student loan debt and that cancellation would represent a massively impactful form of relief given the disproportionate burden.

We use discounted cash flow analysis to measure a country’s fiscal capacity. Crucially, the discount rate applied to projected cash flows includes a GDP risk premium. We apply our valuation method to the CBO’s projections for the U.S. federal government’s deficit between 2022 and 2051 and debt in 2051. In spite of low rates, our current measure of U.S. fiscal capacity is lower than the debt/GDP ratio. Because of the backloading of projected surpluses, the duration of the surplus claim far exceeds the duration of the outstanding Treasury portfolio. This duration mismatch exposes the government to the risk of rising rates, which would trigger the need for higher tax revenue or lower spending. Reducing this risk by front-loading the surpluses also requires major fiscal adjustment.

Author(s): Zhengyang Jiang, Hanno Lustig, Stijn Van Nieuwerburgh & Mindy Z. Xiaolan

Global sovereign debt is expected to climb by 9.5% to a record $71.6 trillion in 2022, according to a new report, while fresh borrowing is also broadly set to remain elevated.

In its second annual Sovereign Debt Index, published Wednesday, British asset manager Janus Henderson projected a 9.5% rise in global government debt, driven primarily by the U.S., Japan and China but with the vast majority of countries expected to increase borrowing.

Global government debt jumped 7.8% in 2021 to $65.4 trillion as every country assessed saw borrowing increase, while debt servicing costs dropped to a record low of $1.01 trillion, an effective interest rate of just 1.6%, the report said.

However, debt servicing costs are set to rise significantly in 2022, climbing around 14.5% on a constant-currency basis to $1.16 trillion.

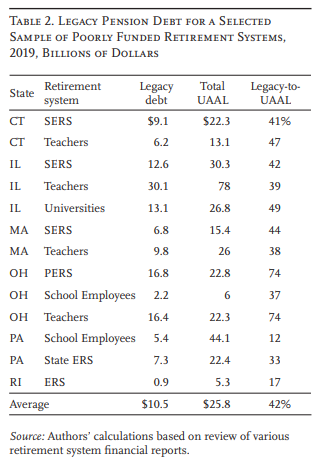

State and local policymakers face a growing pension cost burden, but often lack understanding of the root causes.

One underappreciated cause is “legacy debt” – unfunded liabilities accumulated long ago, before plans adopted modern funding practices.

Legacy debt still exists today because historical unfunded liabilities were ultimately paid in full using some of the money intended to fund later benefits.

In a sample of plans with particularly low funded ratios, legacy debt averaged more than 40 percent of unfunded liabilities.

A failure to recognize the legacy debt has provided misleading information about benefit generosity, hindering progress toward effective solutions.

Author(s): Jean-Pierre Aubry

Publication Date: April 2022

Publication Site: Center for Retirement Research at Boston College

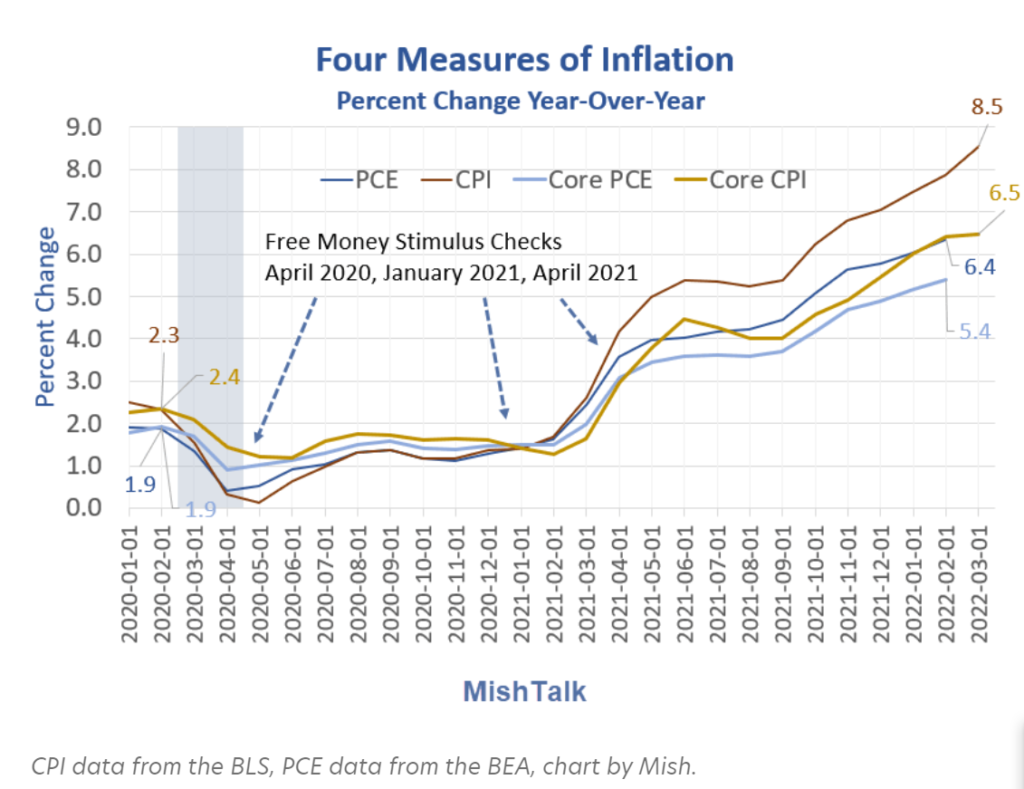

The question is not as straight forward as it looks. The gap between spending and income isn’t constant.

