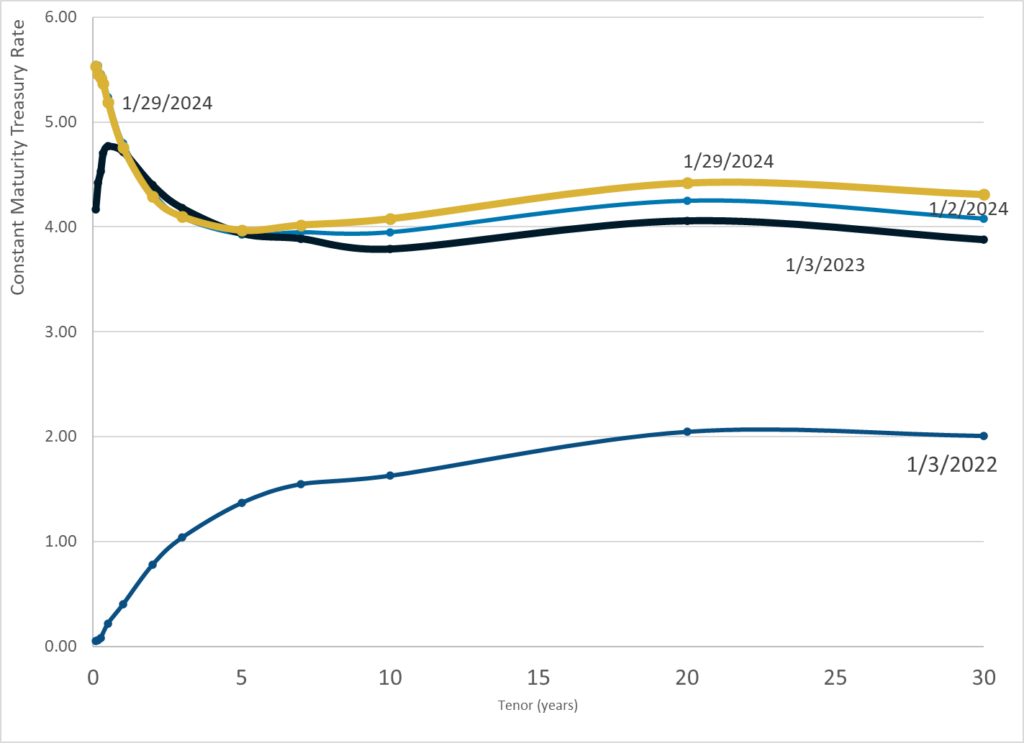

Graphic:

Publication Date: 29 Jan 2024

Publication Site: Treasury Dept

All about risk

Graphic:

Publication Date: 29 Jan 2024

Publication Site: Treasury Dept

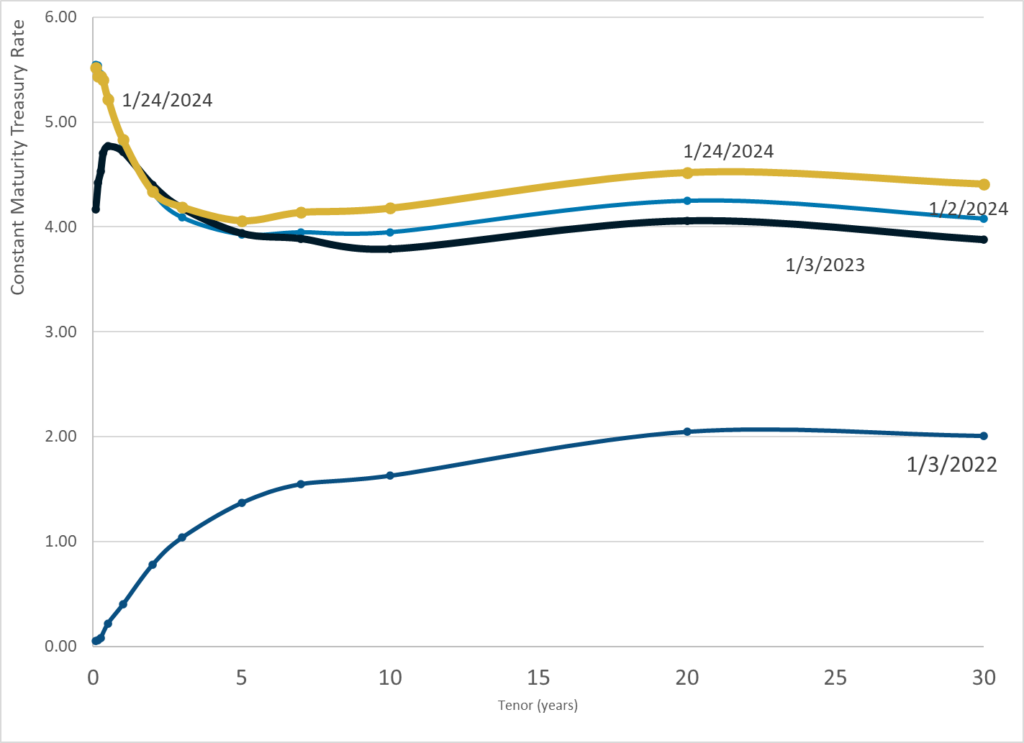

Graphic:

Publication Date: 24 Jan 2024

Publication Site: Treasury Dept

Link: https://www.cato.org/regulation/winter-2023-2024/will-actuaries-come-clean-public-pensions

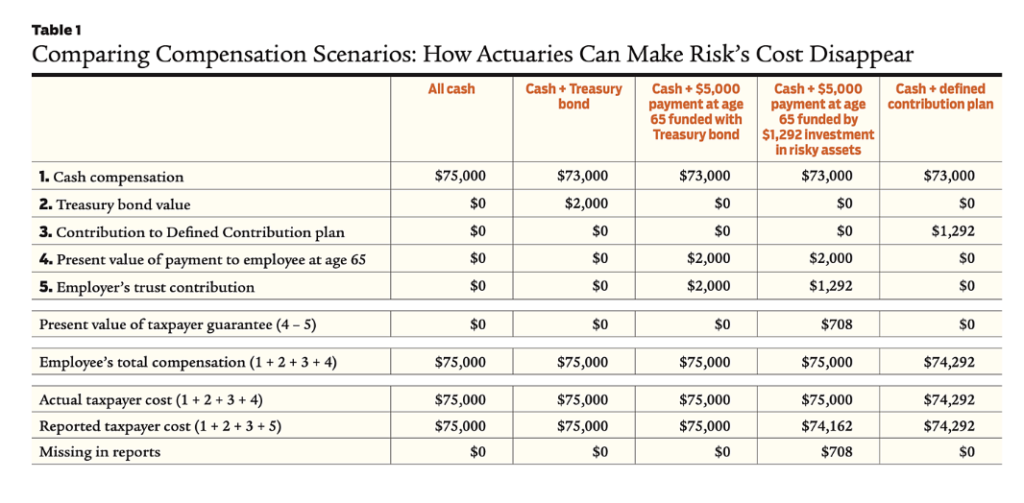

Graphic:

Excerpt:

To appreciate the significance of using inappropriate discounting, consider this example: A 45‐year‐old public sector employee earns $75,000 per year with no pension plan or other benefits. To help secure her retirement, her employer considers changing her compensation to $73,000 in salary plus a U.S. Treasury zero‐coupon bond that pays $5,000 in 20 years. The bond is selling in the market at $2,000. The Treasury bond’s implicit annual “discount rate” is thus 4.69 percent, i.e., $2,000 plus 4.69 percent interest compounded for 20 years equals $5,000.

The total compensation cost to the employer would remain $75,000. The employee, in turn, has three options:

Now suppose the public employer decides to be more paternalistic. Instead of giving the employee the Treasury bond worth $2,000, it promises her that in 20 years it will pay her $5,000. To fund this liability, the employer could deposit the $2,000 in a trust and have the trust buy the Treasury bond. The promise would then be fully funded by the trust. In 20 years, the Treasury bond would be redeemed for $5,000 and the proceeds forwarded to the employee. In the intervening 20 years, before the bond redemption and payment to the employee, the value of the future payment would increase with the passage of time, and increase (or decrease) as market interest rates decrease (or increase). But the value of the bond held in the trust would change identically to the liability, and the contractual obligation to pay $5,000 at age 65 would remain fully funded at every instant until paid, regardless of what happens in financial markets. Ignoring frictional costs and taxes, the employer’s cost of those actions would be the same as if it had paid the employee $75,000 in cash. And the employee’s total compensation would still be $75,000: $73,000 in cash plus a promise worth $2,000.

But instead of contributing the $2,000 and using it to buy the bond, the public employer could hire a public pension actuary and invest any trust contributions in a “prudent diversified” portfolio including assets, like equities, exposed to various market risks. The actuary would attest that the “expected” annual earnings of the portfolio over the long term is 7 percent (according to a sophisticated financial model). The actuary would then use the 7 percent to discount the $5,000 future payment and certify that the “cost” to the employer is $1,292, which is 35 percent less than the $2,000 cost of the Treasury bond. The actuary would certify that if the employer contributes the $1,292, its benefit obligation is “fully funded” because, if the trust earns the “expected return” of 7 percent (50 percent probable, after all), the $1,292 will accumulate to $5,000 in 20 years. The public employer can then claim it has saved taxpayers $708 ($2,000 – $1,292) by investing in a prudent diversified asset portfolio.

