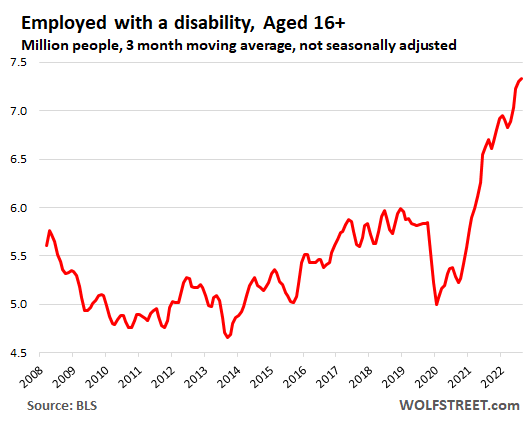

The number of people with a disability who were employed in January spiked by 27% from January 2020, to 7.29 million in January — with December at 7.37 million having been the highest in the data from the BLS going back to 2008:

A number of states have programs in which they actively monitor municipal finances and roughly 20 have emergency manager laws allowing for direct intervention. People have long debated how effective these oversight programs are at generating a real recovery and what the right level of intervention even is. Duly elected city officials don’t like being told what to do by state overseers. States on the other hand, typically want troubled cities to just buckle down and take their advice—even if it’s tough medicine.

So while the whole point of these programs is to avoid or mitigate extreme distress, they can also create or exacerbate tension between cities and states along the way.

By all accounts, Chester’s approach to being placed in Pennsylvania’s municipal distress program in 1995 was to just ignore the state’s advice. Fred Reddig, a retired state official who has coordinated recovery plans for a number of distressed municipalities, worked on Chester’s case from 1995 to the early 2000s. He recalls that during that time, it was difficult to compel local officials to follow any of the state’s recommendations and that relations were tense.

….

Rob DiAdamo, a lecturer at Boston University’s law school who teaches a class on state and local governance, noted many communities that end up under some form of state oversight had structural economic problems long before the state intervened.

“It may be more effective for the state to be looking at how to bring opportunities back to these communities than wait for the crisis and have people argue about the best way to address it,” he said. “It’s like waiting for the patient to have a heart attack and discussing treatment options when the crisis could have potentially been avoided by first encouraging healthier eating habits and exercise.”

The wearing of masks to prevent the spread of COVID-19 and other respiratory illnesses had almost no effect at the societal level, according to a rigorous new review of the available research.

“Interestingly, 12 trials in the review, ten in the community and two among healthcare workers, found that wearing masks in the community probably makes little or no difference to influenza-like or COVID-19-like illness transmission,” writes Tom Jefferson, a British epidemiologist and co-author of the Cochrane Library’s new report on masking trials. “Equally, the review found that masks had no effect on laboratory-confirmed influenza or SARS-CoV-2 outcomes. Five other trials showed no difference between one type of mask over another.”

That finding is significant, given how comprehensive Cochrane’s review was. The randomized control trials had hundreds of thousands of participants, and made useful comparisons: people who received masks—and, according to self-reporting, actually wore them—versus people who did not. Other studies that have tried to uncover the efficacy of mask requirements have tended to compare one municipality with another, without taking into account relevant differences between the groups. This was true of an infamous study of masking in Arizona schools conducted at the county level; the findings were cited by the Centers for Disease Control and Prevention (CDC) as reason to keep mask mandates in place.

Everything will be settled without a big problem for investors, predicts Robert Hunkeler, International Paper’s vice president of investments.

“I guess Congress and the White House will eventually finish their game of chicken, and the debt limit will be raised,” he opines. “There might be a little more drama and brinksmanship this time around, because there are more cooks in Congress than usual, and that’s saying a lot. Either way, I wouldn’t change my investments because of it.”

To Kostin and his Goldman staff, the risk that Congress fails to boost the debt limit by the deadline is “higher than at any point since 2011,” but “the team believes it’s more likely that Congress will raise the debt limit before the Treasury is forced to delay scheduled payments.”

