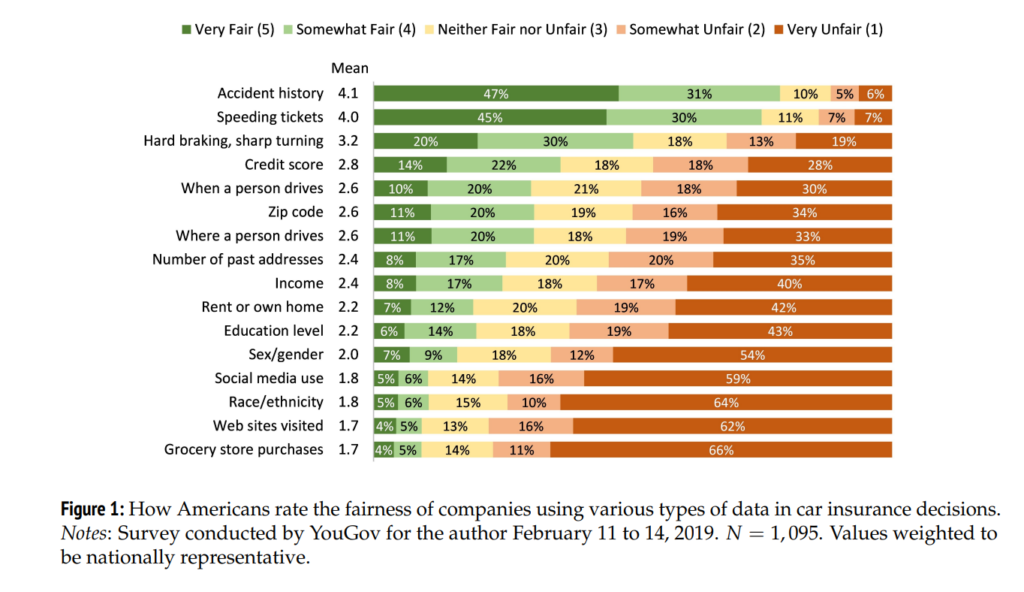

Graphic:

Excerpt:

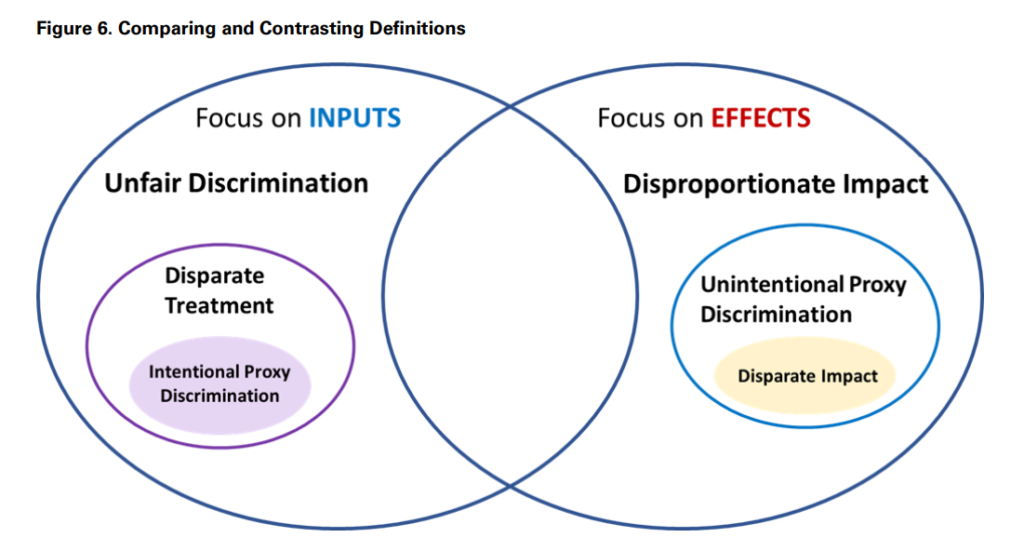

This research paper is designed to introduce various terms used in defining

discrimination by stakeholders in the insurance industry (regulators, consumer

advocacy groups, actuaries and insurers, etc.). The paper defines protected class,

unfair discrimination, proxy discrimination, disproportionate impact, disparate

treatment and disparate impact.

Stakeholders are not always consistent in their definitions of these terms, and

these inconsistencies are highlighted and illustrated in this paper. It is essential to

elucidate key elements and attributes of certain terms as well as conflicting

approaches to defining discrimination in insurance in order to move the industry

discussion forward.

While this paper does not make a judgment on the appropriateness of the

definitions put forth, nor does it promulgate what the definitions should be,

readers will be empowered to understand the components of discrimination terms

used in insurance, as well as be introduced to the potential implications for

insurers.

Actuaries who have a strong foundational knowledge of these terms are likely to

play a key role in informing those who define and refine these terms for insurance

purposes in the future. This paper is not a legal review, and thus discusses terms

and concepts as they are used by insurance stakeholders, rather than what their

ultimate legal definition will be. However, it is important for actuaries to

understand the point of view of various stakeholders, and the potential impact it

could have on actuarial work. As the regulatory and legislative landscape

continues to shift, this brief should be considered a living document, that will

periodically require update.

Author(s): Kudakwashe F. Chibanda, FCAS

Publication Date: March 2022

Publication Site: CAS