The question is, does it really cost only $1,292 to provide the same value as a $2,000 Treasury bond? Is $1,292 invested in the riskier portfolio worth the same as a Treasury bond that costs $2,000? Of course not. If it is possible to spin $1,292 of straw into $2,000 of gold, why would the government employer stop at pensions? Why not borrow as much as possible now and invest the proceeds in a prudent diversified portfolio expected to earn 7 percent and use the “expected” gains from taking market risk to pay for future general government expenditures?

The public employer is providing a benefit worth $2,000—a guarantee—and hoping to pay for it with $1,292 invested in a risky portfolio. The $708 difference represents the value of the guarantee that taxpayers will make good on any shortfall when the $5,000 comes due. The cost to taxpayers in total is still $2,000, but $708 is being taken from future generations by the current generation in the form of risk. Risk is a cost (precisely $708 in this example). Its price reflects the possibility as viewed by the market that future taxpayers ultimately may have to pay nothing at all if things go well, or a significant sum if they don’t.

Suppose the employer takes this logic one step further and, rather than promising $5,000 in 20 years, it contributes $1,292 to a defined contribution plan that invests in the same prudent diversified portfolio on the theory that the employee will be breaking even because the $1,292 is “expected” to accumulate to $5,000. The employee would be correct to view that as a cut in pay. The $708 cost of risk is shifted to the employee, reducing her compensation, instead of being borne by future taxpayers as in the case of the defined benefit plan.

The employee might complain. Future taxpayers cannot.

The only way for the employer to keep the employee whole with $73,000 of cash compensation plus a defined contribution plan is to contribute $2,000 to the plan. Whether it is invested in the Treasury bond or in riskier assets in the hope of higher returns, the value of her total compensation would still be $75,000.

Table 1 summarizes all these scenarios. The fourth column is the analog of public pension plans. Both the reported annual cost for the future $5,000 payment ($1,292) and the reported total compensation ($74,292) are understated. Investment professionals are paid well for managing risky assets for which high expected returns can be claimed. The actuary collects a fee. The employee has the value of the guarantee and bears none of the market risk being taken. Along with a happy employee, the public employer gets to report an understated compensation cost, freeing up money for other budget items. It’s good for all involved—except for the taxpayers on the hook for $708 in costs hidden by using the 7 percent discount rate.

Author(s): Larry Pollack

Publication Date: Winter 2023-2024

Publication Site: Cato Regulation

Excerpt:

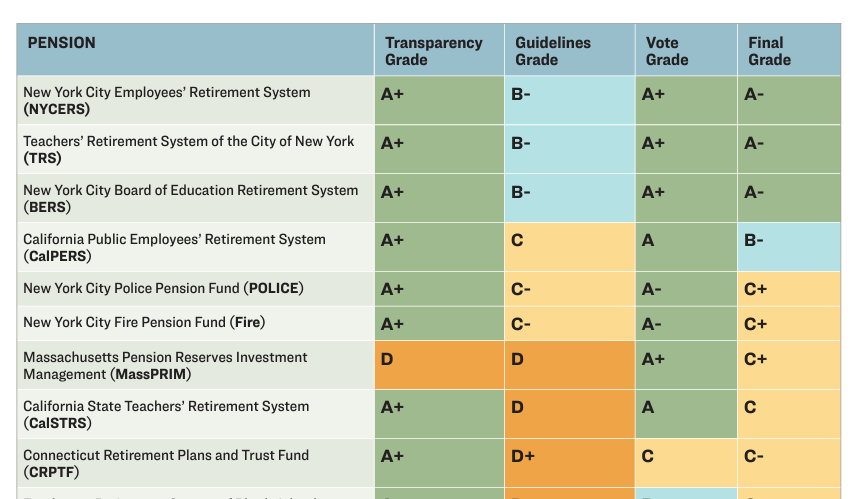

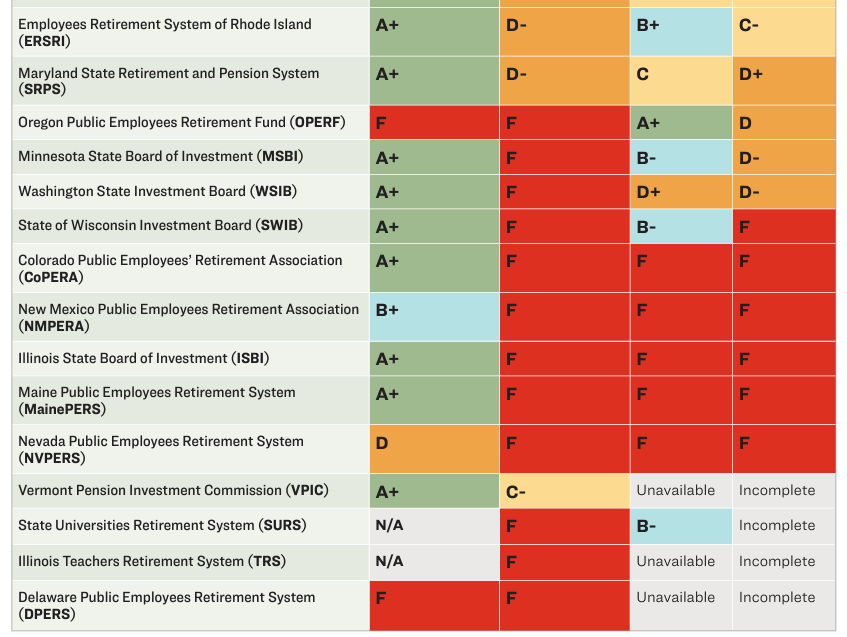

“Too few” public pension funds are addressing climate-related financial risk when it comes to proxy voting, according to a report released Jan. 23 by nonprofit organizations Sierra Club, Stand.earth and Stop the Money Pipeline.

The report, “The Hidden Risk in State Pensions: Analyzing State Pensions’ Responses to the Climate Crisis in Proxy Voting,” looked at 24 public pension funds with a collective $2 trillion in assets, including the $241.7 billion New York City Retirement Systems and state pension funds in California, Colorado, Connecticut, Delaware, Illinois, Maine, Maryland, Massachusetts, Minnesota, Nevada, New Mexico, Oregon, Rhode Island, Vermont, Washington and Wisconsin.

The pension funds were graded on their proxy-voting guidelines, proxy-voting records, and data transparency.

On proxy-voting guidelines, no pension system received an A grade, but three of the five New York City pension funds covering city employees, the Board of Education and teachers, earned a B for addressing systemic risk and climate resolutions. Half of the 24 pension funds studied earned an F.

….

“The findings of this analysis are clear: Far too few state pensions are taking adequate steps to address climate-related financial risks and protect their members’ hard-earned savings, raising serious concerns about their execution of fiduciary duty,” the report’s executive summary said.

….

Amy Gray, associate director of climate finance for Stand.earth, said it is disappointing to see many funds not using proxy-voting strategies to address the financial risks of climate change. “This report is a stark reminder that pension funds can — and must — do so much more to wield their massive investor power,” Gray said in the news release.

Author(s): Hazel Bradford

Publication Date: 23 Jan 2024

Publication Site: P&I

Report PDF: https://stand.earth/wp-content/uploads/2024/01/The-Hidden-Risk-in-State-Pensions-Report.pdf

Graphic:

Excerpt:

A first-of-its-kind report, the Hidden Risk analyzes the proxy voting records and proxy voting guidelines of the 19 public pensions that are in states where a state financial officer has indicated it is a priority issue both to advocate for more sustainable, just, and inclusive firms and markets , and to protect against climate risk.

Ahead of the 2024 shareholder season, a first-of-its-kind report “The Hidden Risk in State Pensions: Analyzing State Pensions’ Responses to the Climate Crisis in Proxy Voting,” from Stand.earth, Sierra Club and Stop the Money Pipeline, analyzes proxy voting records, proxy guidelines, and voting transparency of 24 public pension funds in the USA collectively representing over $2 trillion in assets under management (AUM).

These pensions are based in states where a state financial officer is a member of For the Long Term, a network that advocates for more sustainable, just, and inclusive firms and markets and strives to protect markets against climate risk.

The pensions analyzed include the pension systems of New York City and the states of California, Colorado, Connecticut, Delaware, Illinois, Maine, Maryland, Massachusetts, Minnesota, Nevada, New Mexico, Oregon, Rhode Island, Vermont, Washington, and Wisconsin.

Author(s):

Stand.earth

Sierra Club

Stop The Money Pipeline

Publication Date: 23 Jan 2024

Publication Site: Stand.earth

Graphic:

Publication Date: 23 Jan 2024

Publication Site: Treasury Dept

Graphic:

Excerpt:

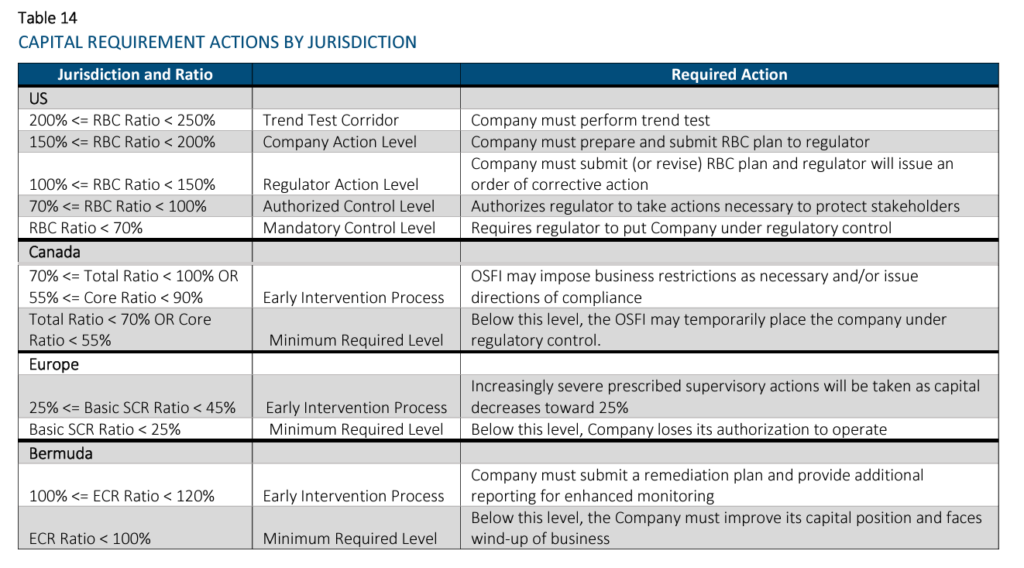

The purpose of this paper is to introduce the concept of capital and key related terms, as well as to compare and contrast four key regulatory capital regimes. Not only is each regime’s methodology explained with key terms defined and formulas provided, but illustrative applications of each approach are provided via an example with a baseline scenario. Comparison among these capital regimes is also provided using this same model with two alternative scenarios.

The four regulatory required capital approaches discussed in this paper are National Association of Insurance Commissioners’ (NAIC) Risk-Based Capital (RBC; the United States), Life Insurer Capital Adequacy Test (LICAT; Canada), Solvency II (European Union), and the Bermuda Insurance Solvency (BIS) Framework which describes the Bermuda Solvency Capital Requirement (BSCR). These terms may be used interchangeably. These standards apply to a large portion of the global life insurance market and were chosen to give the reader a better understanding of how required capital varies by jurisdiction, and the impact of the measurement method on life insurance company capital.

All of these approaches are similar in that they identify key risks for which capital should be held (e.g., asset default and market risks, insurance risks, etc.). However, they differ in significant ways too, including their defined risk taxonomy and risk diversification / aggregation methodologies, as well as required minimum capital thresholds and corresponding implications. Another key difference is that the US’s RBC methodology is largely factor-based, while the other methodologies are model-based approaches. For the model-based approaches, Solvency II and BIS allow for the use of internal models when certain conditions are satisfied. Another difference is that the RBC methodology is largely derived using book values, while the others use economic-based measurements.

As mentioned above, this paper provides a model that calculates the capital requirements for each jurisdiction. The model is used to compare regulatory solvency capital using identical portfolios for both assets and liabilities. For simplicity, we have assumed that all liabilities originated in the same jurisdiction as the calculation. As the objective of the model is to illustrate required capital calculation methodology differences, a number of modeling simplifications were employed and detailed later in the paper. The model considers two products – term insurance and payout annuities, approximately equally weighted in terms of reserves. The assets consist of two non-callable bonds of differing durations, mortgages, real estate, and equities. Two alternative scenarios have been considered, one where the company invests in riskier assets than assumed in the base case and one where the liability mix is more heavily weighted to annuities as compared to the base case.

Author(s): Ben Leiser, FSA, MAAA; Janine Bender, ASA, MAAA; Brian Kaul

Publication Date: July 2023

Publication Site: Society of Actuaries

Link: https://www.bloomberg.com/opinion/articles/2024-01-18/coinbase-trades-beanie-babies

Excerpt:

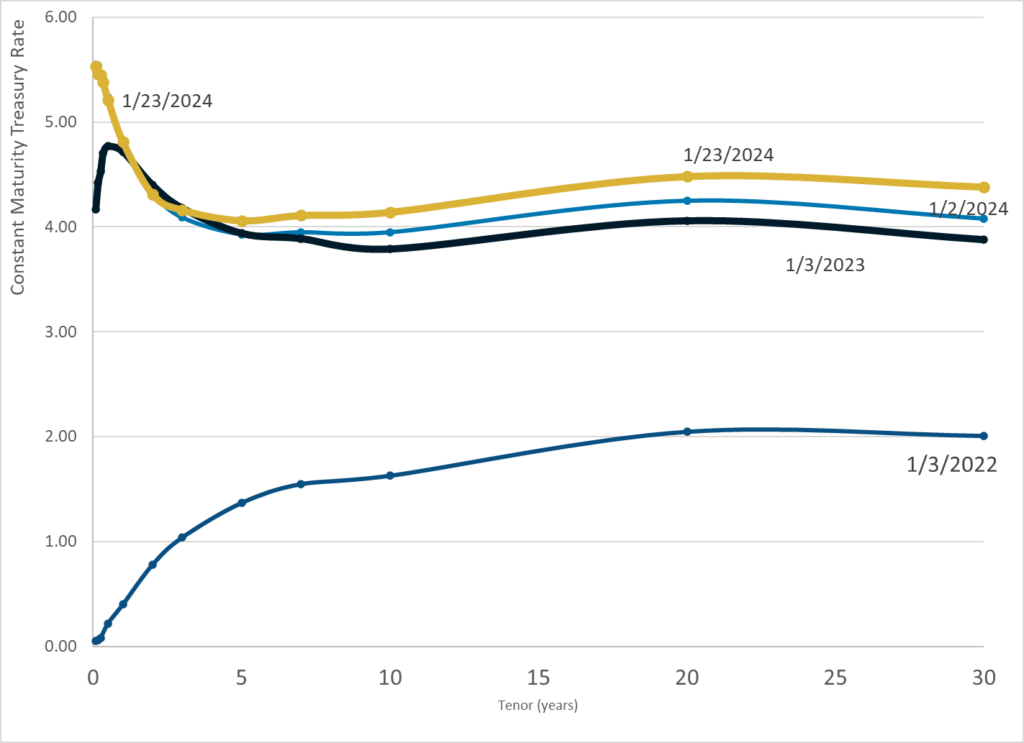

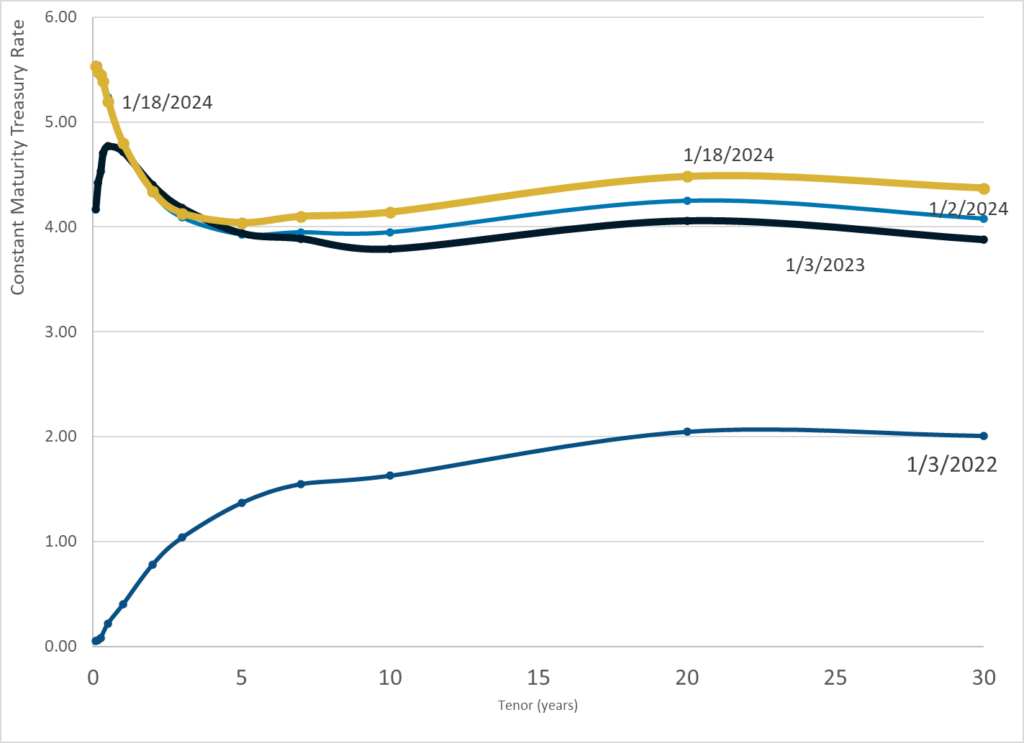

An important meta-story that you could tell about financial markets over the past few years would be that, for a long time, interest rates were roughly zero, which means that discount rates were low: A dollar in the distant future was worth about as much as a dollar today. Therefore, investors ascribed a lot of value to very long-term stuff, and were not particularly concerned about short-term profitability. Low discount rates made speculative distant-future profits worth more and steady current profits worth less.

And then interest rates went up rapidly starting in 2022, and everyone’s priorities shifted. A dollar today is now worth a lot more than a dollar in 10 years. People prioritize profits today over speculation in the future.

This is a popular story to tell about the boom in, for instance, tech startups, or crypto: “Startups are a low-interest-rate phenomenon.” In 2020, people had a lot of money and a lot of patience, so they were willing to invest in speculative possibly-world-changing ideas that would take a long time to pay out. (Or to fund startups that lost money on every transaction in the long-term pursuit of market share.) In 2022, the Fed raised rates, people’s preferences changed, and the startup and crypto bubbles popped.

