Graphic:

Publication Date: 30 May 2023

Publication Site: Treasury Dept

All about risk

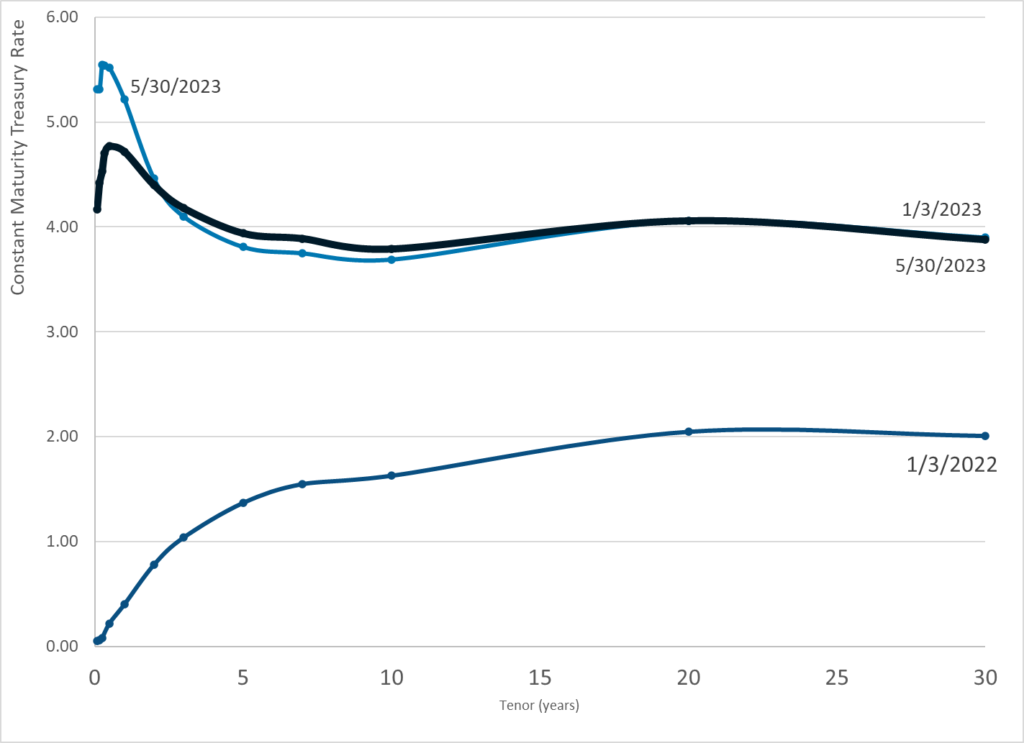

Graphic:

