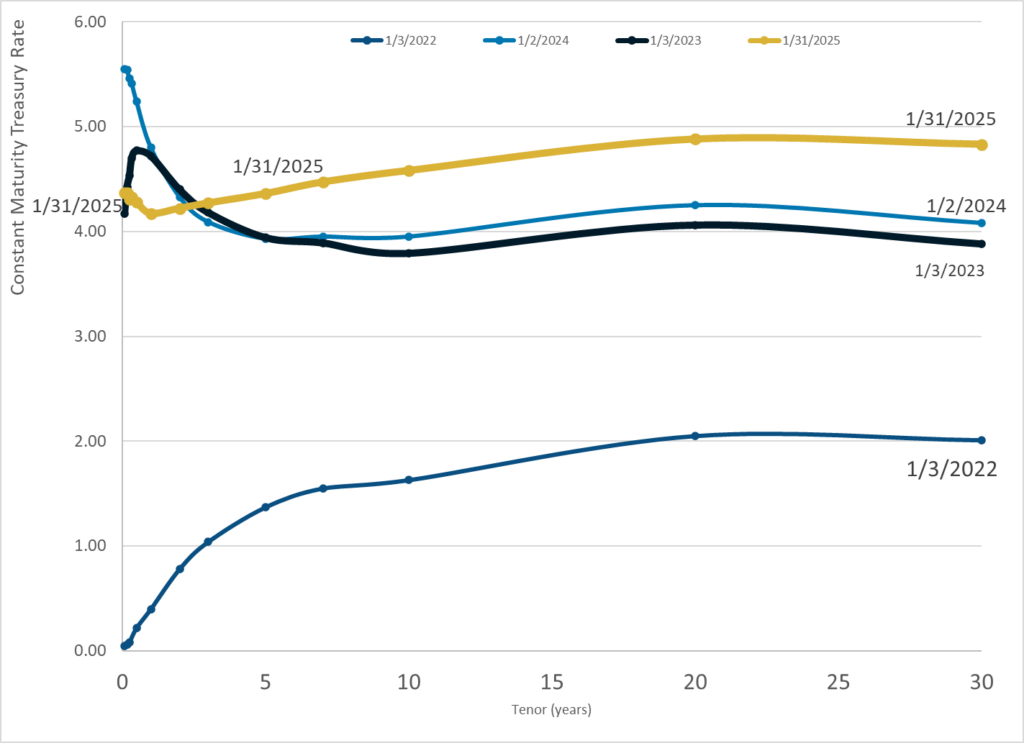

Graphic:

Publication Date: 31 Jan 2025

Publication Site: Treasury Dept

All about risk

Graphic:

Publication Date: 31 Jan 2025

Publication Site: Treasury Dept

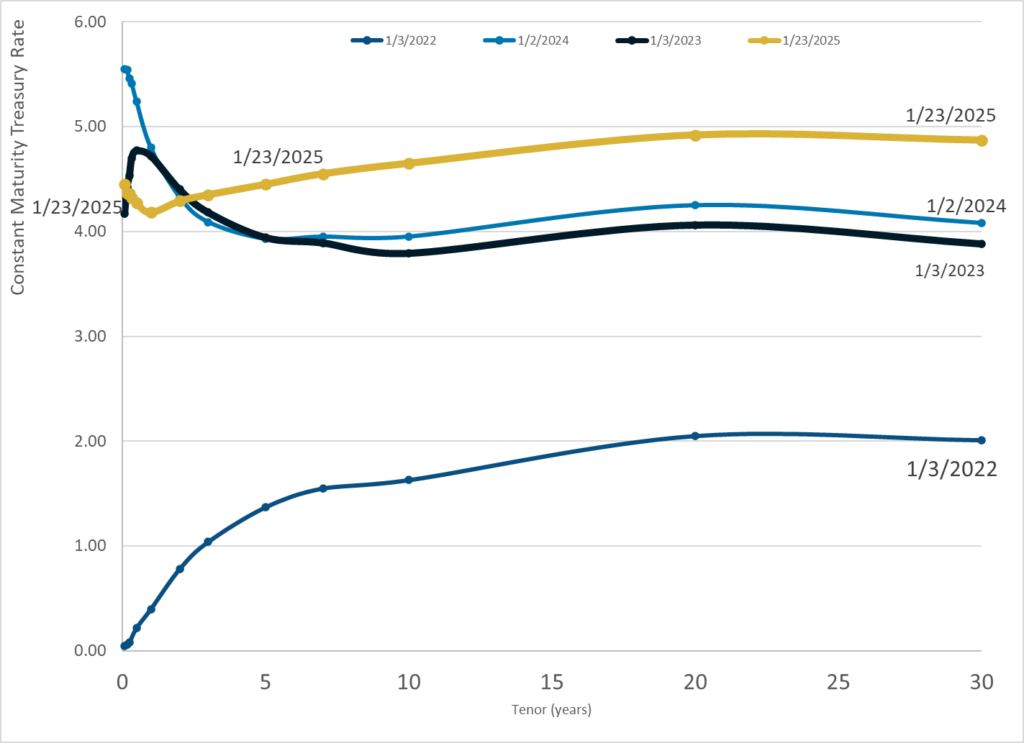

Graphic:

Publication Date: 23 Jan 2025

Publication Site: Treasury Department

Excerpt:

The Ohio State Teachers’ Retirement System cannot invest its way to a permanent COLA, Brian Grinnell, former chief actuary of the $97.3 billion pension fund, told Pensions & Investments.

Grinnell left the pension fund in May after more than 10 years as its chief actuary. In a Sept. 27 interview, he said his responsibilities were primarily to help STRS staff and the board understand the risks the pension fund has faced and help develop a forward-looking plan to make decisions with long-term outcomes in mind.

In his interview, he said, “I was not comfortable with the direction the plan was headed, and I didn’t feel like my continued participation would be positive.”

….

The pension reform law, SB342, was one of five laws that addressed funding issues at all five of Ohio’s state retirement systems and was drafted as a result of severe stock market declines that came from the Great Recession in 2008 and 2009. Among all the state systems, STRS was the worst off in 2012 with a funding ratio of 57.6% as of June 30 of that year. Additionally, the amortization period for the retirement system’s unfunded pension liabilities under the STRS defined benefit plan had become infinite — meaning that it would never become fully funded.

Grinnell said STRS has had to contend with the challenge of being an extremely mature pension fund: Essentially, there is more money being sent out to retirees receiving benefits now relative to the future contributions the pension fund can expect from current and future teachers.

“Here’s where STRS is a little bit of an unusual situation because it is a fixed-rate plan,” Grinnell said, “so both the benefits and the contributions are essentially fixed by statute. So most plans, if they have a bad year in terms of investment performance, the contribution rate goes up the following year to fill that hole. That doesn’t happen at STRS.”

Grinnell said when a pension fund is both a mature plan and has that fixed-rate contribution and fixed benefits, it’s very difficult to recover from any kinds of market downturns. He noted that all five of Ohio’s state retirement systems have that fixed-rate structure.

“Most other public pensions do not have that kind of structure,” he said, “and I think that tends to work all right for an immature plan, a plan that’s growing and not paying out a lot of benefits relative to the contributions.”

Author(s): Rob Kozlowski

Publication Date: 2 October 2024

Publication Site: Pensions & Investments

Link: https://content.naic.org/sites/default/files/capital-markets-market-buzz-private-credit-plr.pdf

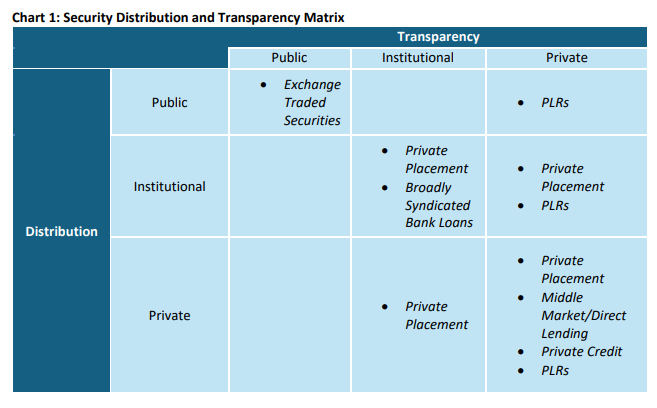

Graphic:

Excerpt:

The terms private credit and private letter ratings (PLRs) have unintentionally elicited some confusion

about their respective meanings. While there is no standardized definition, and the term may be used

differently by market participants, private credit generally refers to debt, or debt-like, securities that are

not publicly issued or traded. On the other hand, PLRs refer to credit opinions that are assigned to

privately rated securities by credit rating providers and are only communicated to the issuer and a

specified group of investors.

