Insurance companies that have long said they’ll cover anything, at the right price, are increasingly ruling out fossil fuel projects because of climate change – to cheers from environmental campaigners.

More than a dozen groups that track what policies insurers have on high-emissions activities say the industry is turning its back on oil, gas and coal.

The alliance, Insure Our Future, said Wednesday that 62% of reinsurance companies – which help other insurers spread their risks – have plans to stop covering coal projects, while 38% are now excluding some oil and natural gas projects. (The Insure Our Future report on re/insurers’ fossil fuel activities can be viewed here).

In part, investors are demanding it. But insurers have also begun to make the link between fossil fuel infrastructure, such as mines and pipelines, and the impact that greenhouse gas emissions are having on other parts of their business.

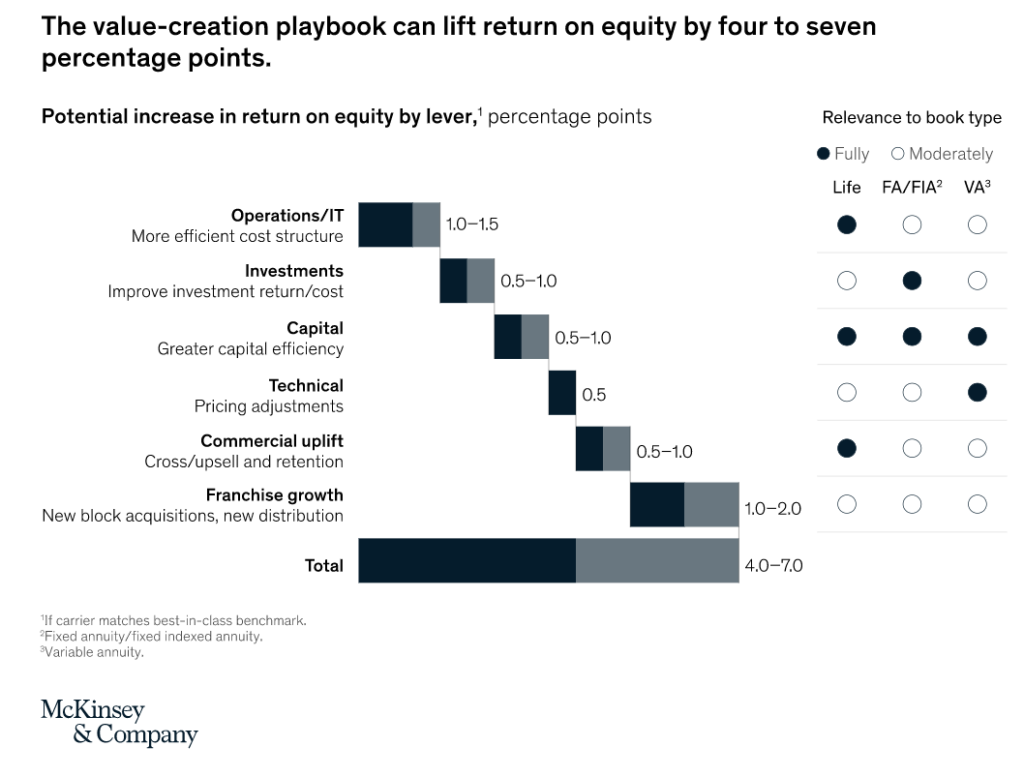

Once they’ve acquired a book, firms can turn their attention to driving value. Building on our guidelines for closed-book value creation, owners have six levers that can collectively improve ROE by up to four to seven percentage points (exhibit):

Investment performance: optimization of the SAA and delivery of alpha within the SAA

Capital efficiency: optimization of balance-sheet exposures—for example, active management of duration gaps

Operations/IT improvement: reduction of operational costs through simplification and modernization

Technical excellence: improvement of profitability through price adjustments, such as reduced surplus sharing

Commercial uplift: cross-selling and upselling higher-margin products

Franchise growth: acquiring new blocks or new distribution channels

Most PE firms view the first lever, investment performance, as the main way to create value for the insurer, as well as for themselves. This lever will grow in importance if yields and spreads continue to decline. Leading firms typically have deep skills in core investment-management areas, such as strategic asset allocation, asset/liability management, risk management, and reporting, as well as access to leading investment teams that have delivered alpha.

