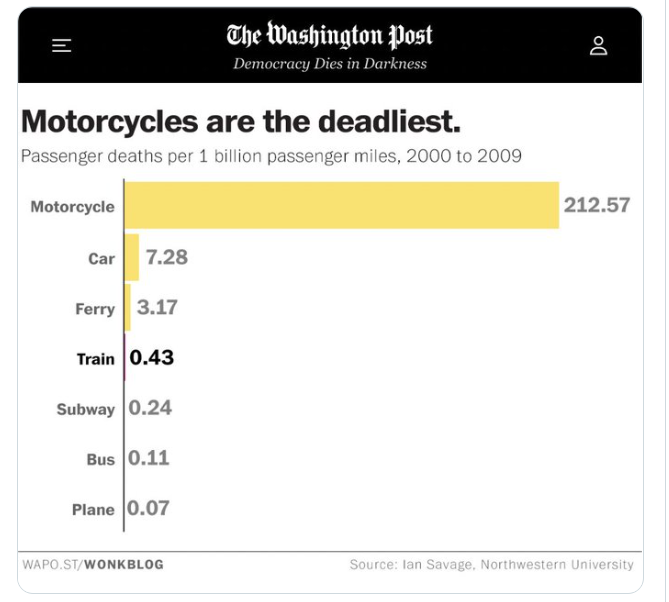

Link: https://twitter.com/AlecStapp/status/1528859020098154496

Graphic:

Publication Date: 23 May 2022

Publication Site: Twitter

All about risk

Link: https://twitter.com/AlecStapp/status/1528859020098154496

Graphic:

Publication Date: 23 May 2022

Publication Site: Twitter

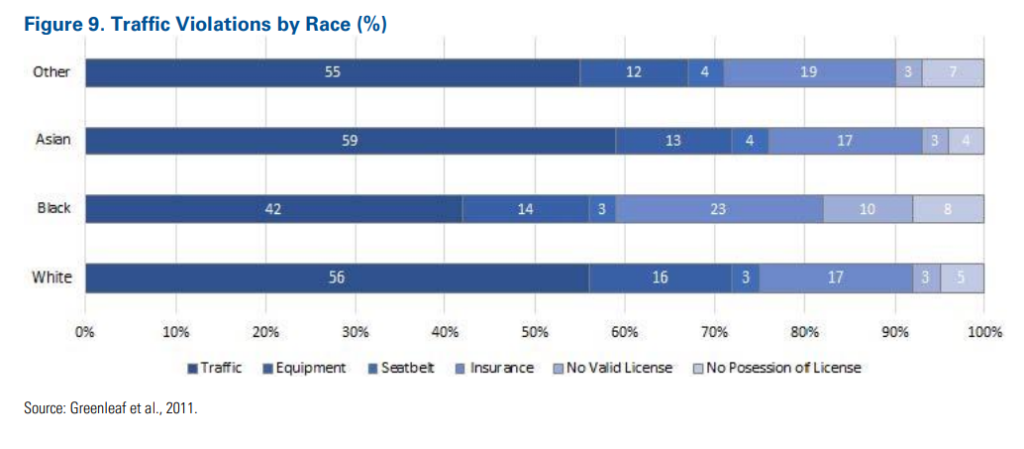

Graphic:

Excerpt:

Insurance rating characteristics have come under scrutiny by legislators and

regulators in their efforts to identify and address racial bias in insurance

practices. The goal of this paper is to equip actuaries with the information

needed to proactively participate in industry discussions and actions related

to racial bias and insurance rating factors. This paper uses the following

definition of racial bias:

Racial bias refers to a system that is inherently skewed along racial lines.

Racial bias can be intentional or unintentional and can be present in the

inputs, design, implementation, interpretation, or outcomes of any system.

This paper will examine four commonly used rating factors in personal

lines insurance — credit-based insurance score, geographic location, home

ownership, and motor vehicle records — to understand how the data

underlying insurance pricing models may be impacted by racially biased

policies and practices outside of the system of insurance. Historical issues

like redlining and racial segregation, as well as inconsistent enforcement of

policies and practices contribute to this potential bias. These historical

issues do not necessarily change the validity of the actuarial approach of

evaluating statistical correlation of rating factors to insurance loss overall.

Differences in the way individual insurers build rating models may produce

very different end results for customers. More data and analyses are

needed to understand if and to what extent these specific issues of racial

bias impact insurance outcomes. Actuaries and other readers can combine

this information with their own subject matter expertise to determine if and

how this could impact the systems for which they are responsible, and what

actions, if any, could be taken as a result.