Publication Date: 30 May 2023

Publication Site: Treasury Dept

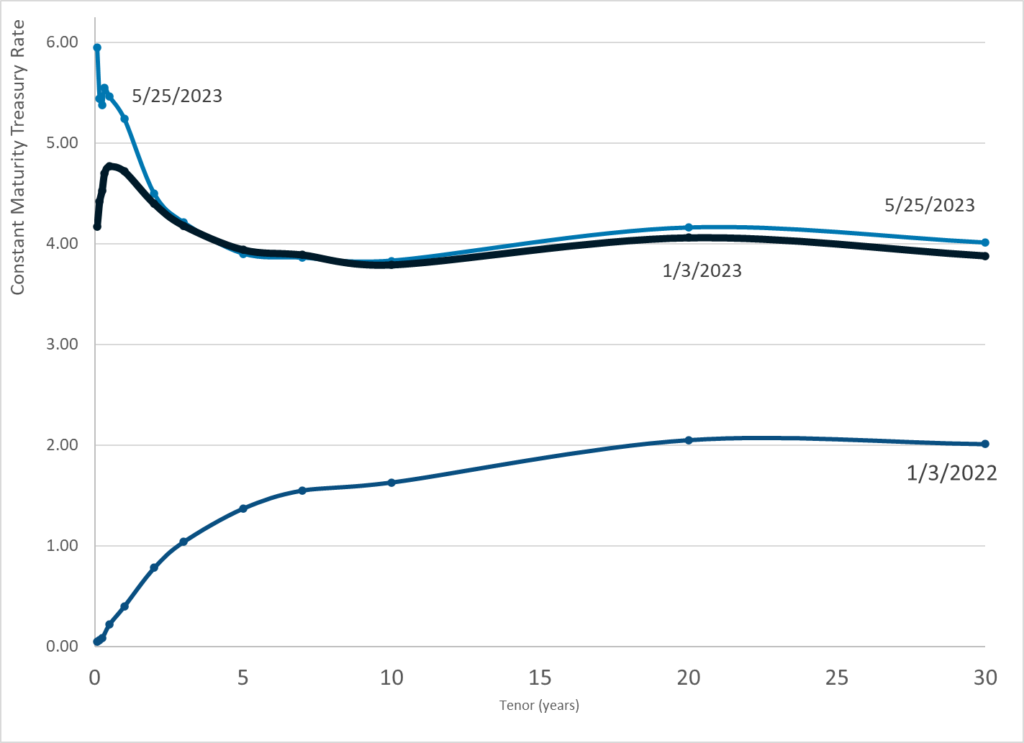

Graphic:

Publication Date: 25 May 2023

Publication Site: Treasury Dept

Link: https://www.thinkadvisor.com/2023/05/22/new-bill-would-exclude-social-security-from-income-tax/

Excerpt:

New legislation, H.R. 3206, the Senior Citizens Tax Elimination Act, would repeal the inclusion in gross income of Social Security benefits.

Social Security advocates criticized the bill, saying it would hurt the solvency of the Social Security and Medicare trust funds.

Under current law, up to 85% of a retiree’s Social Security benefits are taxed, depending on income. This tax revenue is deposited to the trust funds.

The bill specifies that taxes cannot be raised to replace this revenue.

Author(s): Melanie Waddell

Publication Date: 22 May 2023

Publication Site: Think Advisor

Link:https://jamanetwork.com/journals/jama/article-abstract/2804822/

JAMA. 2023;329(19):1662-1670. doi:10.1001/jama.2023.7022

Excerpt:

Key Points

Question How many excess deaths and years of potential life lost for the Black population, compared with the White population, occurred in the United States from 1999 through 2020?

Findings Based on Centers for Disease Control and Prevention data, excess deaths and years of potential life lost persisted throughout the period, with initial progress followed by stagnation of improvement and substantial worsening in 2020. The Black population had 1.63 million excess deaths, representing more than 80 million years of potential life lost over the study period.

Meaning After initial progress, excess mortality and years of potential life lost among the US Black population stagnated and then worsened, indicating a need for new approaches.

Author(s): César Caraballo, MD1,2; Daisy S. Massey, BA3; Chima D. Ndumele, PhD4; et al

Publication Date: 16 May 2023

Publication Site: JAMA Network

Excerpt:

CalPERS’ sense of privilege knows no bounds. The latest example is its Deputy Executive Officer, Communications & Stakeholder Relations Brad Pacheco unsuccessfully trying to ‘splain the very bad optics of Chief Investment Officer Nicole Musicco and her son getting NBA courtside playoff seats that are not available for purchase.

Even if Musicco was careful enough to have her receipt of these seats laundered through the box office, the pretense that a member of the general public could buy these seats is an insult to the intelligence of sports fans all over America.

….

Now one could argue that assuming Musicco bought the ticket, it’s still a sign of bad judgment for her to have gotten a courtside seat at a prized playoff game, the sort normally reserved for the connected and famous, and not state employees.2 But sports enthusiasts, season ticket resellers, and sports insiders all say no way, no how could Musicco have obtained these tickets, whether nominally purchased or not, without connected insiders making them available to her.

….