Capital efficiency is also well-trod ground, and for private insurers it presents a greater opportunity given their different treatment under generally accepted accounting principles, (GAAP), enabling them to apply a longer-term lens and reduce the cost of hedging. However, most firms have yet to explore the other levers—operations and IT improvement, technical excellence, commercial uplift, and franchise growth—at scale. Across all these levers, advanced analytics can enable innovative, value-creating approaches.

Author(s): Ramnath Balasubramanian, Alex D’Amico, Rajiv Dattani, and Diego Mattone

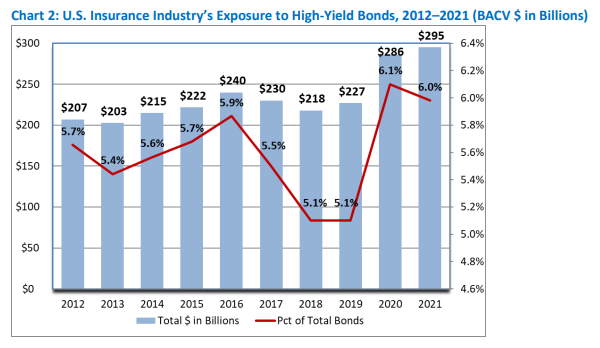

The U.S. insurance industry’s high-yield bond exposure of almost $300 billion at year-end 2021 is the highest BACV reported over the last decade. (See Chart 2.) From 2012 to 2021 , high-yield bond exposure increased approximately 42% while total bond exposure grew approximately 34% as insurance companies sought higher relative yields offered by high-yield bonds, among other asset classes, amid the low interest rate environment of the past decade. In addition, most recently, credit quality deterioration from the impact of the COVID-19 pandemic resulted in some migration of the industry’s investment grade bond exposure into high-yield territory, particularly in 2020.

On a percentage basis, high-yield exposure accounted for 6% of total bonds at year-end 2021, the second highest point over the 10 years ending 2021. While exposure declined modestly from 6.1% at year-end 2020, as a percentage of total bonds, it remains elevated relative to the last 10 years. The most recent period when U.S. insurers’ high-yield-bond exposure exceeded 6% of total bonds was in 2009 during the financial crisis when it reached 6.3%