To bring some clarity, at least with respect to how the NAIC views them, these terms can be characterized

in two dimensions: 1) distribution; and 2) transparency.

Publication Date: 30 July 2024

Publication Site: NAIC Capital Markets Bureau Market Buzz

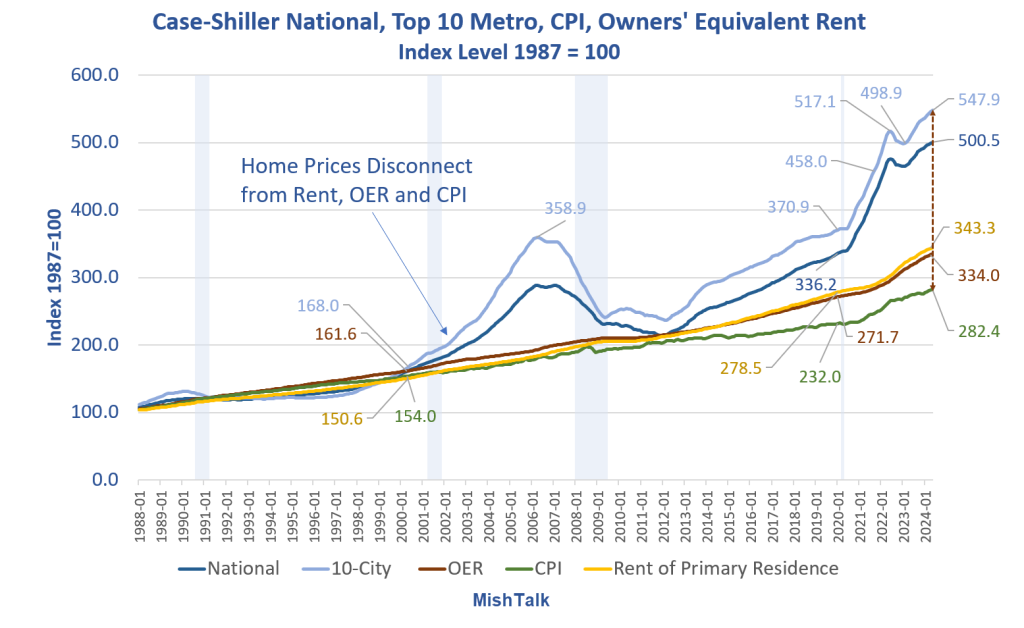

Graphic:

Excerpt:

Housing affordability continues to soar out of reach of most buyers. Not only are prices at a new record level, mortgage rates remain close to 7.0 percent.

Chart Notes

Author(s): Mike Shedlock (Mish)

Publication Date: 30 July 2024

Publication Site: MishTalk

Link:

https://content.naic.org/sites/default/files/capital-markets-special-reports-bank-loans-ye2023_0.pdf

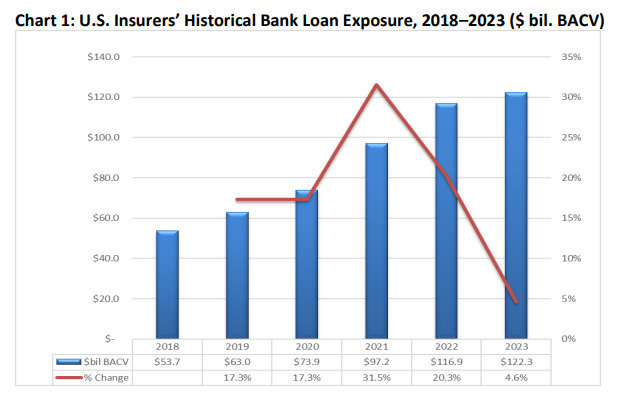

Graphic:

Executive Summary:

Bank loan investments increased to about $122 billion in book/adjusted carrying value (BACV)

at year-end 2023 from $117 billion at year-end 2022.Despite the 4.6% growth, bank loansremained at 1.4% of U.S. insurers’ total cash and invested

assets at year-end 2023—the same as year-end 2022.Approximately 70% of U.S. insurers’ bank loan investments were acquired, and 85% were held

by life companies.In particular, large life companies, or those with more than $10 billion in assets under

management, accounted for 82% of U.S. insurers’ bank loan exposure, up from nearly 80% in

2022.The top 25 insurance companies accounted for 75% of U.S. insurers’ total bank loan

investments at year-end 2023; the top 10 accounted for about 60%.Improvement in credit quality for U.S. insurer-bank loans continued, evidenced by a fourpercentage-point increase in those carrying NAIC 1 and NAIC 2 designations and a

corresponding four-percentage-point decrease in bank loans carrying NAIC 3 and NAIC 4

designations.