I suppose, though, that you could tell a similar story about environmental investing? Climate change is, plausibly, a very large and very long-term threat to a lot of businesses. If you just go around doing everything normally this year, probably rising oceans won’t wash away your factories this year. But maybe they will in 2040. Maybe you should invest today in making your factories ocean-proof, or in cutting carbon emissions so the oceans don’t rise: That will cost you some money today, but will save you some money in 2040. Is it worth it? Well, depends on the discount rate. If rates are low, you will care more about 2040. If rates are high, you will care more about saving money today.

We have talked a few times about the argument that some kinds of environmental investing — the kind where you avoid investing in “dirty” companies, to starve them of capital and reduce the amount of dirty stuff they do — can be counterproductive, because it has the effect of raising those companies’ discount rates and thus making them even more short-term-focused. And being short-term-focused probably leads to more carbon emissions. (If you make it harder for coal companies to raise capital, maybe nobody will start a coal company, but existing coal companies will dig up more coal faster.)

But that argument applies more broadly. If you raise every company’s discount rate (because interest rates go up), then every company should be more short-term-focused. Every company should care a bit less about global temperatures in 2040, and a bit more about maximizing profits now. Maybe ESG was itself a low-interest-rates phenomenon.

Anyway here’s a Financial Times story about BlackRock Inc.:

BlackRock will stress “financial resilience” in its talks with companies this year as the $10tn asset manager puts less emphasis on climate concerns amid a political backlash to environmental, social and governance investing.

With artificial intelligence and high interest rates rattling companies globally, BlackRock wants to know how they are managing these risks to ensure they deliver long-term financial returns, the asset manager said on Thursday as it detailed its engagement priorities for 2024.

BlackRock reviews these priorities annually as it talks with thousands of companies before their annual meetings on issues ranging from how much their executives are paid to how effective their board directors are.

“The macroeconomic and geopolitical backdrop companies are operating in has changed. This new economic regime is shaped by powerful structural forces that we believe may drive divergent performance across economies, sectors and companies,” BlackRock said in its annual report on its engagement priorities. “We are particularly interested in learning from investee companies about how they are adapting to strengthen their financial resilience.”

There is a lot going on here, and it is reasonable to wonder— as the FT does — whether BlackRock’s shift from environmental concerns to high interest rates is about the political and marketing backlash to ESG. But you could take it on its own terms! In 2020, interest rates were zero, and BlackRock’s focus was on the long term. What was the biggest long-term risk to its portfolio? Arguably, climate change. So it went around talking to companies about climate change. In 2024, interest rates are high, and the short term matters more, so BlackRock is going around talking to companies about interest-rate risk.

I don’t know how AI fits into this model. For most of my life, “ooh artificial intelligence will change everything” has been a pretty long-term — like, science-fiction long-term — thing to think about. But I suppose now “how will you integrate large-language-model chatbots into your workflows” is an immediate question.

Author(s): Matt Levine

Publication Date: 18 Jan 2024

Publication Site: Bloomberg

Graphic:

Publication Date: 18 Jan 2024

Publication Site: Treasury Dept

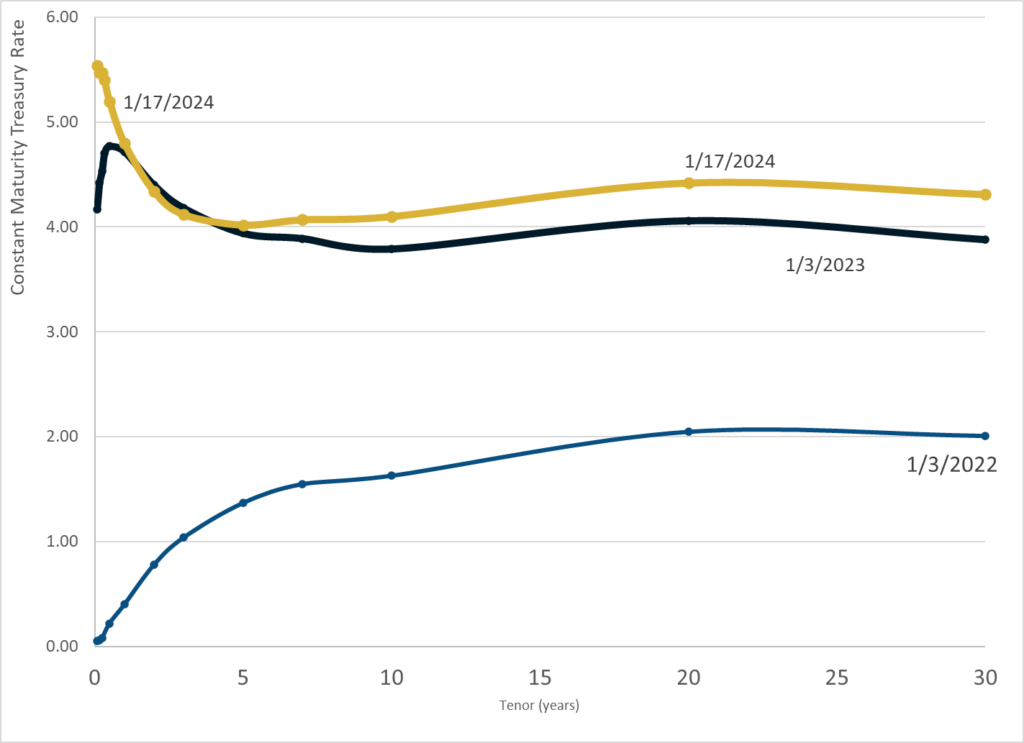

Graphic:

Publication Date: 17 Jan 2024

Publication Site: Treasury Dept

Link:https://www.bloomberg.com/opinion/articles/2024-01-17/making-esg-a-crime

Excerpt:

Oh sure whatever:

Republican lawmakers in New Hampshire are seeking to make using ESG criteria in state funds a crime in the latest attack on the beleaguered investing strategy.

Representatives led by Mike Belcher introduced a bill that would prohibit the state’s treasury, pension fund and executive branch from using investments that consider environmental, social and governance factors. “Knowingly” violating the law would be a felony punishable by not less than one year and no more than 20 years imprisonment, according to the proposal.

Pensions & Investments reports:

“Executive branch agencies that are permitted to invest funds shall review their investments and pursue any necessary steps to ensure that no funds or state-controlled investments are invested with firms that invest New Hampshire funds in accounts with any regard whatsoever based on environmental, social, and governance criteria,” the bill said.

The New Hampshire Retirement System “shall adhere to their fiduciary obligation and not invest with any firm that will invest state retirement system funds in investment funds that consider environmental, social, and governance criteria, as the investment goal should be to obtain the highest return on investment for New Hampshire’s taxpayers and retirees,” the bill said.

Investors aren’t allowed to consider governance! Imagine if this was the law; imagine if it was a felony for an investment manager to consider governance “with any regard whatsoever.”

….

I’m sorry, this is so stupid. “ESG” is essentially about considering certain risks to a company’s financial results: You might want to avoid investing in a company if its factories are going to be washed away by rising oceans, or if its main product is going to be regulated out of existence, or if its position on controversial social issues will cost it sales, or if its CEO controls the board and spends too much corporate money on wasteful personal projects. Obviously ESG in practice is also other, more controversial things:

But if you make it a crime for investors to consider certain financial risks then you get too much of those risks.

In particular, I suspect, you get too much governance risk. If every investor tomorrow said “okay we don’t care about the environment,” most companies probably wouldn’t ramp up their pollution: Their executives probably don’t want to pollute unnecessarily, polluting probably wouldn’t help the bottom line, and many companies just sit at computers developing software and couldn’t pollute much if they wanted to. But if every investor tomorrow said “okay we don’t care about governance,” then, I mean, “governance” is just a way of saying “somebody makes sure that the CEO is doing a good job and doesn’t pay herself too much.” If the investors don’t care about that, then a lot of CEOs will be happy to give themselves raises and spend more time on the corporate jet to their vacation homes.

Author(s): Matt Levine

Publication Date: 17 Jan 2024

Publication Site: Bloomberg

Excerpt:

In May, the United Kingdom’s version of the Securities and Exchange Commission will begin enforcing its pledge to crack down on so-called greenwashing by companies wishing to trade on the label of being green-friendly.

The Financial Conduct Authority’s rules, announced in late November, come as U.S. traders await stronger regulations from the SEC. That body moved in September to curb misleading marketing practices by requiring 80 percent of funds that claim to be “sustainable,” “green,” or “socially responsible” to actually be so.

The sustainability disclosure requirements are now deemed a necessity after regulators found “environmental, social, and corporate governance” analysts at Goldman Sachs and Germany’s DWS Group were promoting investments that were not as ESG-friendly as they claimed.

“The portfolio managers weren’t necessarily doing all of the work that they said they were doing,” the associate director of sustainability research for Morningstar Research Services LLC, Alyssa Stankiewicz, said. “They didn’t have documentation or data maybe related to the ESG-ness of these investments.”

At the same time as ESG-friendly firms are facing accusations of insincerity, they’re also coming under pressure from state pension funds in states with Republican-controlled governments that don’t want their employees’ retirement funds affected by what they view as politicized, left-leaning investing strategies.

Author(s): SHARON KEHNEMUI

Publication Date: 16 Jan 2024

Publication Site: NY Sun