Author(s): Members of the 2021 CAS Race and Insurance Research Task Force

Publication Date: March 2022

Publication Site: CAS

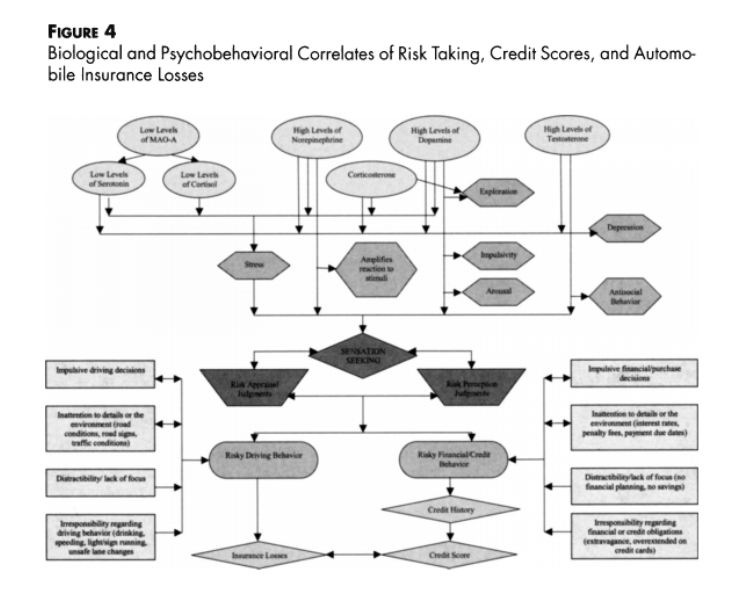

Link: https://www.jstor.org/stable/4138424

Graphic:

Abstract:

The most important new development in the past two decades in the personal lines of insurance may well be the use of an individual’s credit history as a classification and rating variable to predict losses. However, in spite of its obvious success as an underwriting tool, and the clear actuarial substantiation of a strong association between credit score and insured losses over multiple methods and multiple studies, the use of credit scoring is under attack because there is not an understanding of why there is an association. Through a detailed literature review concerning the biological, psychological, and behavioral attributes of risky automobile drivers and insured losses, and a similar review of the biological, psychological, and behavioral attributes of financial risk takers, we delineate that basic chemical and psychobehavioral characteristics (e.g., a sensation-seeking personality type) are common to individuals exhibiting both higher insured automobile loss costs and poorer credit scores, and thus provide a connection which can be used to understand why credit scoring works. Credit scoring can give information distinct from standard actuarial variables concerning an individual’s biopsychological makeup, which then yields useful underwriting information about how they will react in creating risk of insured automobile losses.

Author(s): Patrick L. Brockett and Linda L. Golden

Publication Date: originally 2007

Publication Site: jstor, The Journal of Risk and Insurance

Cite: Brockett, Patrick L., and Linda L. Golden. “Biological and Psychobehavioral Correlates of Credit Scores and Automobile Insurance Losses: Toward an Explication of Why Credit Scoring Works.” The Journal of Risk and Insurance, vol. 74, no. 1, 2007, pp. 23–63. JSTOR, http://www.jstor.org/stable/4138424. Accessed 22 May 2022.

Graphic:

Excerpt:

This research paper’s main objective is to inspire and generate discussions

about algorithmic bias across all areas of insurance and to encourage

actuaries to be involved. Evaluating financial risk involves the creation of

functions that consider myriad characteristics of the insured. Companies utilize

diverse statistical methods and techniques, from relatively simple regression

to complex and opaque machine learning algorithms. It has been alleged that

the predictions produced by these mathematical algorithms have

discriminatory effects against certain groups of society, known as protected

classes.

The notion of discriminatory effects describes the disproportionately adverse

effect algorithms and models could have on protected groups in society. As a

result of the potential for discriminatory effects, the analytical processes

followed by financial institutions for decision making have come under greater

scrutiny by legislators, regulators, and consumer advocates. Interested parties

want to know how to quantify such effects and potentially how to repair such

systems if discriminatory effects have been detected.

This paper provides:

• A historical perspective of unfair discrimination in society and its impact

on property and casualty insurance.

• Specific examples of allegations of bias in insurance and how the various

stakeholders, including regulators, legislators, consumer groups and

insurance companies have reacted and responded to these allegations.