Author(s): Michele Wong

Publication Date: 13 Oct 2022

Publication Site: NAIC Capital Markets Special Report

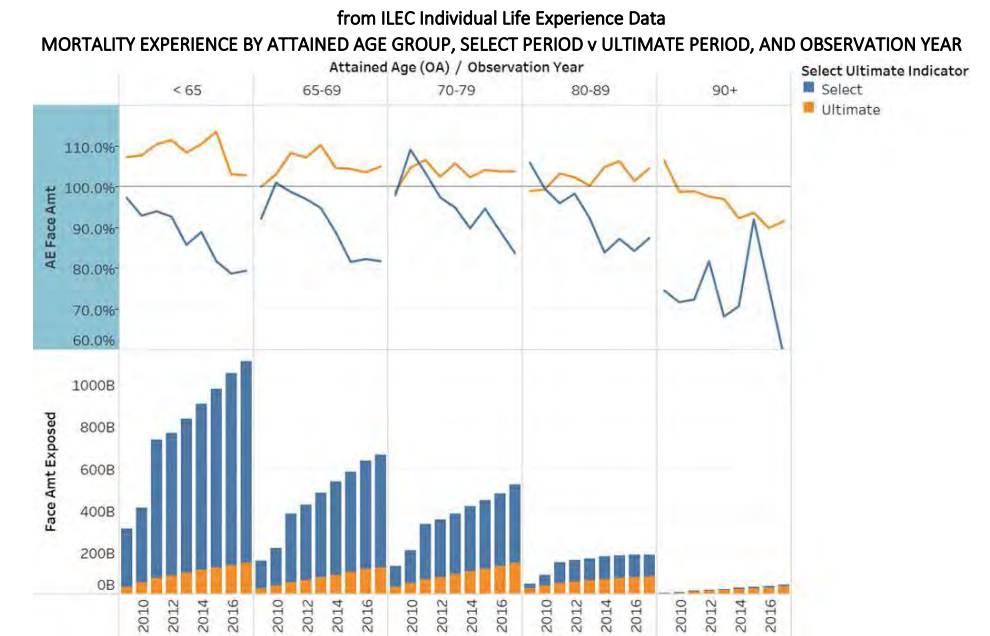

The Society of Actuaries (SOA) Research Institute released a report that examines older age mortality (OAM) with a focus on attained ages 70 and above. The report helps determine whether refinements were needed in the 2015 Valuation Basic Tables. Analysis was performed by sex, issue age and attained age, issue year cohorts, smoking risk classification, benefit band, select vs ultimate period, and interactions.

Author(s):

Old Age Mortality Subgroup of the Individual Life Experience Committee

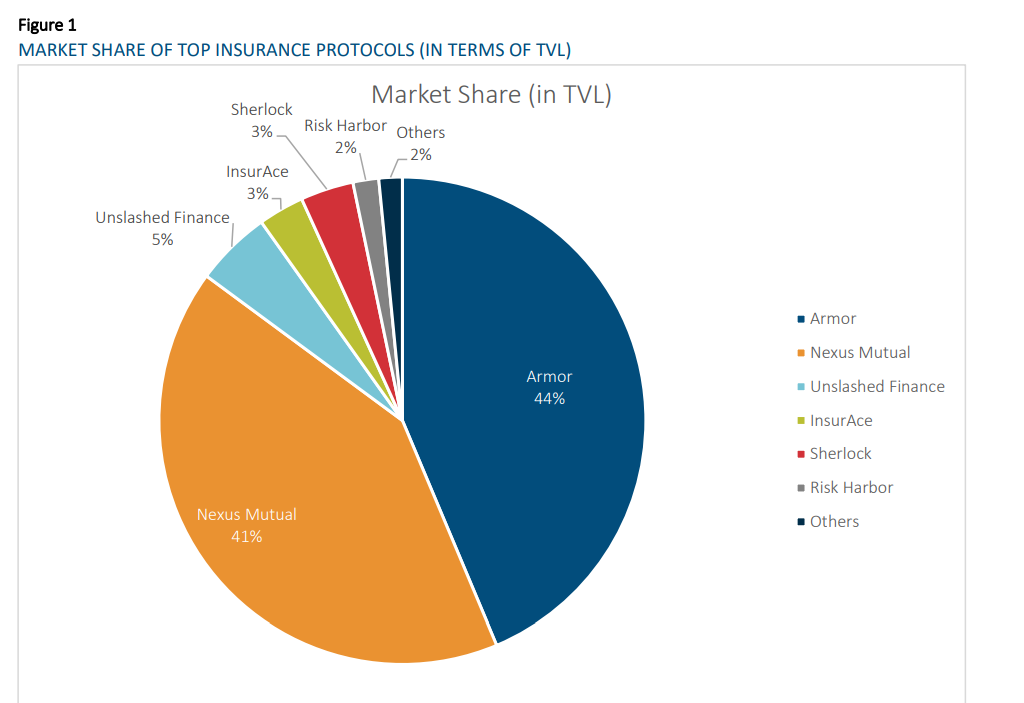

The DeFi ecosystem has been expanding rapidly in the past few years, growing from less than USD $1 billion in 2020 to USD $61.6 billion as of June 2022 as measured by Total Value Locked (TVL), the amount of crypto asset deposited in the DeFi protocols.

With continuous innovation in product design and delivery, the potential of DeFi adoption is massive. However, the rise of DeFi is marred by security issues. Nearly 200 blockchain hacking incidents have taken place in 2021 with approximately USD $7 billion in stolen funds (Cointelegraph, 2021). These hacking events have a wide range of causes including, but not limited to, the following:

Smart contract vulnerabilities exploited by hackers to steal funds

Manipulation of oracles to cause price feed deviation

Attack on governance where a small group of individuals took over the protocol’s governance decisionmaking mechanism