But aside from the decidedly bought-and-paid-for look, does Musicco winding up with these seats amount to a corruption problem under California law? If you read the relevant provisions with care, the answer is yes.

Musicco is at a level in the California government where she is required to make annual disclosure of outside income and her assets through a Statement of Economic Interests, more informally called a Form 700 (here is Musicco’s current Form 700). Form 700 filers are only allowed to receive a maximum of $590 in gifts from each source per year.

….

But rest assured Musicco would not have been able to collect this perk merely as a former partner in a sports-investment-happy fund; it is her status as current CalPERS Chief Investment Officer that makes her a celebrity-equivalent.

And keep in mind that celebrity treatment, normally kept well out of the public eye, is the norm in private equity. We’ve repeatedly discussed the soft corruption of government employees getting lavish perks like trips to attractive destinations with the fund manager providing lavish entertainment (such as the Stones and Elton John for the biggest funds) and meals, all charged to the fund, meaning the investors, meaning ultimately taxpayers. Here’s a recent indiscreetly-shared example from LinkedIn, of a sumptuous banquet at Westminster Abbey, of an annual meeting for Coller Capital, one of the largest private equity secondary investment firms (i.e., they buy the existing interests of limited partners). For once, enough gold to make even Donald Trump happy!

With that largess as not unusual, no wonder Musicco has come to see special treatment as normal.

Regardless, California takes an indulgent posture toward CalPERS, ignoring sins like cooking its books and covering up employee embezzlement.7 Remember, even in its pay to play scandal, where former CEO Fred Buenrostro was caught taking paper bags of cash, it was the Department of Justice,not the California Attorney General, that successfully prosecuted him, resulting in a four-and-a-half-year prison sentence. Even though the general public will take offense at the latest chicanery, CalPERS’ status in California as too big to fail apparently means it is too big to be disciplined.

Author(s): Yves Smith

Publication Date: 18 May 2023

Publication Site: naked capilism

Excerpt:

Although the regional hospital in the city of Orangeburg delivers babies, the birth outcomes in the county are awful by any standard. In 2021, nearly 3% of all Black infants in Orangeburg County died before their 1st birthday.

Nationally, the average is about 1% for Black infants and less than 0.5% for white infants.

Meanwhile, Orangeburg County’s infant mortality rate for babies of all races is the highest in South Carolina, according to the latest data published by the South Carolina Department of Health and Environmental Control.

By 2030, the federal government wants infant mortality to fall to 5 or fewer deaths per 1,000 live births. According to annual data compiled by the Centers for Disease Control and Prevention, 16 states have already met or surpassed that goal, including Nevada, New York, and California. But none of those states are in the South, where infant mortality is by far the highest in the country, with Mississippi’s rate of 8.12 deaths per 1,000 live births ranking worst.

Even in those few Southern states where infant mortality rates are inching closer to the national average, the gap between death rates of Black and white babies is vast. In Florida and North Carolina, for example, the Black infant mortality rate is more than twice as high as it is for white babies. A new study published in JAMA found that over two decades Black people in the U.S. experienced more than 1.6 million excess deaths and 80 million years of life lost because of increased mortality risk relative to white Americans. The study also found that infants and older Black Americans bear the brunt of excess deaths and years lost.

….

The state Department of Health and Human Services — which administers Medicaid, the health coverage program for low-income residents, and pays for more than half of all births in South Carolina — claims accidental deaths were the No. 1 reason babies covered by Medicaid died from 2016 to 2020, according to Medicaid spokesperson Jeff Leieritz.

But the state health department, where all infant death data is housed, reported birth defects as the top cause for the past several years. Accidental deaths ranked fifth among all causes in 2021, according to the 2021 health department report. All but one of those accidental infant deaths were attributed to suffocation or strangulation in bed.

Author(s): Lauren Sausser

Publication Date: 22 May 2023

Publication Site: Kaiser Health News

Link: https://nypost.com/2023/05/20/nyc-pension-funds-lose-2m-in-first-republic-signature-banks/

Excerpt:

City pension funds had almost $2 million invested with First Republic and Signature banks — losing it all when both banks failed this year.