Author(s): Jennifer Johnson

Publication Date: 16 July 2024

Publication Site: NAIC Capital Markets Special Report

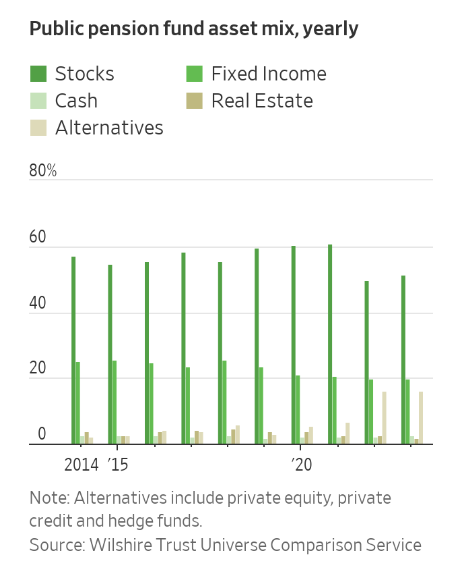

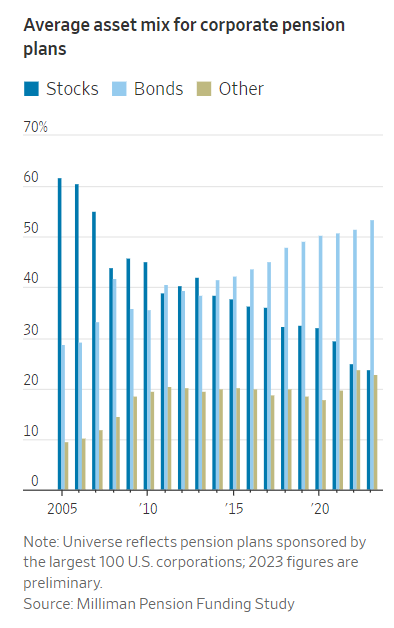

Graphic:

Excerpt:

Stock portfolios at large pension funds had a blockbuster run. Now, managers are cashing out.

Corporate pension funds are shifting money into bonds. State and local government funds are swapping stocks for alternative investments. The nation’s largest public pension, the California Public Employees’ Retirement System, is planning to move close to $25 billion out of equities and into private equity and private debt.

Like investors of all kinds, the funds are slowly adapting to a world of yield, where they can get sizable returns on risk-free assets. That is rippling throughout markets, as investors assess how much risk they want to take on. Moving out of stocks could mean surrendering some potential gains. Hold too much, for too long, and prices might fall.

Author(s): Heather Gillers, Charley Grant

Publication Date: 18 Apr 2024

Publication Site: WSJ

Excerpt:

The Dallas Police and Fire Pension System — which as been severely underfunded for years — still has about 25% of its assets tied up in private investments.

That’s according to pension system official’s briefing during Thursday’s Ad Hoc Committee on Pensions meeting.

Those include investments in an energy fund, natural resources — and assets in real estate. The private investments were deemed “legacy” assets that the pension system still maintains.

It was risky private investments that landed the system in the situation it’s in now — with over a billion dollars in unfunded liabilities.

“Currently we’ve gotten that down to 26%,” Dallas Police and Fire Pension System Chief Investment Officer Ryan Wagner said during the meeting.

Author(s): Nathan Collins

Publication Date: 9 Feb 2024

Publication Site: KERA News

Graphic:

Excerpt:

The Financial Times made its interview with departing CalSTRS’ Chief Investment Officer Chris Ailman its lead story yesterday: Private equity should share more wealth with workers, says US pension giant. The Financial Times was too polite to say so, but Ailman could lay claim to being the best large public pension fund chief investment officer. CalSTRS, which manages the pensions of California teachers, is in the same general size league as its Sacramento sister CalPERS, and regularly outperforms CalPERS by a meaningful margin.