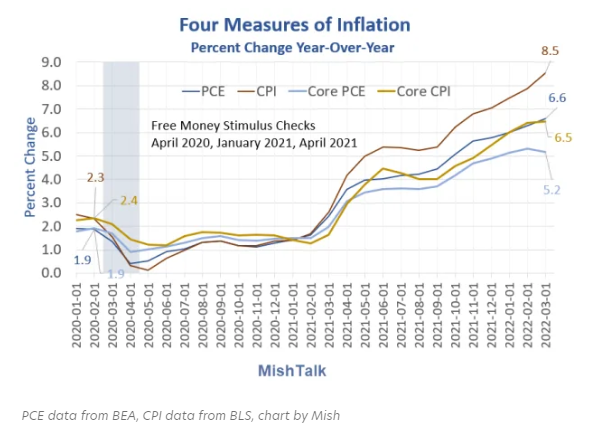

Free money that goes to bottom rung households tends to immediately get spent. The higher the rung, the more the savings. This is complicated by the fact that most of the money was supposed to go to lower tiers, and further complicated by corporate fraud, especially in round one.

More importantly, personal spending does not count mortgage paydowns, stock market or Bitcoin purchases, capital expenses for businesses, drug money, other illegal uses, or money sent to relatives overseas.

….

The Peterson Foundation reports direct checks were $292 billion in round one, $164 billion in round two, and $411 billion in round three.

There was $850 billion of direct payments to taxpayers with the biggest and most unwarranted round the last.

Spending data suggests free money, at least most of direct payments, already did enter the economy.

However, that does not factor in unpaid rent via eviction moratoriums or SNAP (Supplemental Nutrition Assistance Program), formerly Food Stamps, which I will address in a separate post.

So yes, there still could be a pile of unspent stimulus savings, possibly much higher than my $2 trillion summation estimate, again with my caveats on investments, sending money overseas, etc.

Tardy federal budgets are nothing new in Washington. According to the Tax Policy Center, Congress has only completed the budgetary process in a timely fashion, which requires passing all 12 appropriations bills prior to October 1, four times since fiscal year (FY) 1977. The last time Congress’ budgetary process worked as expected was FY 1997, more than two decades ago.

When the budget does not pass on time, Congress must pass a continuing resolution (CR) to avoid a government shutdown. Since continuing resolutions typically maintain departmental funding at prior-year levels, they do not signal the policy choices ultimately made in the budget process. As a result, federal managers must begin the fiscal year without a clear direction as to whether they should be increasing or decreasing staff and non-employee operational expenditures. If a federal agency or department ultimately receives a significant funding increase or funding cut in the final appropriations bill, managers may have insufficient time to respond efficiently.

While federal budgeting has been broken for some time, the situation in 2022 is especially bad. Over five months into the budgetary year, the House Rules Committee produced a 2,741-page omnibus budget bill in the wee hours of March 9, just hours before the bill’s scheduled vote on the House floor.

The war in Ukraine and subsequent international sanctions have triggered a bank run in Russia. But this is no ordinary run—it may become a run on the central bank itself, one that holds important lessons for introducing central bank digital currencies.

Reports show Russians lining up at ATMs to withdraw their cash. For now, the run is largely driven by fears of withdrawal limits and the anticipation that credit cards and electronic means of payments will cease to function. If that happens, cash at hand is the better alternative. For that scenario, central banks know what to do: provide solvent banks with plenty of liquidity against good collateral, as Walter Bagehot recommended.

But will that be all? As Western countries freeze the Russian central bank’s reserves and limit the ability of banks to transact internationally, the exchange rate of the ruble has collapsed, falling by more than 40 percent. Prices for ordinary goods may begin to rise, perhaps dramatically so. If that happens, then rubles would no longer be a good store of value. Russians may seek to convert them into foreign currency, but that’s hard to do with the current sanctions. Consequently, they may start to hoard goods instead, dumping their cash as they go along. The situation would no longer be a run on specific goods, but a run away from fiat money and toward goods—a run, in other words, on the central bank.

Author(s): Linda Schilling, Jesús Fernández-Villaverde, Harald Uhlig

Tax cuts remain a powerful tool to entice people and firms, and the pandemic has triggered a new tax war. After the lockdowns, states and cities predicted unprecedented revenue drops. Instead, economies bounced back quickly from the pandemic, partly because of widespread adoption of remote work and extensive federal aid from the Trump and Biden administrations — hundreds of billions of dollars in unemployment benefits (which kept individuals spending money), business loans and funding for local governments to fight COVID-19.

The March 2021 Biden stimulus then provided local governments with an unprecedented $350 billion to bolster their budgets. The revenue gusher has produced state budget surpluses where experts had only recently predicted steep deficits.

Nearly a dozen states, mostly Republican-governed, have used the windfall to cut taxes. Idaho reduced its corporate and individual tax rates and shrank its income-tax brackets from seven to five, producing a $163 million tax cut for residents and businesses. The state also sent $220 million in rebates to everyone who filed tax returns in 2019.

….

Advocates for higher taxes often say that the levies don’t drive away wealthy individuals or businesses. When New Jersey raised taxes on the wealthy in November 2020, Democratic Gov. Phil Murphy said, “When people say folks are going to leave, there’s no research anywhere that suggests that happens.”

Yet New Jersey, with taxes on the wealthy and on businesses long ranking among the nation’s highest, ranked a dismal 42nd in economic growth over the five years preceding the pandemic, according to one study, and it has been an economic laggard for two decades. Voters in this overwhelmingly Democratic state showed their disapproval in giving incumbent Murphy an extremely narrow victory in his November reelection bid. Polls showed that most voters favored the Republican position on cutting taxes over Murphy’s.