The losses were contained in new data The Post obtained from the city Comptroller’s office under a Freedom of Information Law request.

Though a federal bailout rescued bank depositors, the city’s pension cash had been invested in bank stocks and bonds.

“The overall loss is negligible in the context of the daily market motions of our $240 billion pension funds,” said Chloe Chik, spokesperson for Comptroller Brad Lander.

All five city pensions funds were hit in the bank failures.

Author(s): Jon Levine

Publication Date: 20 May 2023

Publication Site: NY Post

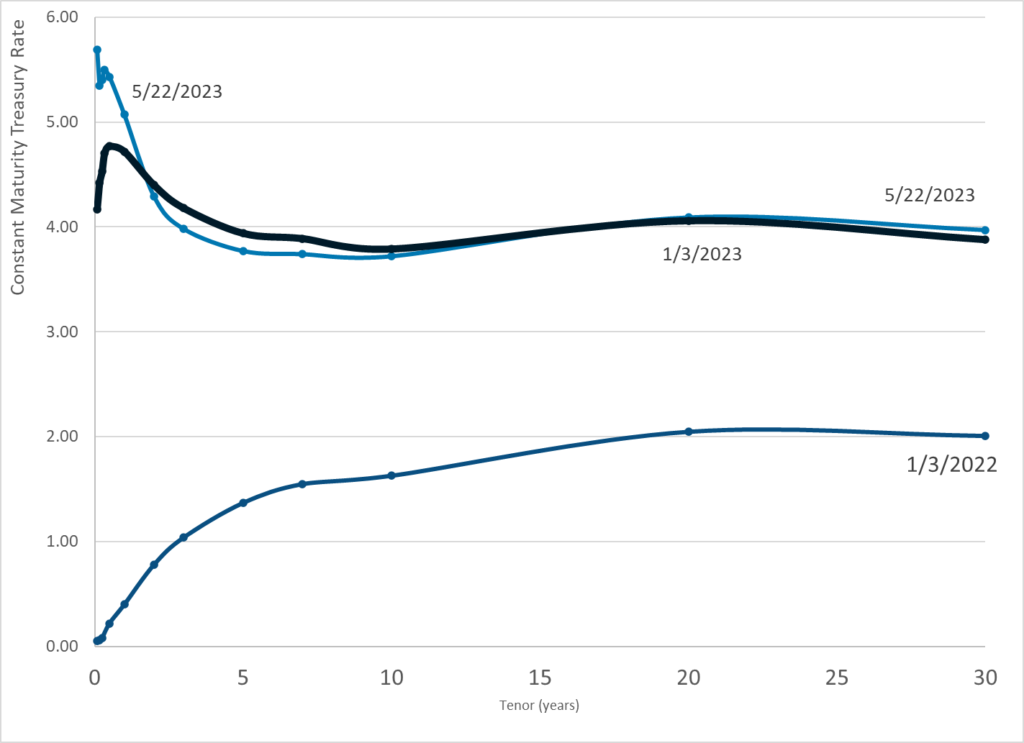

Graphic:

Publication Date: 22 May 2023

Publication Site: Department of Treasury

Graphic:

Excerpt:

First, we need to simplify our rules while strengthening them. Too many areas of regulation across our economy have become so complicated with weird formulas, dizzying methodologies, and endless loopholes and carveouts. We need simpler rules to prevent future disasters. A better alternative is to create bright line limits, with clear sanctions, including size caps and growth restrictions. Clearly observable metrics make it easier to monitor and increase consistency.

Second, we need to stop subsidizing the largest and riskiest banks by giving out free deposit insurance. When small banks fail, they rarely lead to much cost to the FDIC’s Deposit Insurance Fund, since they can be fairly easily wound down or sold. But when large banks fail, the costs to the Deposit Insurance Fund and broader economy can be steep. To make matters worse, those institutional clients with the biggest deposits feel they can get around insurance limits by going to the biggest banks. In other words, people perceive that the biggest banks get free deposit insurance over the legal limits by way of their too-big-to-fail status.