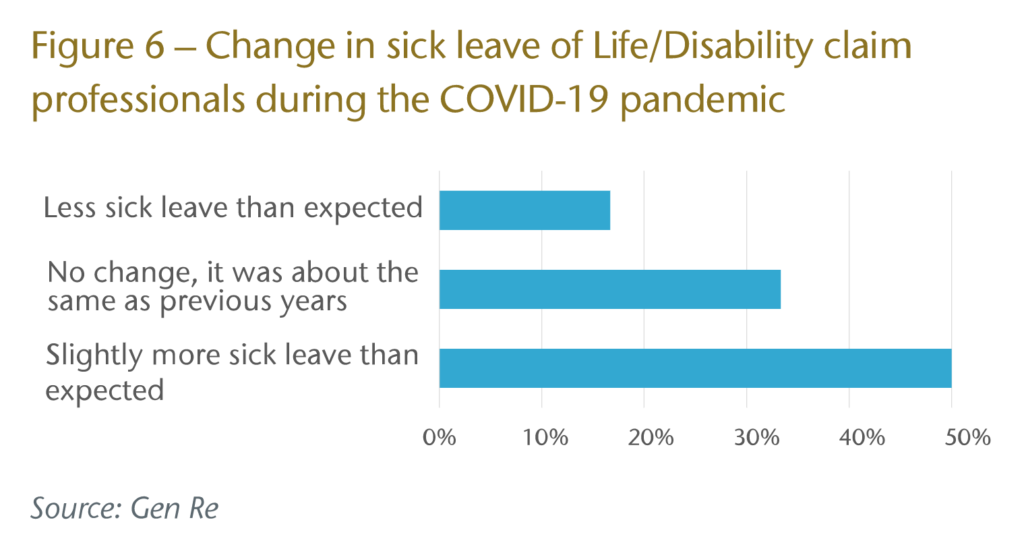

The main concern of managers was that their assessors were, like the rest of the population, limited in terms of what they could do to unwind or use to escape due to lockdown restrictions and limited freedom. This contrasted with usual routines.

We asked about the impact of these concerns on the health of claims professionals. Absenteeism within claims teams varied across the companies and while sick leave increased slightly there did not appear to be any significant or concerning trends (Figure 6).

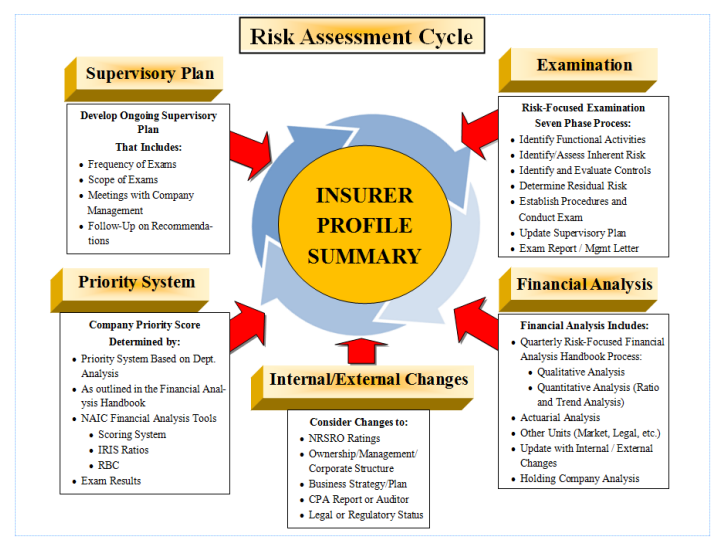

The risk-focused surveillance framework is designed to provide continuous regulatory oversight. The risk-focused approach requires fully coordinated efforts between the financial examination function and the financial analysis function. There should be a continuous exchange of information between the field examination function and the financial analysis function to ensure that all members of the state insurance department are properly informed of solvency issues related to the state’s domestic insurers.

The regulatory Risk-Focused Surveillance Cycle involves five functions, most of which are performed under the current financial solvency oversight role. The enhancements coordinate all of these functions in a more integrated manner that should be consistently applied by state insurance regulators. The five functions of the risk assessment process are illustrated within the Risk-Focused Surveillance Cycle.

