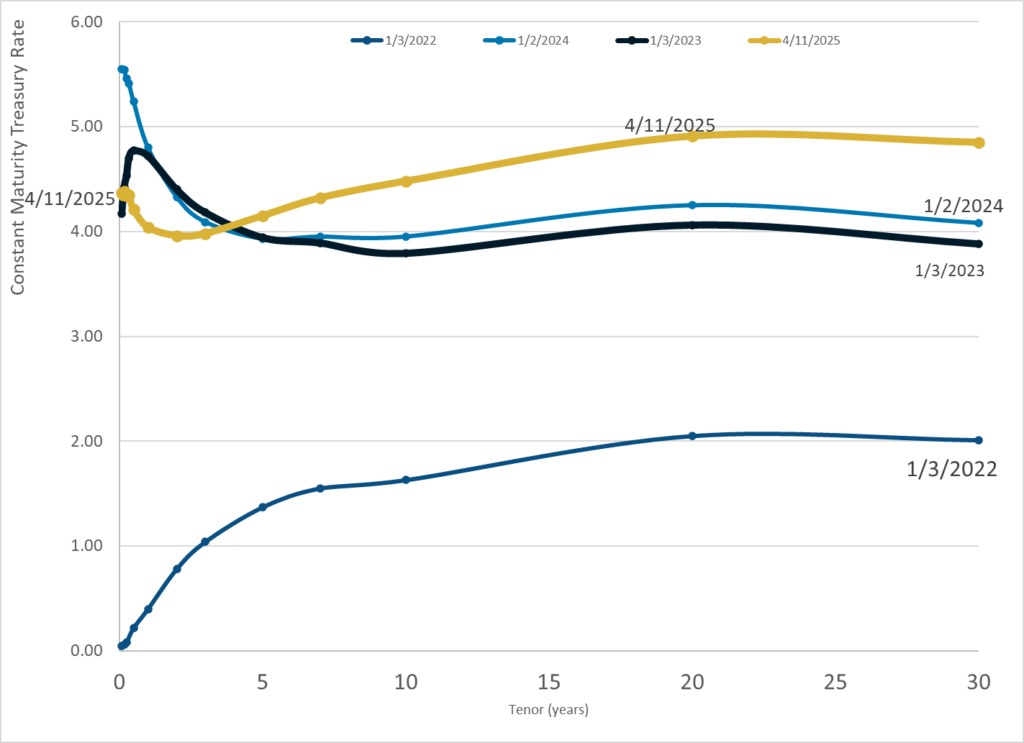

Graphic:

Publication Date: 11 Apr 2025

Publication Site: Treasury Dept

All about risk

Graphic:

Publication Date: 11 Apr 2025

Publication Site: Treasury Dept

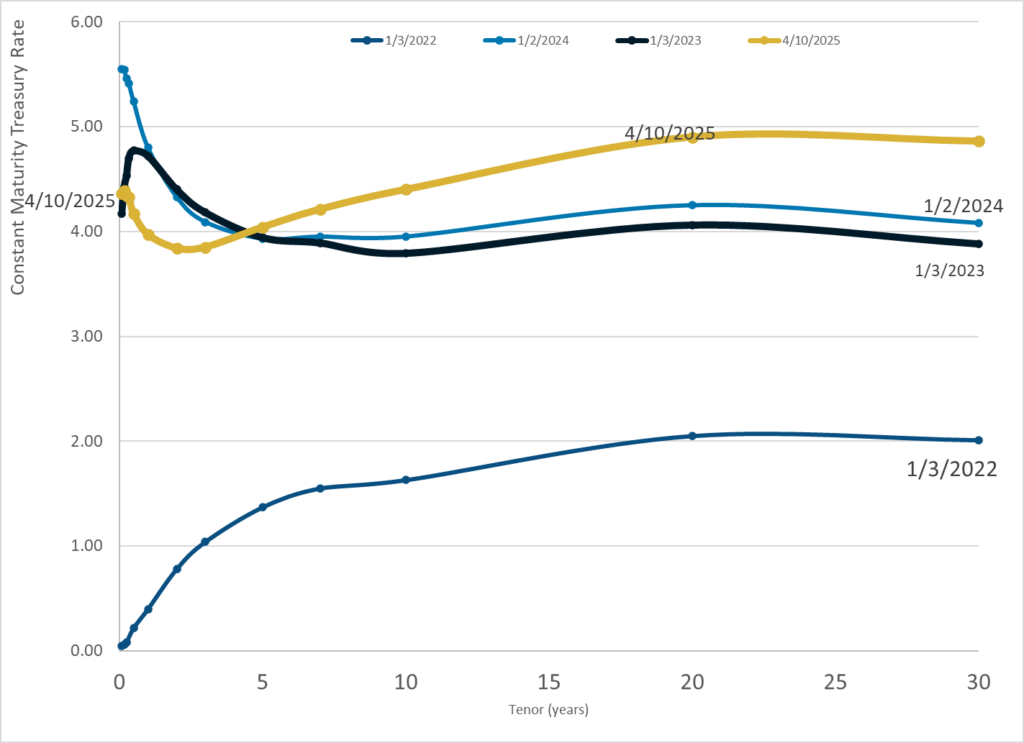

Graphic:

Publication Date: 10 Apr 2025

Publication Site: Treasury Dept

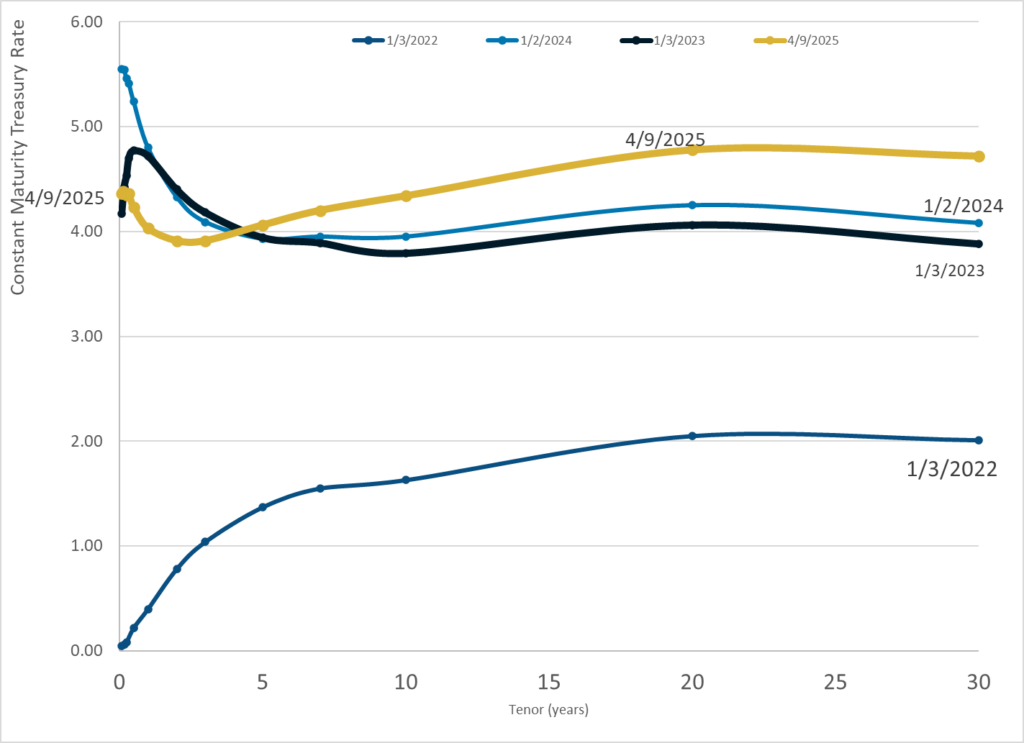

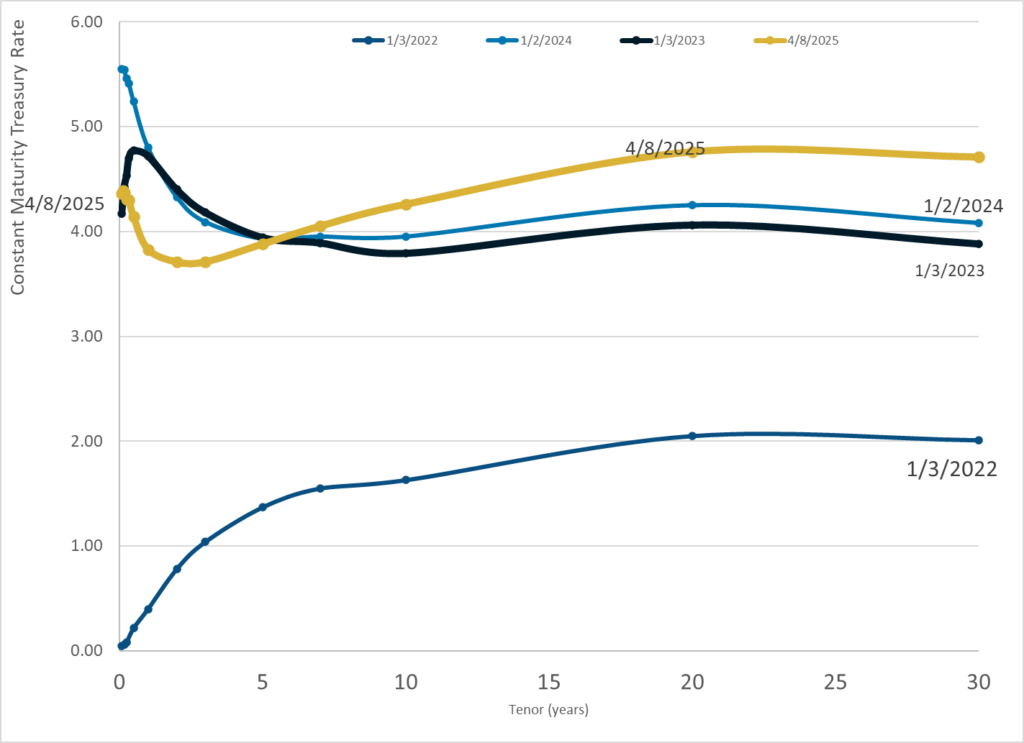

Graphic:

Publication Date: 9 Apr 2025

Publication Site: Treasury Dept

Link: https://ar.casact.org/modeling-the-casualty-exposures-in-epidemics/

Graphic:

Excerpt:

A casualty actuary might be forgiven for thinking that illness and disease are what those “other” actuaries worry about.

Though risk of illness is usually considered the province of the life-health actuary, a session at the 2017 CAS Annual Meeting in Anaheim, California, showed how epidemics can affect property-casualty risks. The session also described how to approach modeling those exposures.

….

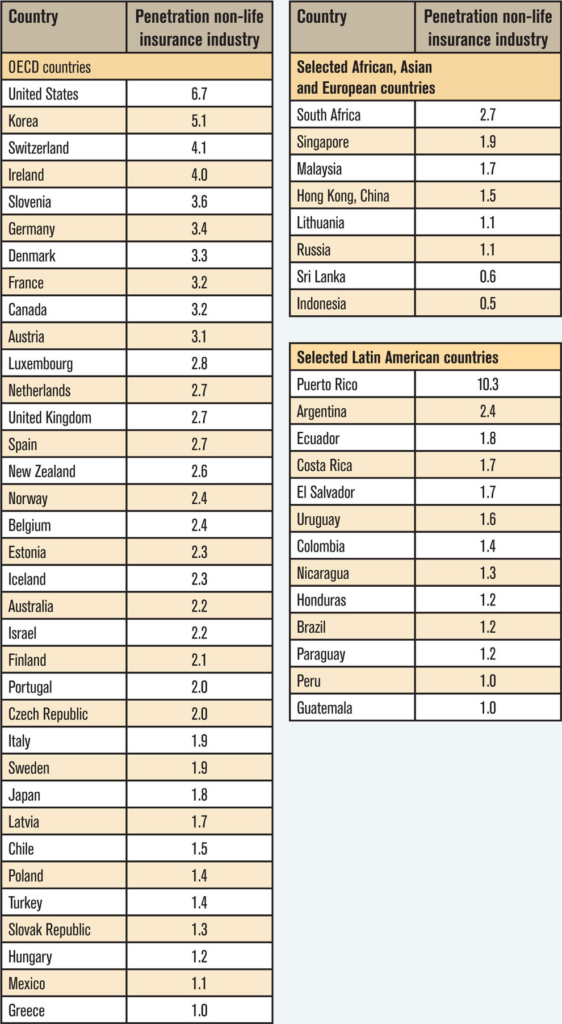

Milliman actuary Cody Webb, FCAS, began by demonstrating how big the insurance gap is, particularly in developing nations. He explained that the spectrum of losses ranges from minuscule (loss of a single strand of hair) to catastrophic (sudden, instant death) and can affect a single person or every entity in the universe across eons. But the insurable losses share some traits, Webb said, including:

In showing a chart of property-casualty insurance as a percentage of GDP — with the wealthier countries better insured than others — Webb noted that insurance companies need to “quantify and develop products that meet all criteria of insurability.” (See chart below.)