….

It’s hard to know where to begin with this. Limited partners like CalSTRS, who are, in Wall Street parlance, the money, have not even been able to get basic disclosures from the general partners like how much in total the private equity firms hoover out in fees and expenses, despite many years of pleading. Mind you, it’s a requirement for a fiduciary to evaluate the costs and risks of any investment, yet these investors have accepted this abuse.

Limited partners don’t get P&Ls of portfolio companies. They don’t get independent valuations even though that is considered to be essential for every other type of investment. So it’s ludicrous to think that general partners will share money with one of the very weakest parties in the picture, mere workers, when they won’t give information to the limited partners.

Someone new to this topic might wonder why limited partners don’t say “no”. The reason is they perceive private equity to be necessary for them to earn enough to reduce their level of underfunding, which in the public pension fund world is typically pretty bad. To make up for the shortfalls, pension funds like CalPERS and CalSTRS have also been increasing the amount they charge to cities, counties, and other local government entities. These pension costs are taking up larger and larger proportions of these budgets, creating concern and anger.

Author(s): Yves Smith

Publication Date: 16 Feb 2024

Publication Site: naked capitalism

Excerpt:

The primary responsibility of the $8.4 billion Philadelphia pension fund is to assure the continuing financial security promised to city workers upon retirement. The welfare of city employees, along with all Philadelphians, depends on the economic and social well-being of the city itself. Therefore, the Philadelphia Public Banking Coalition has proposed that the city pension fund invest $168 million, 2% of its portfolio, in local economically targeted investments to fund projects that benefit Philadelphians.

These investments would address policy goals while achieving returns as high or higher than many of the fund’s current asset classes. Currently, the 2023 pension fund investment policy describes risky investments in options, futures, forwards, and swap agreements. And there’s a precedent for public policy considerations, for example, in limitations on investments in Russian companies, private prisons, and arms manufacturers. The current portfolio exhibits a strong real estate focus but without preference for Philadelphia projects.

Below are just a few of the possible opportunities for targeted investments that would strengthen the health of Philadelphia’s economy.

Author(s): Stan Shapiro and Peter Winslow, For The Inquirer

Publication Date: 14 Feb 2024

Publication Site: The Philadelphia Inquirer

Excerpt:

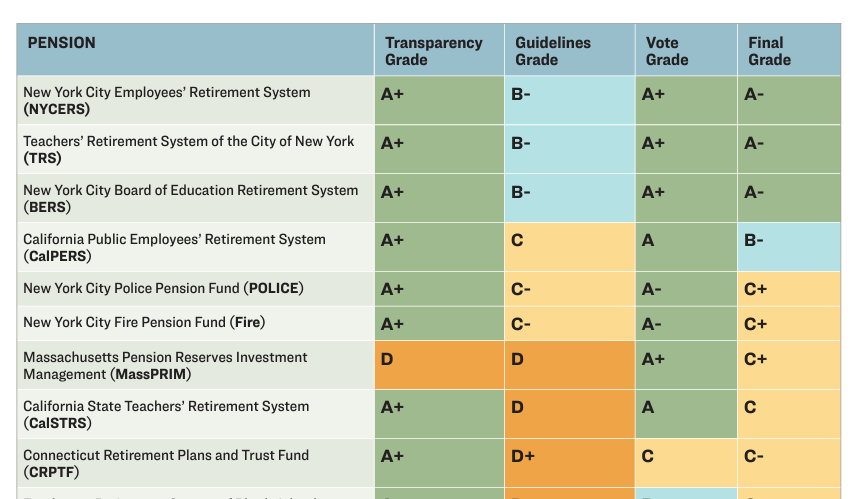

“Too few” public pension funds are addressing climate-related financial risk when it comes to proxy voting, according to a report released Jan. 23 by nonprofit organizations Sierra Club, Stand.earth and Stop the Money Pipeline.

The report, “The Hidden Risk in State Pensions: Analyzing State Pensions’ Responses to the Climate Crisis in Proxy Voting,” looked at 24 public pension funds with a collective $2 trillion in assets, including the $241.7 billion New York City Retirement Systems and state pension funds in California, Colorado, Connecticut, Delaware, Illinois, Maine, Maryland, Massachusetts, Minnesota, Nevada, New Mexico, Oregon, Rhode Island, Vermont, Washington and Wisconsin.