If the debt ceiling is not raised in time to make those payments, in Goldman’s estimate, the economy would shrink by about $225 billion per month, or 10% of annualized gross domestic product. That’s provided that the Treasury does what policy wonks call, “prioritize,” meaning somehow continuing to pay interest on the national debt, but to stop payment on other obligations.

For Thomas Swaney, CIO for global fixed income at Northern Trust Asset Management, another credit downgrade for the government is possible.

“The practical implications of a credit downgrade are not entirely clear,” he writes in a report. “But we don’t expect a modest downgrade to result in market disruptions for Treasuries, U.S. agency debt or overnight repurchase agreements.”

Despite such tragedies, Missouri is one of two states — the other is Montana — that do not prohibit all drivers from text messaging while operating vehicles. (Missouri has such a law for people 21 and under.)

Before this year, Missouri state lawmakers from both parties had proposed more than 80 bills since 2010 with varying levels of restrictions on cellphone use and driving. Similar legislation has been proposed in Montana, too. In both states, such bills have faltered, largely because Republican opponents say they don’t think the laws work and are just another infringement on people’s civil liberties.

Nevertheless, Missouri Republicans and Democrats introduced at least seven bills this session concerning hand-held phone use while driving — and road safety advocates think such legislation has a better chance of passing this year. Montana, meanwhile, has a bill seeking to block localities’ distracted driving laws.

….

Supporters of hands-free driving laws concede that distracted driving restrictions are not a panacea for all traffic fatalities. And even if Missouri passes additional restrictions on cellphone use, small nuances in wording could influence whether such a law is effective.

Nationwide, about 3,000 people typically die in distracted driving crashes each year, according to National Highway Traffic Safety Administration data, though researchers suggest that’s an undercount. While hands-free options are now standard for new vehicles, the number of distracted driving deaths has stayed relatively steady. They represented at least 1 in 12 traffic fatalities in 2020.

Distracted driving laws reduce fatalities — if, like the ones established in 24 states, they ban all hand-held cellphone use rather than banning only a specific activity such as texting, according to the Governors Highway Safety Association and a study published in 2021 in the journal Epidemiology. Banning texting alone does not make a difference, those researchers found.

Oregon and Washington saw significant reductions in the rates of monthly rear-end crashes when they broadened their laws to prohibit “holding” a cellphone as compared with states that banned only texting, according to a study from the Insurance Institute for Highway Safety. Those two states also prohibited holding a phone when stopped temporarily — say, at a red light.

A key driver of the conflict is around fiscal management and disclosure. Amid its budget troubles, the city has racked up $750,000 in Internal Revenue Service penalties related to unpaid payroll taxes, fell victim to a $400,000 phishing scam that wasn’t publicly disclosed for months, cycled through two chief financial officers in as many years and has failed to produce an audited financial report since 2018. But perhaps the most striking example of the problems surrounding the city’s bankruptcy is the discord—and conflicting information—around Chester’s underfunded police pension.

Like other distressed cities, Chester has an outsized pension liability and annual pension bills that would take up a substantial portion of its budget if paid in full. But also like other cities, Chester hadn’t been paying its entire bill—called the Minimum Municipal Obligation (MMO) in Pennsylvania. In 2021, the city paid its full MMO for the first time since 2013 and it was a significant lift. The total it spent on pension and retiree health care costs that year—$14.6 million—took up 28% of its entire general fund.

But there’s a bigger problem: Due to accounting practices that inflated the plan’s assets and a dispute over what the city’s police pension formula actually is, no one really knows what Chester’s true unfunded liabilities are.

Welcome back to the 79th edition of Data Vis Dispatch! Every week, we’ll be publishing a collection of the best small and large data visualizations we find, especially from news organizations — to celebrate data journalism, data visualization, simple charts, elaborate maps, and their creators.

Recurring topics this week include wintery weather, social inequality, and inflation.