As illustrated in the Risk-Focused Surveillance Cycle diagram, elements from the five identified functions contribute to the development of an IPS. Each state will maintain an IPS for its domestic companies. State insurance regulators that wish to review an IPS for a non-domestic company will be able to request the IPS from the domestic or lead state. The documentation contained in the IPS is considered proprietary, confidential information that is not intended to be distributed to individuals other than state insurance regulators.

Please note that once the Risk-Focused Surveillance Cycle has begun, any of the inputs to the IPS can be changed at any time to reflect the changing environment of an insurer’s operation and financial condition.

On September 8, 2022, the U.S. Senate Committee on Banking, Housing and Urban Affairs (“Senate Banking Committee”) held a hearing to consider “Current Issues in Insurance.” One of the items discussed at the hearing was Senator Sherrod Brown’s (D-OH) March 2022 letter to the National Association of Insurance Commissioners (the “NAIC”) and U.S. Department of the Treasury’s Federal Insurance Office (“FIO”) regarding private equity-controlled insurers.1

In his letter, Senator Brown requested that FIO, in consultation with the NAIC, prepare a report for Congress that evaluates the investment strategies pursued by private equity-controlled insurers, the impact on protections for pension plan beneficiaries following pension risk transfer arrangements, and whether state regulatory regimes are capable of assessing and managing risks related to private equity-controlled insurers. In the early summer, the NAIC and the U.S. Department of the Treasury (on behalf of FIO) each provided substantive responses to Senator Brown.2

Author(s): Kara Baysinger | Leah Campbell | Jane Callanan | Matthew J. Gaul Donald B. Henderson, Jr. | David G. Nadig | Allison J. Tam

An active year for mergers and acquisitions in 2021 and large block reinsurance transactions led to a 41% increase in admitted assets owned by private equity firms in 2021, according to a new AM Best special report.

In its Best’s Special Report, “Private Equity Continues to Make Inroads in Insurance Industry,” AM Best states that as life/annuity insurers’ earnings have been pressured, with capital that has been strained due to reserve adjustments, insurers’ willingness to divest businesses has been bolstered; private equity firms have been eager to step in. With the year-over-year increase in admitted assets to $849.6 billion, private equity insurers now have a 10% share of the U.S. life/annuity’s total assets, more than double the share from five years ago.

“More-experienced private equity firms have gotten comfortable managing insurance assets while adhering to constraints imposed on their portfolios, such as regulatory compliance and rating agency capital charges on asset and liability risks, ALM matching requirements and liquidity concerns,” said Jason Hopper, associate director, industry research and analytics. “As these firms take advantage of the more-permanent capital and premium flows afforded them through ownership of an insurer, there is less of a need to look for a quick exit from their investment.”

The report notes that private equity firms have entered the insurance market in one of two ways: by controlling an insurer through an equity investment and buying or reinsuring blocks of business from other insurers, while influencing the insurer’s investment management strategies to earn higher yields; or by working with insurers as a partnership or outsourced chief-investment officer, whereby the private equity firm manages a portion of the insurer’s assets for a fee.

Even with their more diversified bond portfolios, less than a third of private equity insurers have exposures to below-investment-grade bonds greater than the industry average of 5.9%, according to the report. The investing strategies of private equity insurers have helped them consistently generate a higher net yield since 2017, and most continued to outperform the individual annuity writers’ composite in 2021. The competitive pricing private equity insurers can offer puts more pressure on traditional insurers that lack the same scale with more-conservative crediting rates.

The more fundamental changes affect the measurement of future services (previously termed as “Reserves”). Many insurance accounting regimes have tried to stabilize their financial statements over the years; therefore, they calculated their reserves based on historic information—locked-in assumptions for insurance parameters as well as historic interest rates. The latter, however, are not in line with the use of market values for the asset side of the balance sheet, which is now perceived as the only fair-value representation for the different stakeholders. Therefore, the measurement of the liabilities in IFRS 17 will always be based on current assumptions.

Due to the compound effect over many projected years, the regular update of assumptions (particularly interest rate or discounting assumptions) can make long-term liabilities much more volatile.

Insurers are bracing for a hit of between $28 billion and $47 billion from Hurricane Ian, in what could be the costliest Florida storm since Hurricane Andrew in 1992, according to U.S. property data and analytics company CoreLogic.

