Graphic:

Excerpt:

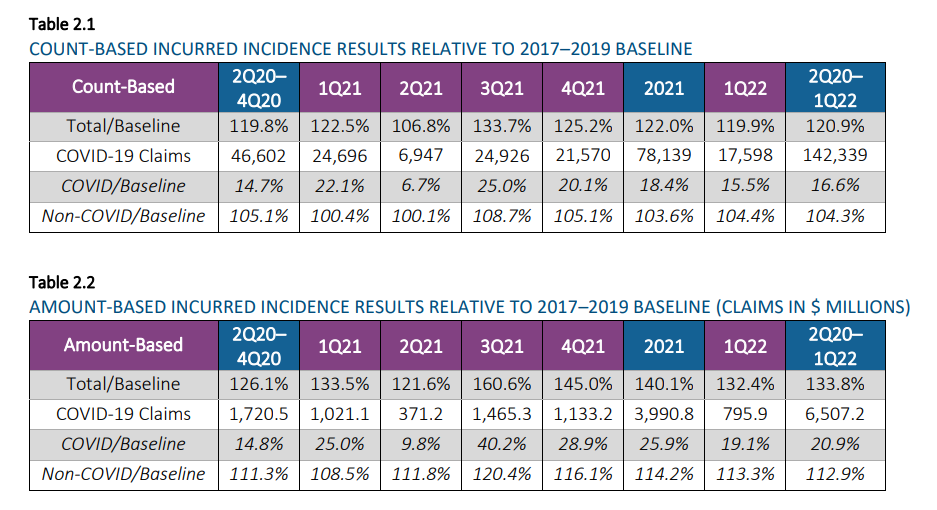

Tables 2.1 through 2.41 display high-level incidence results for the second quarter of 2020 through the first quarter of 2022 compared to the 2017-2019 baseline period for each combination of (a) incurred/reported basis and (b) count/amount basis as of March 31, 2022. In these tables, the number of COVID-19 claims has not been adjusted for seasonality, but the ratios to baseline have been adjusted for seasonality.

….

Note that additional data reported in April and May 2022 indicated that the 1Q 2022 excess mortality would likely complete downward from the 19.9% shown below using March data. The fully complete 1Q 2022 excess mortality is expected to remain above 15%.

The 24-month period of April 2020 through March 2022 showed the following Group Life mortality results:

• Estimated reported Group Life claim incidence rates were up 20.0% on a seasonally-adjusted basis

compared to 2017–2019 reported claims.

• Estimated incurred Group Life incidence rates were 20.9% higher than baseline on a seasonally-adjusted

basis. As noted above, the incurred incidence rates in February and March 2022 are based on fairly

incomplete data, so they are subject to change and should not be fully relied upon at this point.

Author(s):

Thomas J. Britt, FSA, MAAA

Paul Correia, FSA, MAAA

Patrick Hurley, FSA, MAAA

Mike Krohn, FSA, CERA, MAAA

Tony LaSala, FSA, MAAA

Rick Leavitt, ASA, MAAA

Robert Lumia, FSA, MAAA

Cynthia S. MacDonald, FSA, MAAA, SOA

Patrick Nolan, FSA, MAAA, SOA

Steve Rulis, FSA, MAAA

Bram Spector, FSA, MAAA

Publication Date: August 2022

Publication Site: SOA