• Some specific definitions of unfair discrimination and that are interpreted

in the context of insurance predictive models.

• A high-level description of some of the more common statistical metrics

for bias detection that have been recently developed by the machine

learning community, as well as a brief account of some machine learning

algorithms that can help with mitigating bias in models.

This paper also presents a concrete example of an insurance pricing GLM

model developed on anonymized French private passenger automobile data,

which demonstrates how discriminatory effects can be measured and

mitigated.

Author(s): Roosevelt Mosley, FCAS, and Radost Wenman, FCAS

Publication Date: March 2022

Publication Site: CAS

Link: https://fee.org/articles/are-seat-belts-making-you-less-safe/

Excerpt:

In the 1960s, the federal government—in its infinite wisdom—thought that cars were too unsafe for the general public. In response, it passed automobile safety legislation, requiring that seat belts, padded dashboards, and other safety measures be put in every automobile.

Although well-intended, auto accidents actually increased after the legislation was passed and enforced. Why? As Lansburg explains, “the threat of being killed in an accident is a powerful incentive to drive carefully.”

In other words, the high price (certain death from an accident) of an activity (reckless driving) reduced the likelihood of that activity. The safety features reduced the price of reckless driving by making cars safer. For example, seatbelts reduced the likelihood of a driver being hurt if he drove recklessly and got into an accident. Because of this, drivers were more likely to drive recklessly.

The benefit of the policy was that it reduced the number of deaths per accident. The cost of the policy was that it increased the number of accidents, thus canceling the benefit. Or at least, that is the conclusion of University of Chicago’s Sam Peltzman, who found the two effects canceled each other.

His work has led to a theory called “The Peltzman Effect,” also known as risk compensation. Risk compensation says that safety requirements incentivize people to increase risky behavior in response to the lower price of that behavior.

Author(s): Joshua Anumolu

Publication Date: 13 July 2017

Publication Site: FEE

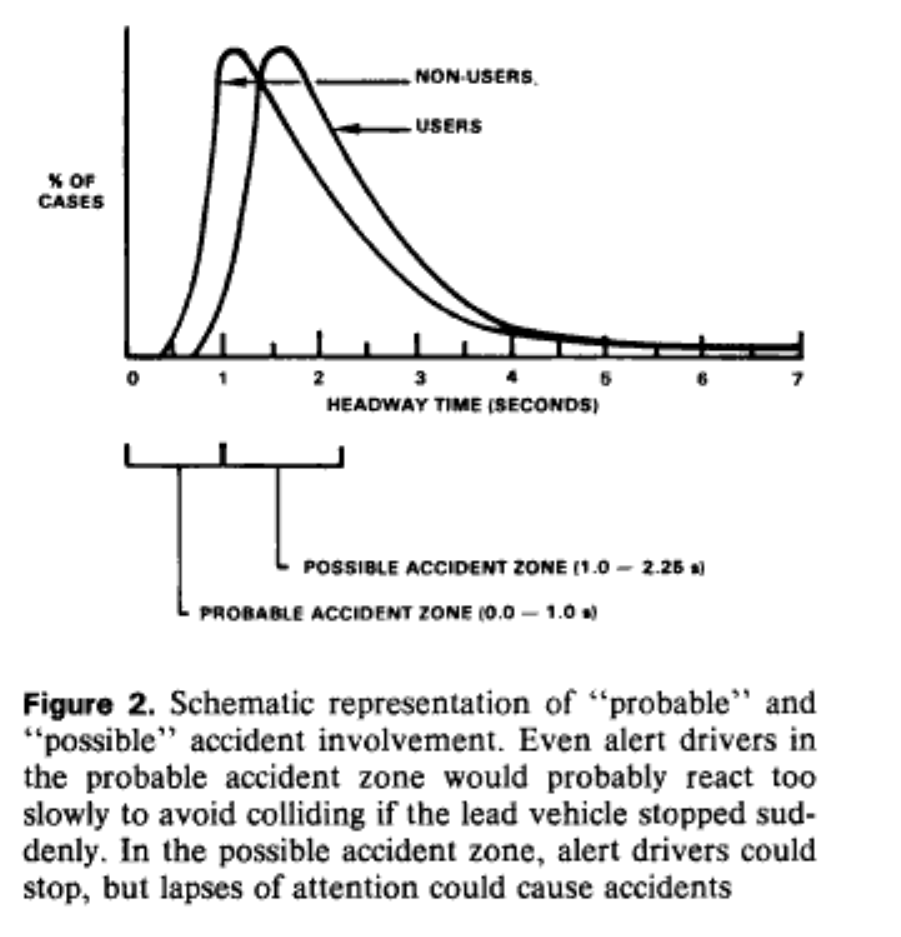

Link: https://www.jstor.org/stable/44633774

Graphic:

Abstract:

This study tested the hypothesis that seat belt usage is related to driver risk taking in car-following behavior. Individual vehicles on a Detroit area freeway were monitored to identify seat belt users and nonusers. Headways between successive vehicles in the traffic stream were also measured to provide a behavioral indicator of driver risk taking. Results showed that nonusers of seat belts tended to follow other vehicles closer than did users. Users were also less likely than nonusers to follow other vehicles at very short headways (one second or less). The implications of these findings for occupant safety in rear end collisions are discussed.

Author(s): Buseck, Calvin R. von, Leonard Evans, Donald E. Schmidt, and Paul Wasielewski

Publication Date: 1980

Publication Site: jstor, originally published in SAE Transactions, vol 89

Cite:

von Buseck, Calvin R., et al. “Seat Belt Usage and Risk Taking in Driving Behavior.” SAE Transactions, vol. 89, 1980, pp. 1529–33. JSTOR, http://www.jstor.org/stable/44633774. Accessed 21 May 2022.

Link: https://ctmirror.org/2022/04/18/why-driving-needs-to-feel-less-safe/

Excerpt:

Motor vehicle fatalities in Connecticut have risen dramatically since the pandemic, echoing a trend that we’ve seen across the country. About 300 people are killed annually on Connecticut’s streets by motor vehicles, and about 100 times as many people (roughly 30,000) suffer injuries severe ePnough to warrant hospital admission.

Nationally, these figures are roughly 40,000 deaths and 3.4 million injuries per year. The U.S. is an outlier among developed countries in the number of deaths that we tolerate on our roads, with a death rate 2 to 3 times that of similarly wealthy countries. The human cost of this carnage leaves no one untouched: almost everyone knows at least one person killed by a vehicle, not to mention millions of others who suffer from life-altering consequences like paralysis and traumatic brain injuries.

If we truly care about saving lives and preventing injuries, we need to change the mindset by which we view the act of driving.

Author(s): Dice Oh

Publication Date: 18 April 2022

Publication Site: CT Mirror

Link: https://www.rstreet.org/2022/04/05/event-risk-based-rating-in-personal-lines-insurance/

Screenshot:

Video:

Excerpt:

The insurance industry is unique in that the cost of its products—insurance policies—is unknown at the time of sale. Insurers calculate the price of their policies with “risk-based rating,” wherein risk factors known to be correlated with the probability of future loss are incorporated into premium calculations. One of these risk factors employed in the rating process for personal automobile and homeowner’s insurance is a credit-based insurance score.

Credit-based insurance scores draw on some elements of the insurance buyer’s credit history. Actuaries have found this score to be strongly correlated with the potential for an insurance claim. The use of credit-based insurance scores by insurers has generated controversy, as some consumer organizations claim incorporating such scores into rating models is inherently discriminatory. R Street’s webinar explores the facts and the history of this issue with two of the most knowledgeable experts on the topic.

Author(s): Jerry Theodorou, Roosevelt Mosley, Mory Katz

Publication Date: 5 April 2022

Publication Site: R Street Institute

Link: https://www.youtube.com/watch?v=IPYSSZkP-Oo&ab_channel=RStreetInstitute

Video:

Description:

The insurance industry is unique in that the cost of its products—insurance policies—is unknown at the time of sale. Insurers calculate the price of their policies with “risk-based rating,” wherein risk factors known to be correlated with the probability of future loss are incorporated into premium calculations. One of these risk factors employed in the rating process for personal automobile and homeowner’s insurance is a credit-based insurance score.

Credit-based insurance scores draw on some elements of the insurance buyer’s credit history. Actuaries have found this score to be strongly correlated with the potential for an insurance claim. The use of credit-based insurance scores by insurers has generated controversy, as some consumer organizations claim incorporating such scores into rating models is inherently discriminatory. R Street’s webinar explores the facts and the history of this issue with two of the most knowledgeable experts on the topic.