Author(s): James P. Lynch

Publication Date: 16 Jan 2018

Publication Site: Actuarial Review, Casualty Actuarial Society

Graphic:

Publication Date: 8 Apr 2025

Publication Site: Treasury Dept

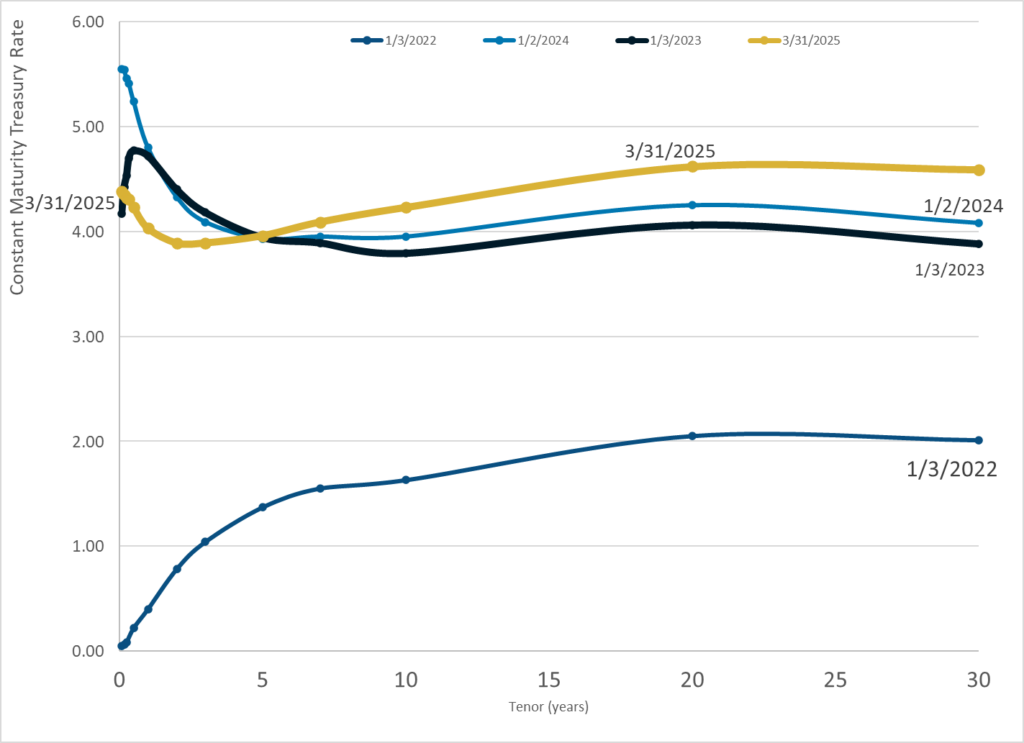

Graphic:

Publication Date: 31 Mar 2025

Publication Site: Treasury Dept

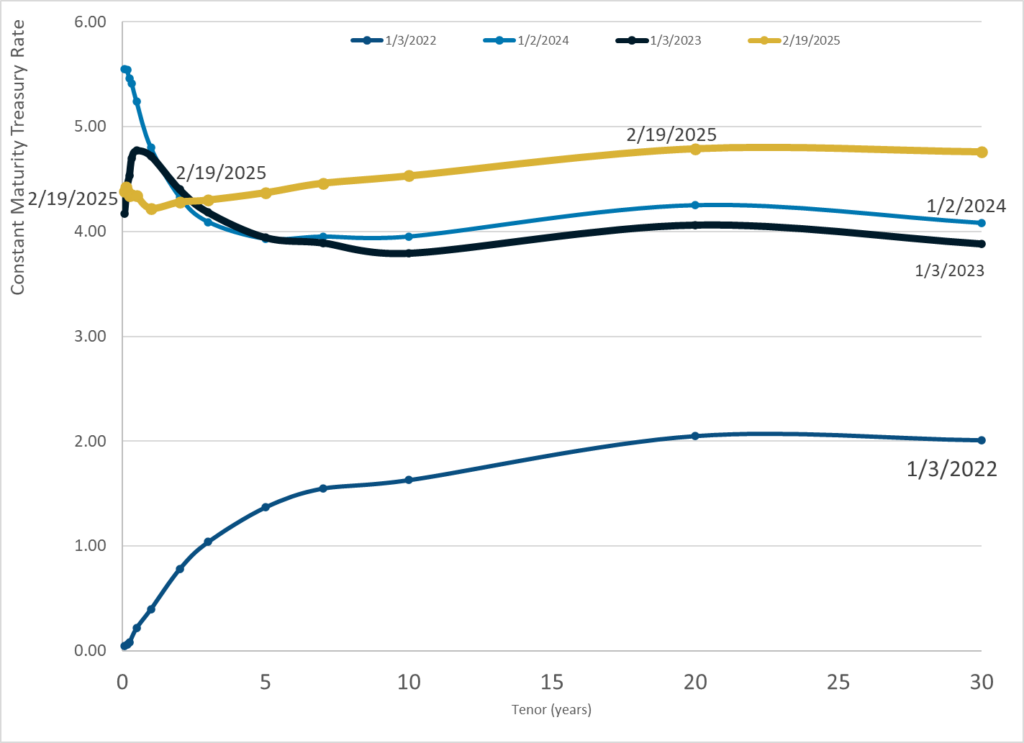

Graphic:

Publication Date: 21 Feb 2025

Publication Site: Treasury Department

Graphic:

Publication Date: 19 Feb 2025

Publication Site: Treasury Department

Graphic:

Excerpt:

Effective with the inaugural auction of the new benchmark 6-week Treasury bill on Tuesday, February 18, 2025, Treasury plans to include 6-week bill prices in its input data set for the daily yield curve. Treasury also plans to add a 1.5-month CMT to the Daily Treasury Par Yield Curve Rates and 6-week bill rates to the Daily Treasury Bill Rates that it publishes.

Changes to the published tables and data files to accommodate the additional rates will appear beginning in the evening on February 14, 2025.

Publication Date: 18 Feb 2025

Publication Site: Treasury Dept

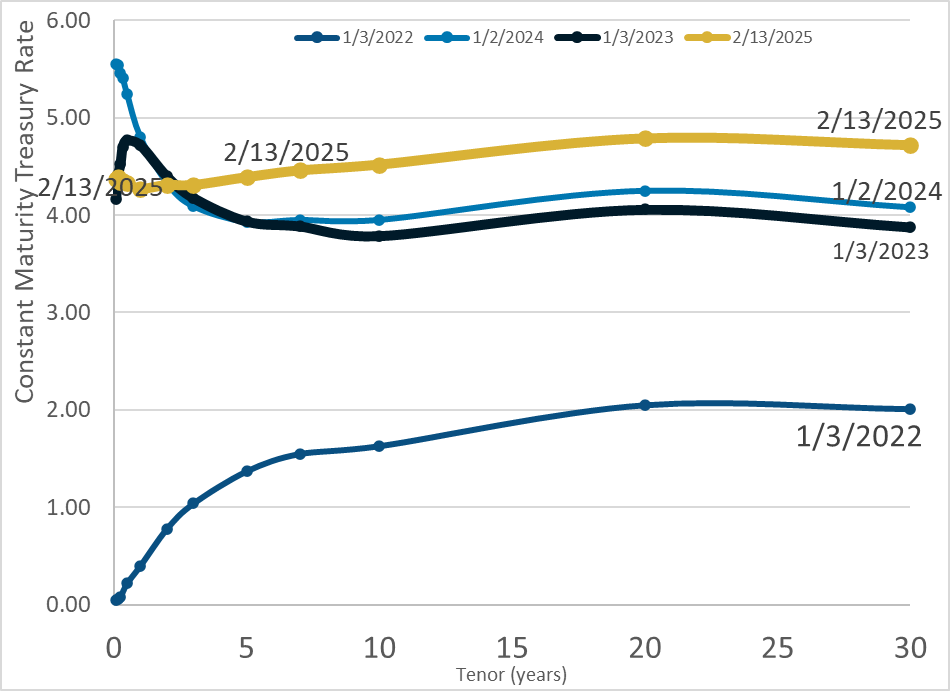

Graphic:

Publication Date: 13 Feb 2025

Publication Site: Treasury Dept

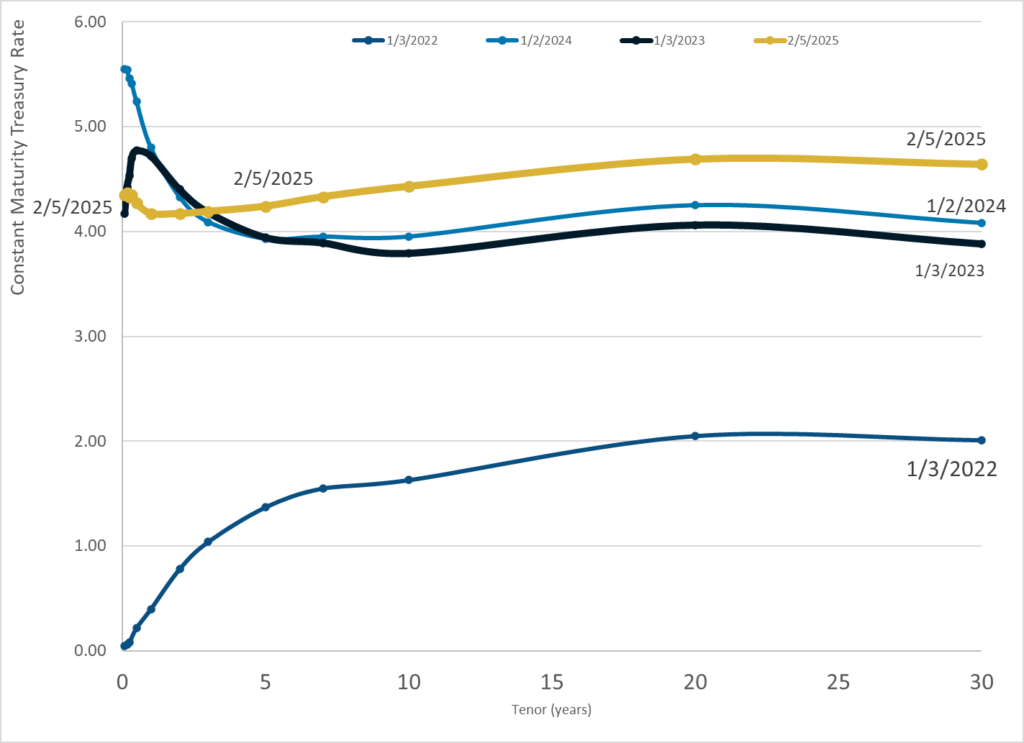

Graphic:

Publication Date: 5 Feb 2025

Publication Site: Treasury Dept

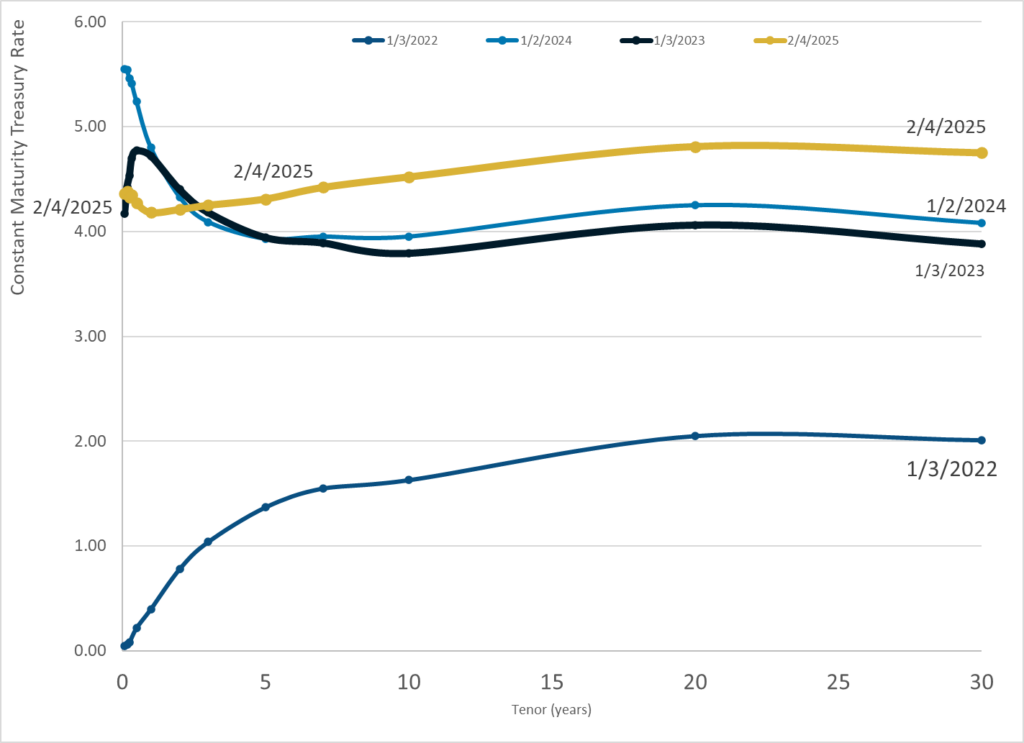

Graphic:

Publication Date: 4 Feb 2025

Publication Site: Treasury Dept