Link: https://www.politico.com/news/2023/03/13/barney-frank-signature-bank-collapse-warren-trump-00086765

Excerpt:

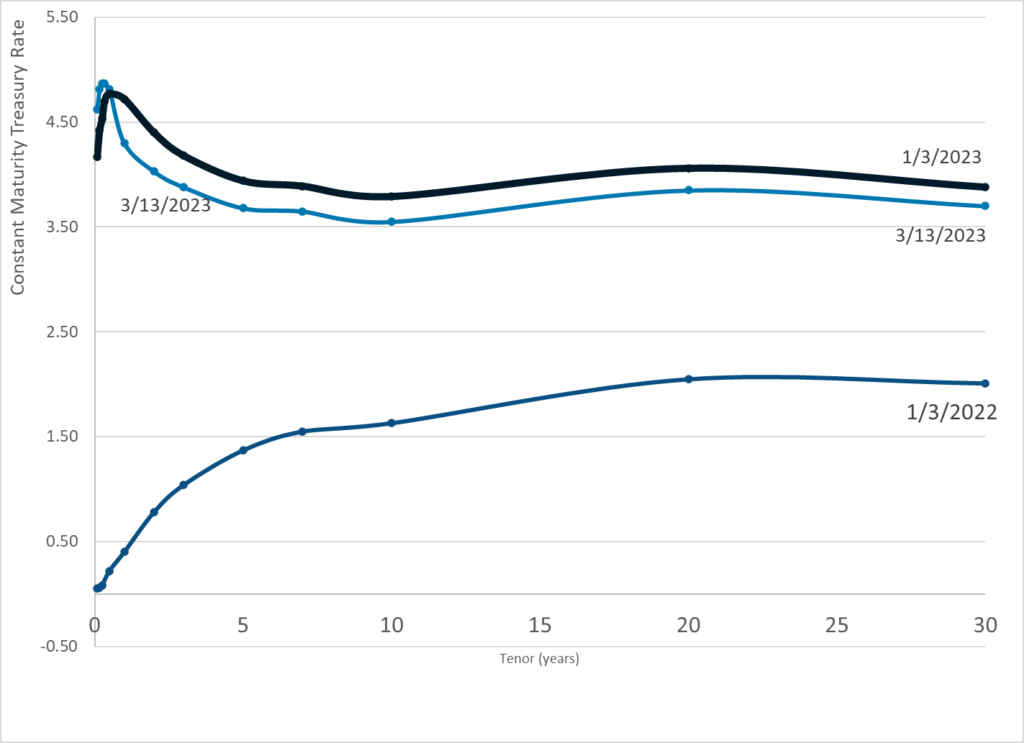

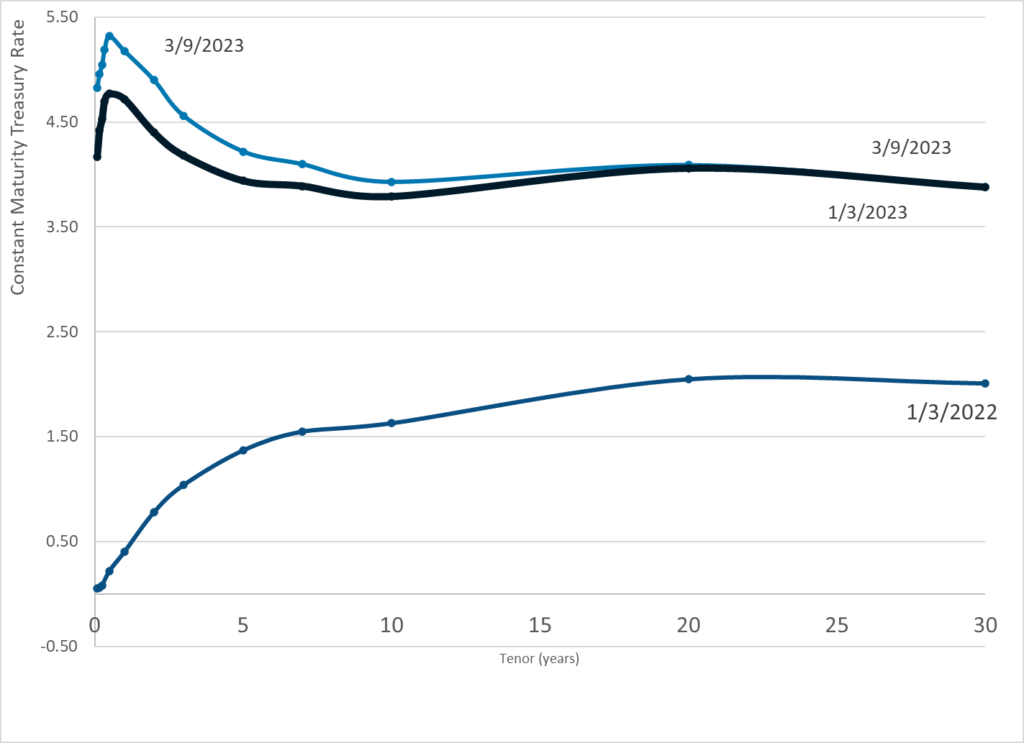

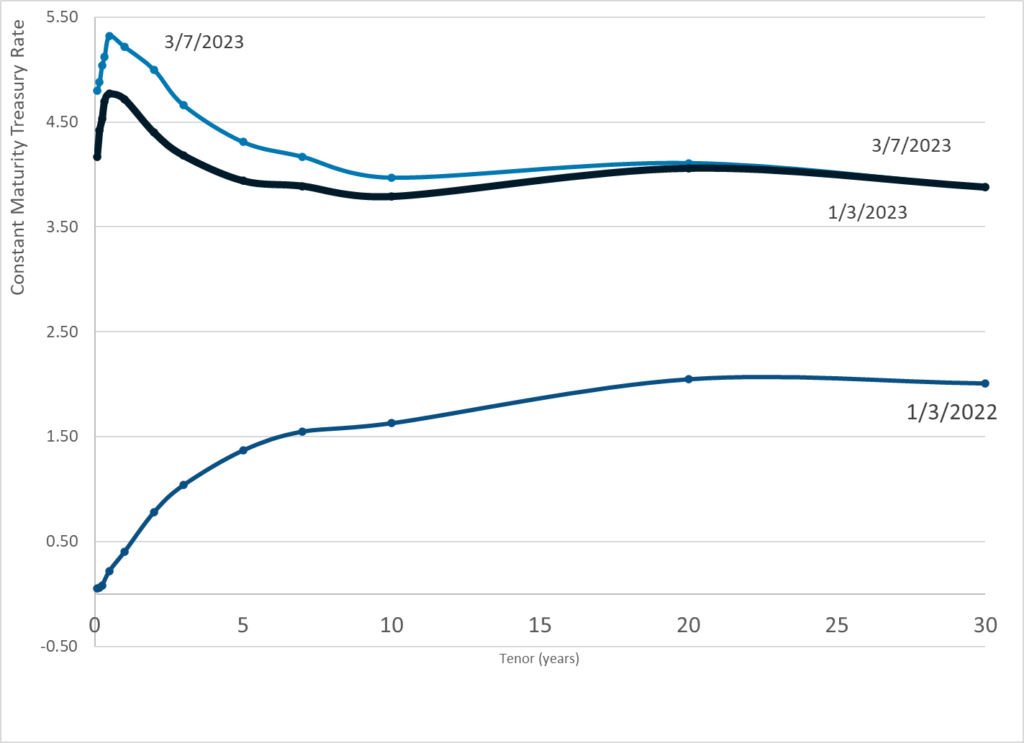

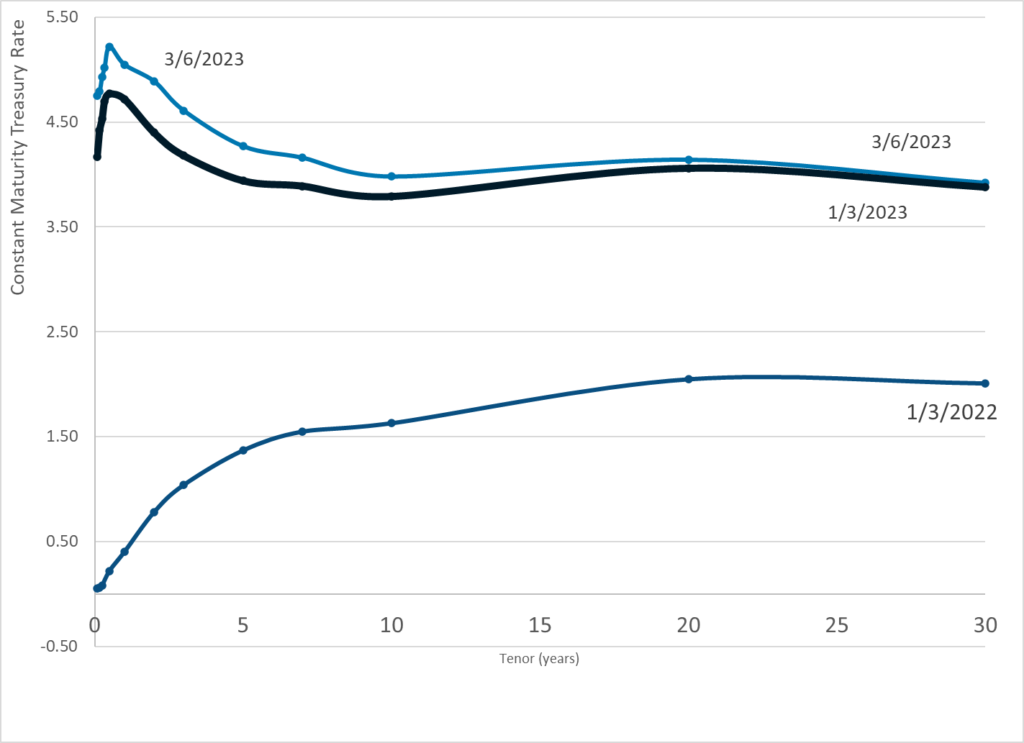

From his front-row seat, [Barney Frank] blames Signature’s failure on a panic that began with last year’s cryptocurrency collapse — his bank was one of few that served the industry — compounded by a run triggered by the failure of tech-focused Silicon Valley Bank late last week. Frank disputes that a bipartisan regulatory rollback signed into law by former President Donald Trump in 2018 had anything to do with it, even if it was driven by a desire to ease regulation of mid-size and regional banks like his own.

“I don’t think that had any impact,” Frank said in an interview. “They hadn’t stopped examining banks.”

But Warren, a fellow Massachusetts Democrat who designed landmark consumer safeguards that ended up in Frank’s 2010 banking law, is placing the blame firmly on the Trump-era changes that relaxed oversight of some banks and says Signature is a prime example of the fallout. Warren argues that, had Congress and the Federal Reserve not rolled back stricter oversight, Silicon Valley Bank and Signature would have been better able to withstand financial shocks.

Author(s): ZACHARY WARMBRODT

Publication Date: 13 Mar 2023

Publication Site: Politico