Fixing our deposit insurance pricing structure is just one small step that could help address this problem. Large, riskier banks should pay more and small, simpler banks should pay less. We should also make the framework countercyclical, so that we aren’t in the position of raising rates when banking conditions are weak.

While today’s proposed special assessment will not fall on small, local banks, the failure of First Republic Bank will be a direct hit to the Deposit Insurance Fund that is not being recouped through this special assessment. It’s a reminder that we need to fix the fund’s pricing over the long term.

Finally, as Swiss policymakers made clear regarding the recent turmoil involving Credit Suisse, more people are saying the quiet part out loud: the current resolution plans filed by the largest financial institutions in the world, which purport to show how the firms could fail without a government bailout or economic chaos, are essentially a fairy tale.5

The latest failures are another reminder that we must work to eliminate the unfair advantages bestowed upon too-big-to-fail banks. New laws and old laws alike provide a roadmap to end too-big-to-fail and the resulting risks to financial stability, fair competition, and the rule of law.6

Author(s): Rohit Chopra

Publication Date: 11 May 2023

Publication Site: Consumer Finance Protection Bureau

Link: https://kffhealthnews.org/news/article/prison-health-impact-american-life-expectancy-aging/

Excerpt:

Thousands of people like Jordan are released from prisons and jails every year with conditions such as cancer, heart disease, and infectious diseases they developed while incarcerated. The issue hits hard in Alabama, Louisiana, and other Southeastern states, which have some of the highest incarceration rates in the nation.

A major reason the U.S. trails other developed countries in life expectancy is because it has more people behind bars and keeps them there far longer, said Chris Wildeman, a Duke University sociology professor who has researched the link between criminal justice and life expectancy.

“It’s a health strain on the population,” Wildeman said. “The worse the prison conditions, the more likely it is incarceration can be tied to excess mortality.”

Mass incarceration has a ripple effect across society.