Featuring:

[Moderator] Jerry Theodorou, Director, Finance, Insurance & Trade Program, R Street Institute

Roosevelt Mosley, Principal and Consulting Actuary, Pinnacle Actuarial Services

Mory Katz, Legacy Practice Leader, BMS GroupR Street Institute is a nonprofit, nonpartisan, public policy research organization. Our mission is to engage in policy research and outreach to promote free markets and limited, effective government.

We believe free markets work better than the alternatives. We also recognize that the legislative process calls for practical responses to current problems. To that end, our motto is “Free markets. Real solutions.”

We offer research and analysis that advance the goals of a more market-oriented society and an effective, efficient government, with the full realization that progress on the ground tends to be made one inch at a time. In other words, we look for free-market victories on the margin.

Learn more at https://www.rstreet.org/

Follow us on Twitter at @RSI

Author(s): Jerry Theodorou, Roosevelt Mosley, Mory Katz

Publication Date: 4 April 2022

Publication Site: R Street at YouTube

Excerpt:

Tesla is looking to expand its auto insurance offering into two more states: Oregon and Virginia.

The electric vehicle manufacturer currently offers insurance products in Arizona, California, Illinois, Ohio, and Texas – where Tesla first launched its pilot insurance program which tracks policyholders’ driving behavior to set rates.

The “safety scores” generated by Tesla’s onboard telematics systems in its vehicles are available for drivers to view and use in insurance rate setting in Arizona, Illinois, Ohio and Texas – California regulations have not yet permitted the use of telematics data in insurance. Tesla claims that drivers with high safety scores can save 20% to 60% on their insurance costs.

Author(s): Lyle Adriano

Publication Date: 14 Mar 2022

Publication Site: Insurance Business America

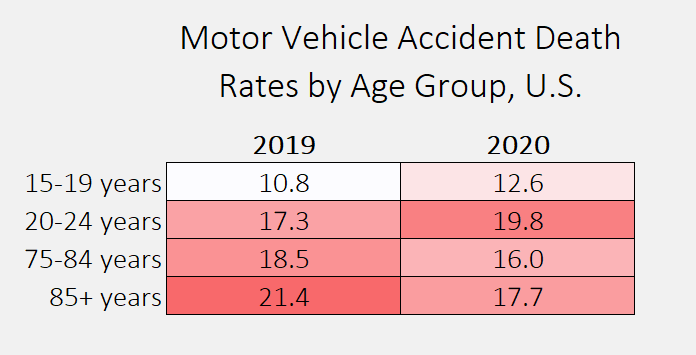

Link: https://marypatcampbell.substack.com/p/motor-vehicle-accident-deaths-part?s=w

Graphic:

Excerpt:

The rates are per 100,000 people for the year, but the point is who has the highest, and we see that the answer is:

For 2019: age 85+

For 2020: age 20-24

I threw in the age 15-19 group as ringers, by the way. When we get to all the age groups, they’re not even #4 in the ranking.

Just in that little table, you can see that the rates went up for the youngsters and dropped for the seniors. Think about why that might be.

As noted in my polling question, I’m not adjusting for the number of miles driven, and I’m not going to dig for that data now. But would you like to make some assumptions about the driving habits of these different groups? Especially during the pandemic?

Author(s): Mary Pat Campbell

Publication Date: 2 March 2022

Publication Site: STUMP at substack

Link: https://www.dig-in.com/news/allstate-and-john-hancock-partner-safe-driving-telematics

Excerpt:

John Hancock and Allstate have announced a partnership to reward John Hancock Vitality members with points for safe driving. The partnership is the first of its kind, and comes in response to an increase in vehicle crash-related injuries. Customers will benefit from understanding how their choices, including driving behavior, impact their overall health, John Hancock believes.

….

The Vitality Program, which combines life insurance with education, incentives and rewards to help members lead healthier, longer lives, will allow members to submit proof of safe driving status in Allstate’s usage-based insurance program through a cashback reward email or by submitting a recent bill to show a safe-driving discount.

Motor vehicle deaths in the U.S. rose 18.4% in the first six months of 2021 over 2020, according to data from the U.S. Department of Transportation’s National Highway Traffic Safety Administration. An estimated 20,160 people died in motor vehicle crashes in the first half of 2021, the largest number of projected fatalities since the same period in 2006. Research into driving behavior from March 2020 through June 2021, shows that speeding and traveling without a seatbelt remain higher than pre-pandemic times, according to findings from NHTSA.

Author(s): Kaitlyn Mattson

Publication Date: 24 January 2022

Publication Site: Digital Insurance