Wind losses for residential and commercial properties in Florida are expected to be between $22 billion and $32 billion, while insured storm surge losses are expected to be an additional $6 billion to $15 billion, according to CoreLogic.

“This is the costliest Florida storm since Hurricane Andrew made landfall in 1992 and a record number of homes and properties were lost,” said Tom Larsen, associate vice president, hazard & risk management, CoreLogic.

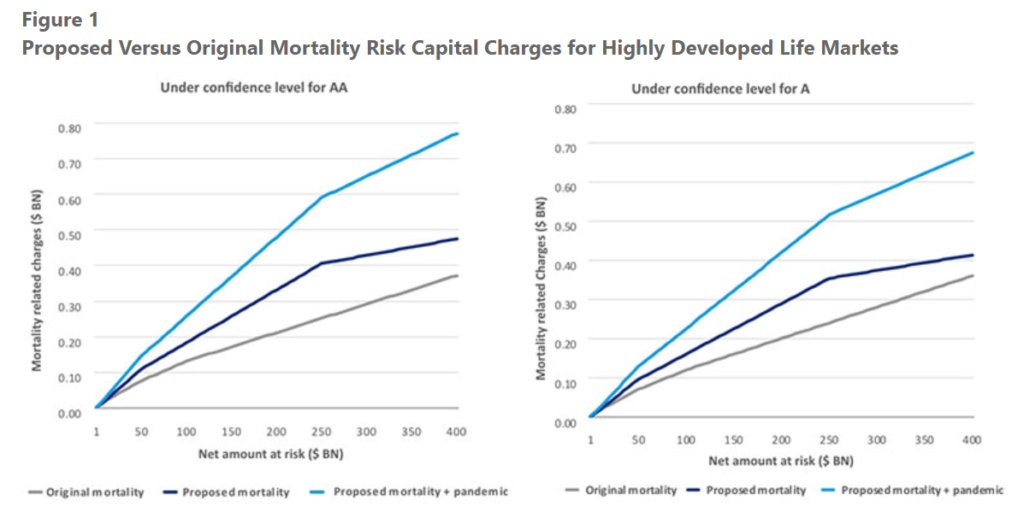

Life technical risks measure the possible losses from deviations from the best estimate assumptions relating to life expectancy, policyholder behavior, and expenses. The life technical risks are captured through mortality, longevity, morbidity, and other risks. The methodology for calculating the capital adequacy for these four risk categories remains unchanged under the proposed method, apart from the recalibration of capital charges or the consolidation of defining categories within each risk. Comparing to the current GAAP based model, charges have materially increased across all categories partly due to higher confidence intervals, with notable exceptions of longevity risk, with reduced charges across all stress levels (changes applicable to U.S. life insurers are illustrated in Tables A2 to A5 in the Appendix linked at the end of this article). Please note that S&P’s current capital model under U.S. statutory basis does not have an explicit longevity risk charge. However, this article focuses on comparison to current GAAP capital model[1] that is closer to the new capital methodology framework.

For mortality risk, lower rates are charged for smaller exposures (net amount at risk (NAR) $5 billion or less) with the consolidation of size categories, but higher rates are charged for NAR between $5 billion and $250 billion, with an average increase of 49 percent for businesses under $400 billion NAR. A new pandemic risk charge (Table A3 in the Appendix linked at the end of this article) will further increase mortality related risk charges to be 109 percent higher than original mortality charges under confidence level for company rating of AA, and 93 percent higher for confidence level for company rating of A, respectively, on average (Figure 1). The disability risk charge rates increased moderately for most products, across all eight product types such that the increase of disability premium risk charges is 6 percent under confidence level for AA, and 2 percent for A, respectively. In addition, the proposed model introduced a new charge on disability claims reserve, ranging from 13.7 percent of total disability claims reserves for AAA, to 9.6 percent for BBB. However, the proposed model provides lower capital charge rates in longevity risk and lapse risk.

Author(s): Yiru (Eve) Sun, John Choi, and Seong-Weon Park

Publication Date: September 2022

Publication Site: Financial Reporting newsletter of the SOA