Author(s): Fred Clasen-Kelly

Publication Date: 27 April 2023

Publication Site: KFF Health News

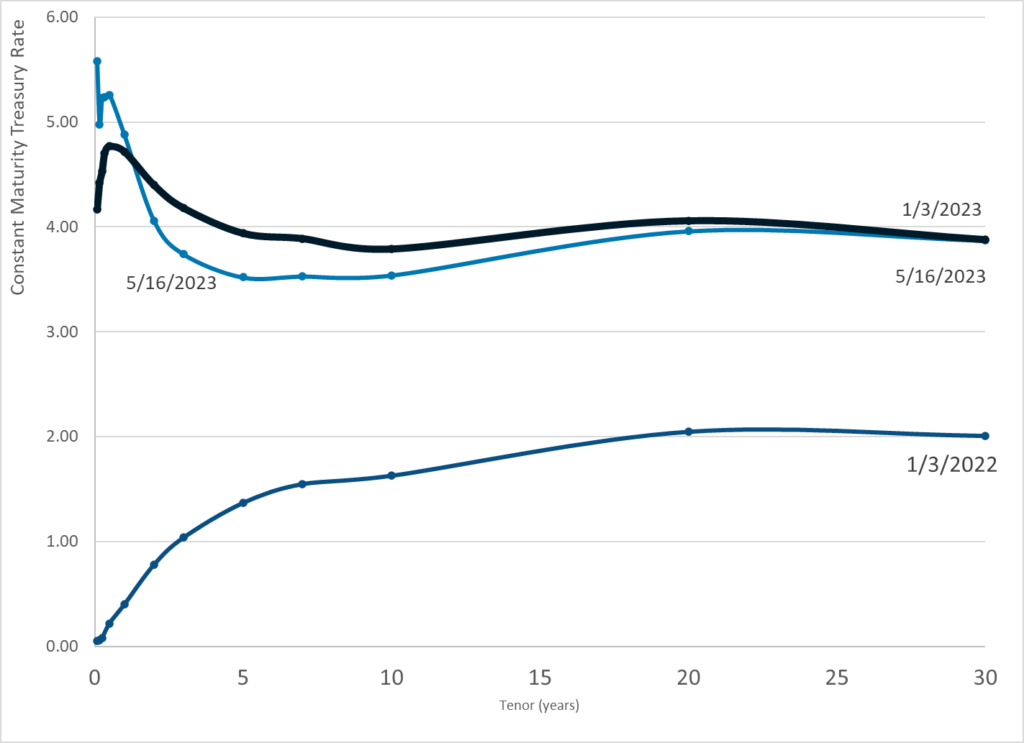

Graphic:

Publication Date: 16 May 2023

Publication Site: Treasury Dept

Link: https://www.visualcapitalist.com/american-workforce-100-people/

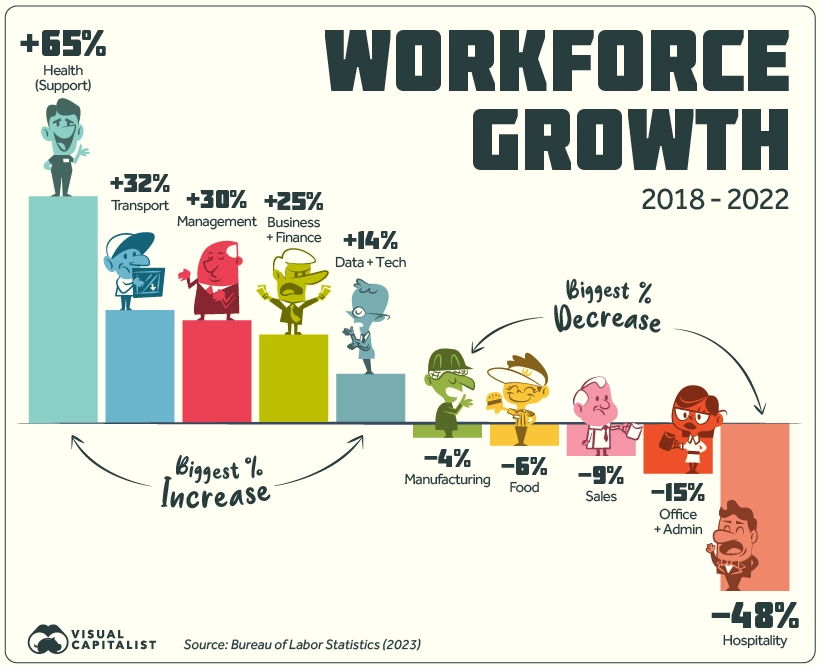

Graphic:

Excerpt:

Over the last five years, the American workforce has not stayed static. Of the listed 22 groups, 13 saw growth in employment numbers, nine saw a decrease, and one stayed flat since 2018.

The top gainer by far is Health Support (medical assistants, care aides, orderlies, etc.) which grew by 65%. Looking at the timeline of growth does not paint a steady picture: employment jumped between 2018 and 2019, briefly fell in 2020, and has since risen again in 2021-2022.

Another top gainer is Transport, rising from the 4th to 3rd biggest employer, beating out Sales in 2022. Business & Finance and Management have also seen steady increases since 2018.

On the other hand Hospitality saw a staggering 48% drop in numbers, not all together surprising given the impact of the COVID-19 pandemic as well as the rise of tech companies like Airbnb.

Meanwhile, Office & Admin work saw a 15% loss in employees, even though this category is still the biggest employer in the country by a significant margin. Although jobs in this group saw steady declines from 2018-2021, it registered a slight uptick in workers between 2021 and 2022.

Author(s): Pallavi Rao

Publication Date: 15 May 2023

Publication Site: Visual Capitalist