Link: https://content.naic.org/sites/default/files/JIR-ZA-40-10-EL.pdf

Graphic:

Excerpt:

RETHINKING UNINSURABILITY While many have viewed insurability as a binary choice with respect to a risk (i.e., insurable or uninsurable), insurability is more appropriately considered on a continuum, ranging from easy-to-insure, such as automobile or life insurance, to difficult-to-insure, such as pandemic, loss of the electrical grid, and other extreme catastrophic risks.

FRAMEWORK The role of private and public sectors in dealing with risks that are difficult-to-insure should be to develop strategies that enable a greater degree of insurability. To do so, the framework suggests that policymakers consider three fundamental options in dealing with the insurance industry:

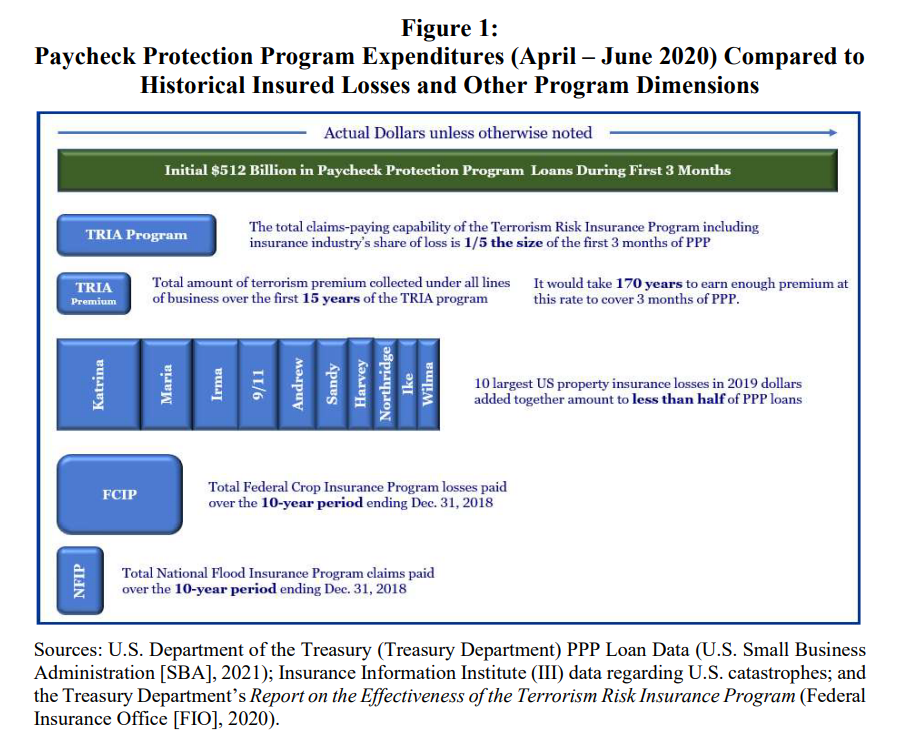

Status Quo (SQ) –This option (SQ) contemplates a similar dynamic to that experienced with COVID-19, wherein businesses, nonprofits, and local governments found limited (if any) insurance coverage for their losses and ex post relief programs funded by the government.

Service Provider (SP) – This option (SP) contemplates an administrative, non-risk-bearing role for the insurance industry while the entire cost of claims would be publicly financed.

Service and Risk (SR) –In addition to its role as a service provider as characterized by SP, this option (SR) would expect insurers to commit capital – in an amount that does not threaten their financial viability – to cover a specified layer or other defined element of losses.

Author(s): Howard Kunreuther, Jason Schupp

Publication Date: 2021

Publication Site: NAIC