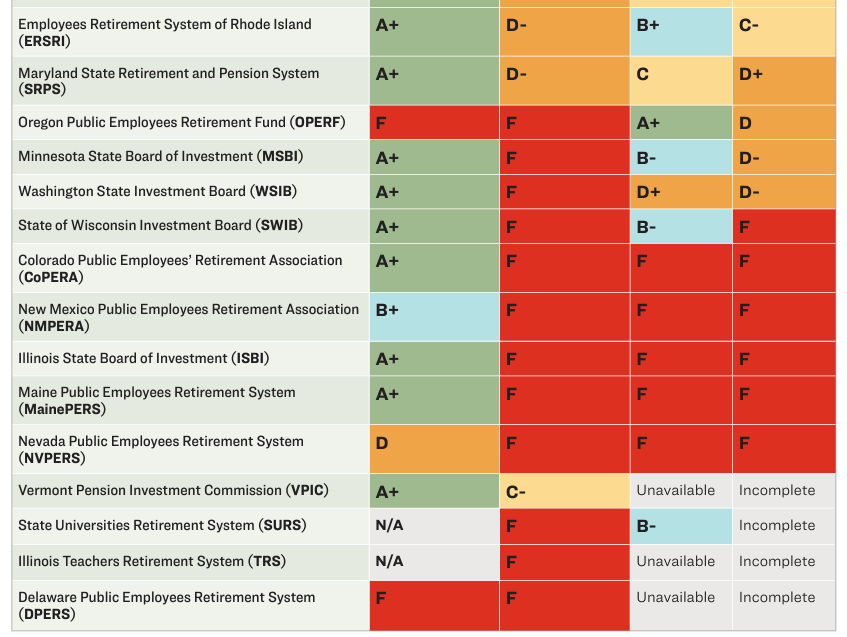

The pension funds were graded on their proxy-voting guidelines, proxy-voting records, and data transparency.

On proxy-voting guidelines, no pension system received an A grade, but three of the five New York City pension funds covering city employees, the Board of Education and teachers, earned a B for addressing systemic risk and climate resolutions. Half of the 24 pension funds studied earned an F.

….

“The findings of this analysis are clear: Far too few state pensions are taking adequate steps to address climate-related financial risks and protect their members’ hard-earned savings, raising serious concerns about their execution of fiduciary duty,” the report’s executive summary said.

….

Amy Gray, associate director of climate finance for Stand.earth, said it is disappointing to see many funds not using proxy-voting strategies to address the financial risks of climate change. “This report is a stark reminder that pension funds can — and must — do so much more to wield their massive investor power,” Gray said in the news release.

Author(s): Hazel Bradford

Publication Date: 23 Jan 2024

Publication Site: P&I

Report PDF: https://stand.earth/wp-content/uploads/2024/01/The-Hidden-Risk-in-State-Pensions-Report.pdf

Graphic:

Excerpt:

A first-of-its-kind report, the Hidden Risk analyzes the proxy voting records and proxy voting guidelines of the 19 public pensions that are in states where a state financial officer has indicated it is a priority issue both to advocate for more sustainable, just, and inclusive firms and markets , and to protect against climate risk.

Ahead of the 2024 shareholder season, a first-of-its-kind report “The Hidden Risk in State Pensions: Analyzing State Pensions’ Responses to the Climate Crisis in Proxy Voting,” from Stand.earth, Sierra Club and Stop the Money Pipeline, analyzes proxy voting records, proxy guidelines, and voting transparency of 24 public pension funds in the USA collectively representing over $2 trillion in assets under management (AUM).

These pensions are based in states where a state financial officer is a member of For the Long Term, a network that advocates for more sustainable, just, and inclusive firms and markets and strives to protect markets against climate risk.

The pensions analyzed include the pension systems of New York City and the states of California, Colorado, Connecticut, Delaware, Illinois, Maine, Maryland, Massachusetts, Minnesota, Nevada, New Mexico, Oregon, Rhode Island, Vermont, Washington, and Wisconsin.

Author(s):

Stand.earth

Sierra Club

Stop The Money Pipeline

Publication Date: 23 Jan 2024

Publication Site: Stand.earth