Graphic:

Publication Date: 21 Feb 2025

Publication Site: Treasury Department

All about risk

Graphic:

Publication Date: 21 Feb 2025

Publication Site: Treasury Department

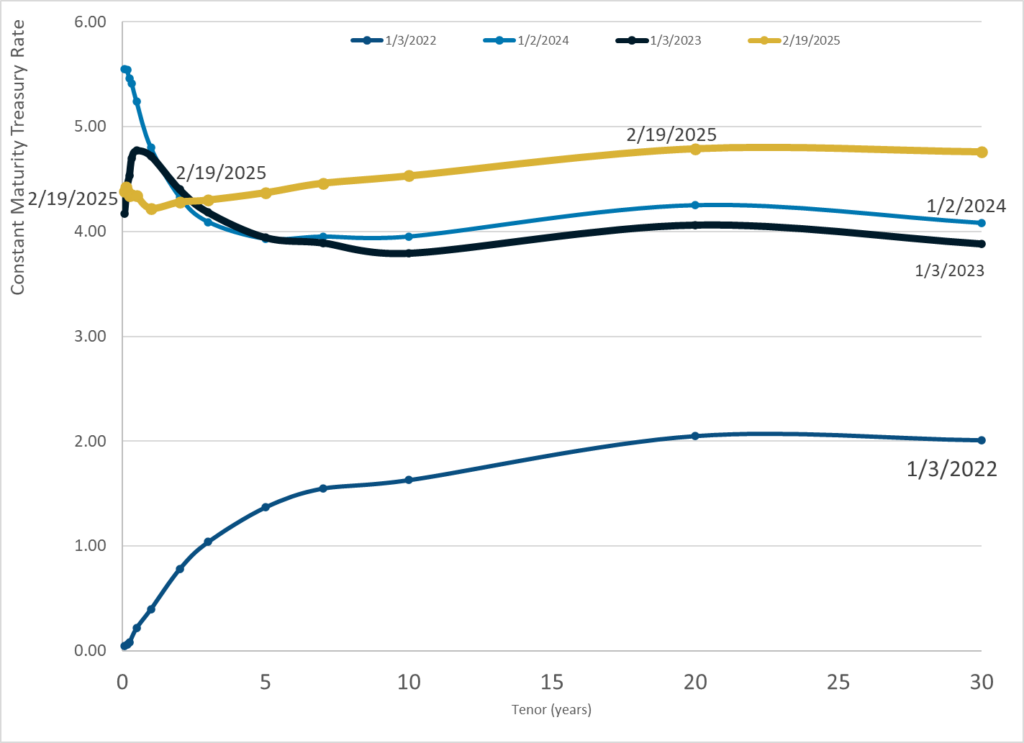

Graphic:

Publication Date: 19 Feb 2025

Publication Site: Treasury Department

Graphic:

Excerpt:

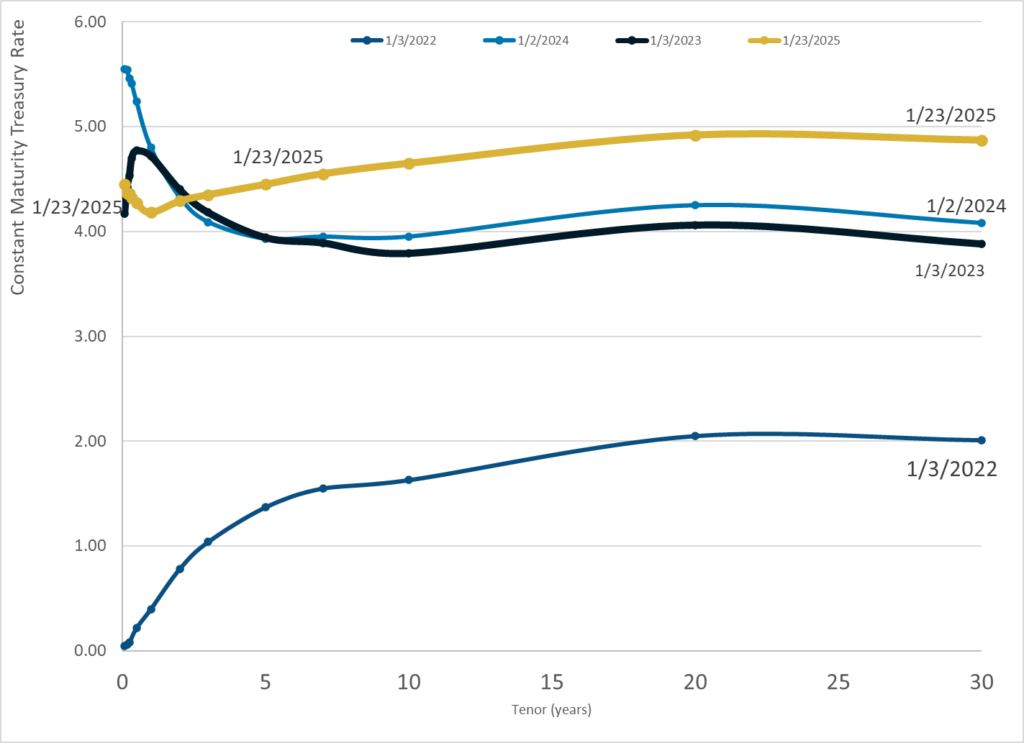

Effective with the inaugural auction of the new benchmark 6-week Treasury bill on Tuesday, February 18, 2025, Treasury plans to include 6-week bill prices in its input data set for the daily yield curve. Treasury also plans to add a 1.5-month CMT to the Daily Treasury Par Yield Curve Rates and 6-week bill rates to the Daily Treasury Bill Rates that it publishes.

Changes to the published tables and data files to accommodate the additional rates will appear beginning in the evening on February 14, 2025.

Publication Date: 18 Feb 2025

Publication Site: Treasury Dept

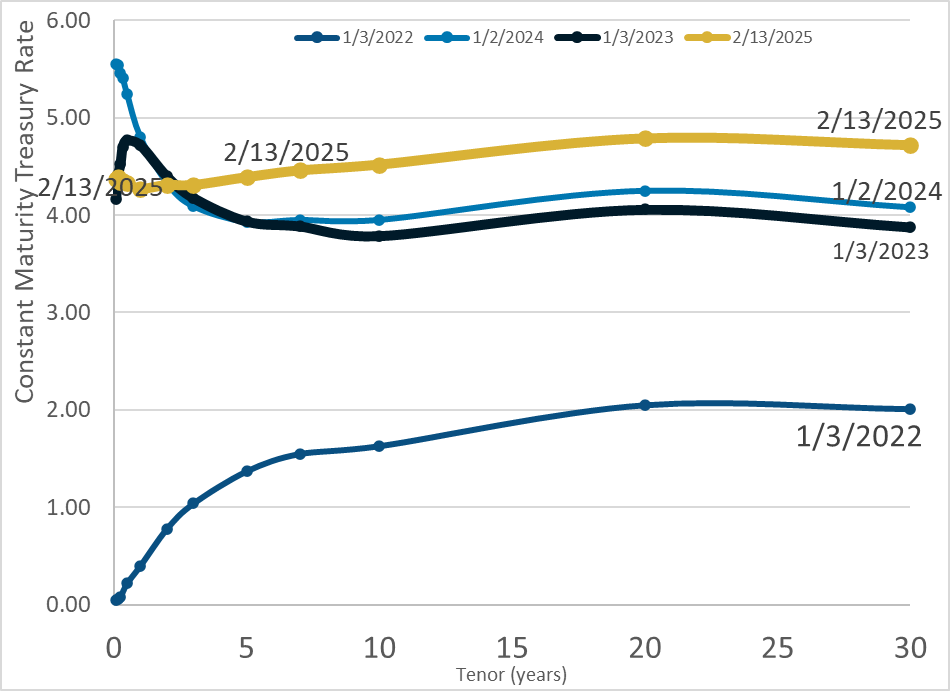

Graphic:

Publication Date: 13 Feb 2025

Publication Site: Treasury Dept

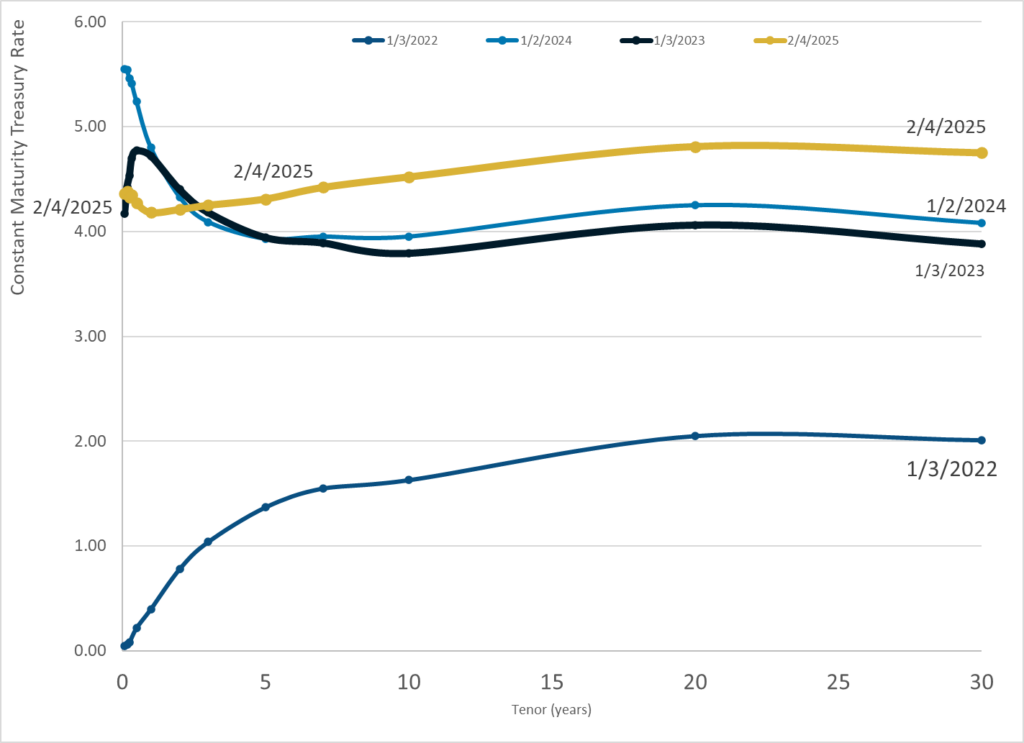

Graphic:

Publication Date: 4 Feb 2025

Publication Site: Treasury Dept

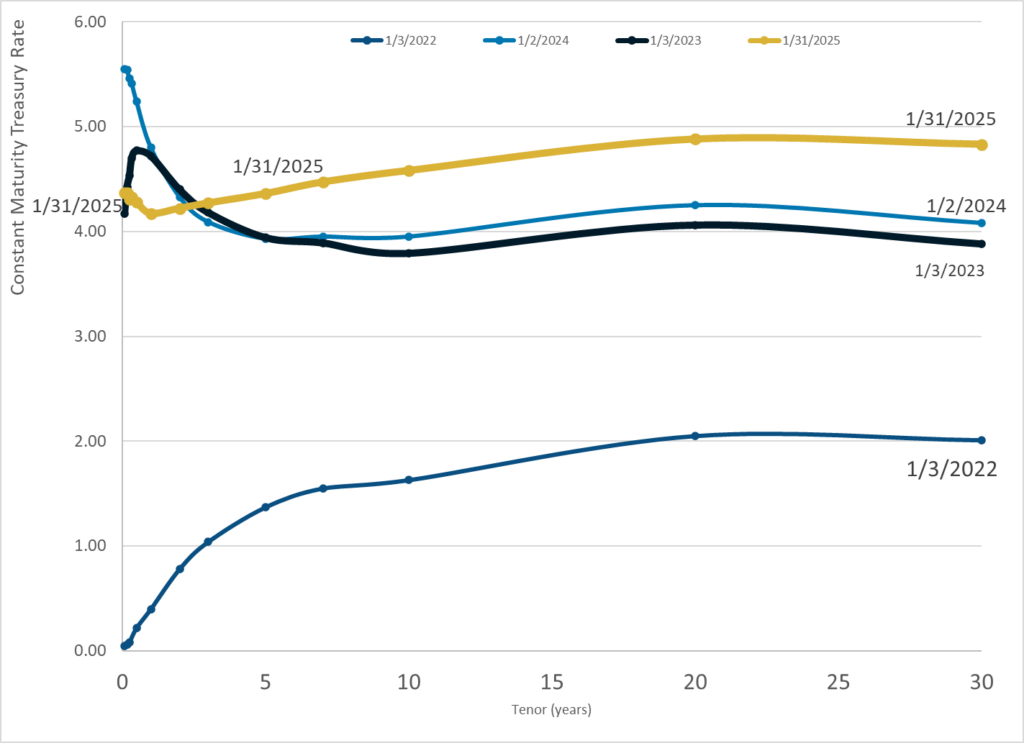

Graphic:

Publication Date: 31 Jan 2025

Publication Site: Treasury Dept

Graphic:

Publication Date: 23 Jan 2025

Publication Site: Treasury Department

Excerpt:

The Ohio State Teachers’ Retirement System cannot invest its way to a permanent COLA, Brian Grinnell, former chief actuary of the $97.3 billion pension fund, told Pensions & Investments.

Grinnell left the pension fund in May after more than 10 years as its chief actuary. In a Sept. 27 interview, he said his responsibilities were primarily to help STRS staff and the board understand the risks the pension fund has faced and help develop a forward-looking plan to make decisions with long-term outcomes in mind.

In his interview, he said, “I was not comfortable with the direction the plan was headed, and I didn’t feel like my continued participation would be positive.”

….

The pension reform law, SB342, was one of five laws that addressed funding issues at all five of Ohio’s state retirement systems and was drafted as a result of severe stock market declines that came from the Great Recession in 2008 and 2009. Among all the state systems, STRS was the worst off in 2012 with a funding ratio of 57.6% as of June 30 of that year. Additionally, the amortization period for the retirement system’s unfunded pension liabilities under the STRS defined benefit plan had become infinite — meaning that it would never become fully funded.

Grinnell said STRS has had to contend with the challenge of being an extremely mature pension fund: Essentially, there is more money being sent out to retirees receiving benefits now relative to the future contributions the pension fund can expect from current and future teachers.

“Here’s where STRS is a little bit of an unusual situation because it is a fixed-rate plan,” Grinnell said, “so both the benefits and the contributions are essentially fixed by statute. So most plans, if they have a bad year in terms of investment performance, the contribution rate goes up the following year to fill that hole. That doesn’t happen at STRS.”

Grinnell said when a pension fund is both a mature plan and has that fixed-rate contribution and fixed benefits, it’s very difficult to recover from any kinds of market downturns. He noted that all five of Ohio’s state retirement systems have that fixed-rate structure.

“Most other public pensions do not have that kind of structure,” he said, “and I think that tends to work all right for an immature plan, a plan that’s growing and not paying out a lot of benefits relative to the contributions.”

Author(s): Rob Kozlowski

Publication Date: 2 October 2024

Publication Site: Pensions & Investments

Link: https://content.naic.org/sites/default/files/capital-markets-market-buzz-private-credit-plr.pdf

Graphic:

Excerpt:

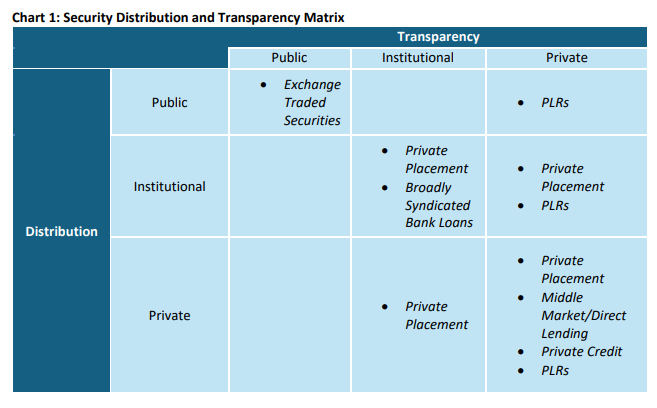

The terms private credit and private letter ratings (PLRs) have unintentionally elicited some confusion

about their respective meanings. While there is no standardized definition, and the term may be used

differently by market participants, private credit generally refers to debt, or debt-like, securities that are

not publicly issued or traded. On the other hand, PLRs refer to credit opinions that are assigned to

privately rated securities by credit rating providers and are only communicated to the issuer and a

specified group of investors.

To bring some clarity, at least with respect to how the NAIC views them, these terms can be characterized

in two dimensions: 1) distribution; and 2) transparency.

Publication Date: 30 July 2024

Publication Site: NAIC Capital Markets Bureau Market Buzz

Graphic:

Excerpt:

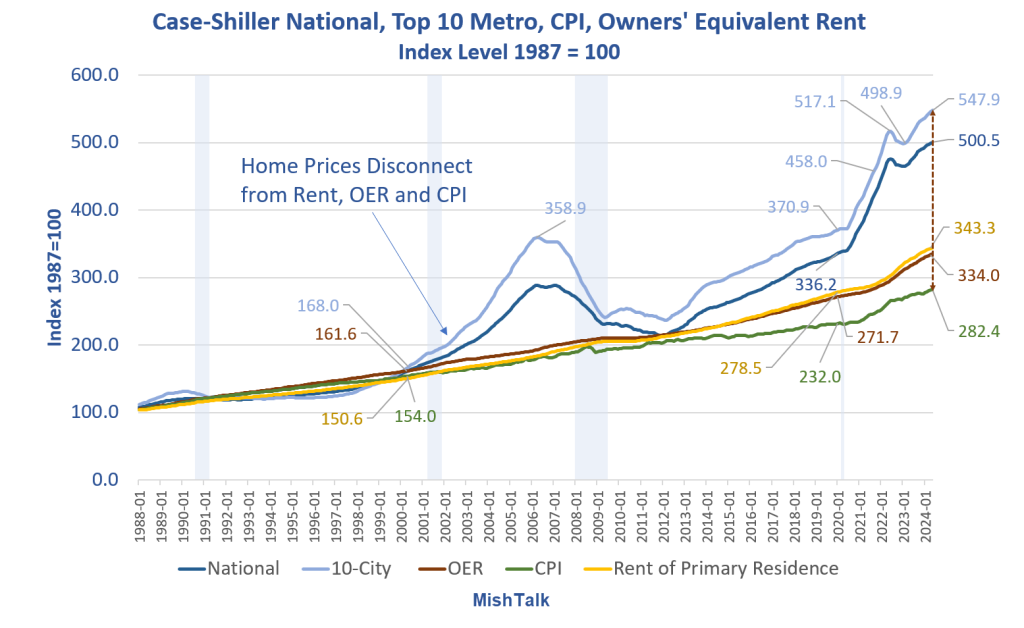

Housing affordability continues to soar out of reach of most buyers. Not only are prices at a new record level, mortgage rates remain close to 7.0 percent.

Chart Notes

Author(s): Mike Shedlock (Mish)

Publication Date: 30 July 2024

Publication Site: MishTalk

Link:

https://content.naic.org/sites/default/files/capital-markets-special-reports-bank-loans-ye2023_0.pdf

Graphic:

Executive Summary:

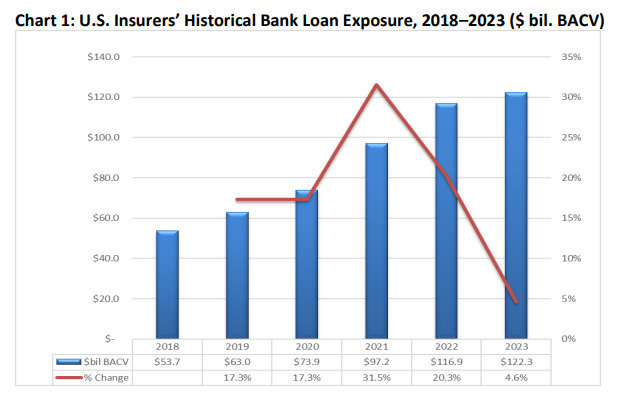

Bank loan investments increased to about $122 billion in book/adjusted carrying value (BACV)

at year-end 2023 from $117 billion at year-end 2022.Despite the 4.6% growth, bank loansremained at 1.4% of U.S. insurers’ total cash and invested

assets at year-end 2023—the same as year-end 2022.Approximately 70% of U.S. insurers’ bank loan investments were acquired, and 85% were held

by life companies.In particular, large life companies, or those with more than $10 billion in assets under

management, accounted for 82% of U.S. insurers’ bank loan exposure, up from nearly 80% in

2022.The top 25 insurance companies accounted for 75% of U.S. insurers’ total bank loan

investments at year-end 2023; the top 10 accounted for about 60%.Improvement in credit quality for U.S. insurer-bank loans continued, evidenced by a fourpercentage-point increase in those carrying NAIC 1 and NAIC 2 designations and a

corresponding four-percentage-point decrease in bank loans carrying NAIC 3 and NAIC 4

designations.

Author(s): Jennifer Johnson

Publication Date: 16 July 2024

Publication Site: NAIC Capital Markets Special Report

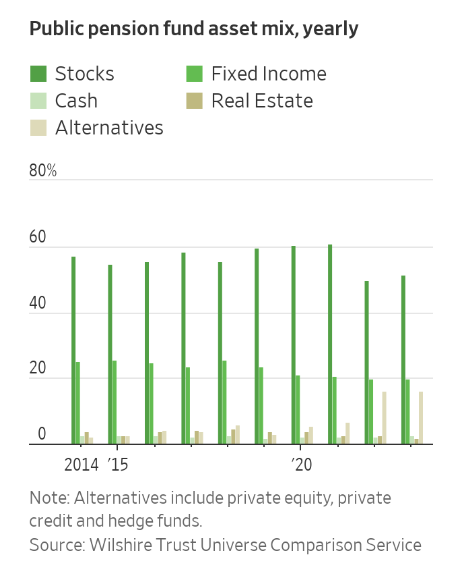

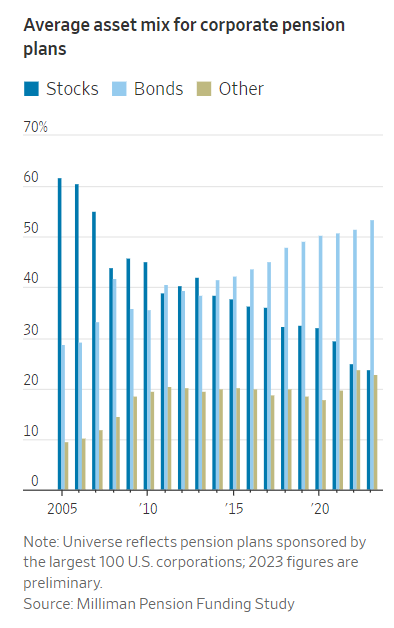

Graphic:

Excerpt:

Stock portfolios at large pension funds had a blockbuster run. Now, managers are cashing out.

Corporate pension funds are shifting money into bonds. State and local government funds are swapping stocks for alternative investments. The nation’s largest public pension, the California Public Employees’ Retirement System, is planning to move close to $25 billion out of equities and into private equity and private debt.

Like investors of all kinds, the funds are slowly adapting to a world of yield, where they can get sizable returns on risk-free assets. That is rippling throughout markets, as investors assess how much risk they want to take on. Moving out of stocks could mean surrendering some potential gains. Hold too much, for too long, and prices might fall.

Author(s): Heather Gillers, Charley Grant

Publication Date: 18 Apr 2024

Publication Site: WSJ