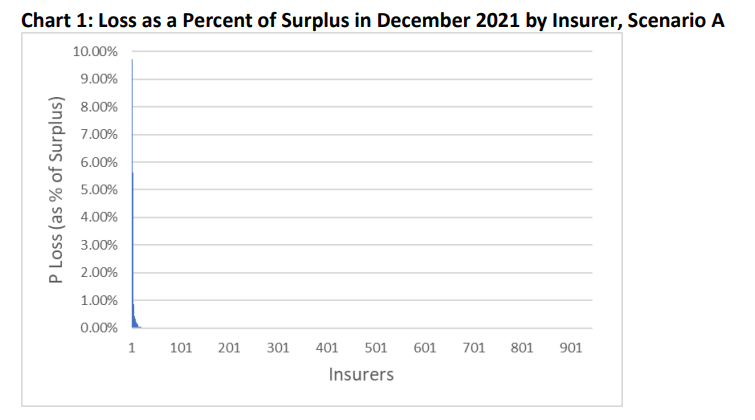

The stress test analysis found that 1,114 U.S. insurers, with a surplus of about $1.2 trillion, held some amount of CLO tranches modeled. Similar to last year’s stress testing results, we found that the losses on insurers’ CLO investments that were modeled, even in the stressed scenarios, were highly concentrated.

To understand the impact of potential losses on insurers, principal loss (compare with Table 7) for scenarios A, B, and C was divided by each insurer’s year-end 2021 total surplus. For each scenario, the principal loss as a percentage of total surplus for each of the 1,114 insurers was sorted from highest to lowest. Then the insurer with the largest percentage loss was referenced as “Insurer 1,” the insurer with the second largest percentage loss was referenced as “Insurer 2,” and so on until the smallest percentage loss, which was referenced as “‘Insurer 1,114” (x-axis). Please note the difference in the scale of the y-axis in Charts 1, 2, and 3.

Chart 1 shows the distribution of losses as a percentage of surplus for December 2021’s Scenario A. Although the bulk of insurers show no losses, 49 of the 1,114 insurers experienced losses in this scenario. Intuitively, the losses were derived primarily from CCC-rated CLO tranches. The largest loss as a percentage of surplus under Scenario A was 9.72%. Similar to the analysis for year-end 2020, no insurers experienced double digit losses.

Author(s): Jean-Baptiste Carelus, Eric Kolchinsky, Hankook Lee, Jennifer Johnson, Michele Wong, Azar Abramov

Publication Date: Jan 2023

Publication Site: NAIC Capital Markets Special Reports

Canada’s system of Medicare — a point of national pride — was strained before the COVID-19 pandemic hit. It’s now teetering on the brink, with some Conservative provincial leaders salivating at the prospect of privatization.

For months, provincial premiers have been demanding that the federal government increase health transfer payments. Indeed, the cost-sharing model which sees the federal government currently kick in around 22 percent of health funding should be revised so that Ottawa pays more of the bill. Although a deal to boost federal funding appears to be in sight, Prime Minister Justin Trudeau and the Liberals are failing to ensure that protecting public health care delivery is a part of it.

….

Canada’s health care crisis is in large part a labor crisis. In general, unceasing anguish over a generalized “labor shortage” in Canada has had only the most tenuous relationship to reality. In the health care sector, however, worker burnout and a consequent lack of staff are all too real. While the Canadian Federation of Independent Business, the mouthpiece of Canadian employers, bemoaned a purportedly economy-wide labor shortage that was crippling business, an actual dearth of nurses and other health care professionals snowballed as deteriorating pay and working conditions drove these workers out of their jobs.

Newly released Statistics Canada payroll data helps paint the picture. Overall payroll figures show year-over-year employment across the whole economy virtually unchanged in November 2022, despite the Bank of Canada’s aggressive series of interest rate hikes (how much longer stable employment numbers will persist is debatable). Job vacancies — the bugbear of employers in Canada for most of the past year — declined another 2.4 percent, down to 850,300 from 1,002,200 at their peak, and reached their lowest post-pandemic level since August 2021. Average weekly wage growth, while continuing to lag inflation, ticked upward slightly to 4.2 percent (5.3 percent in goods-production alone).

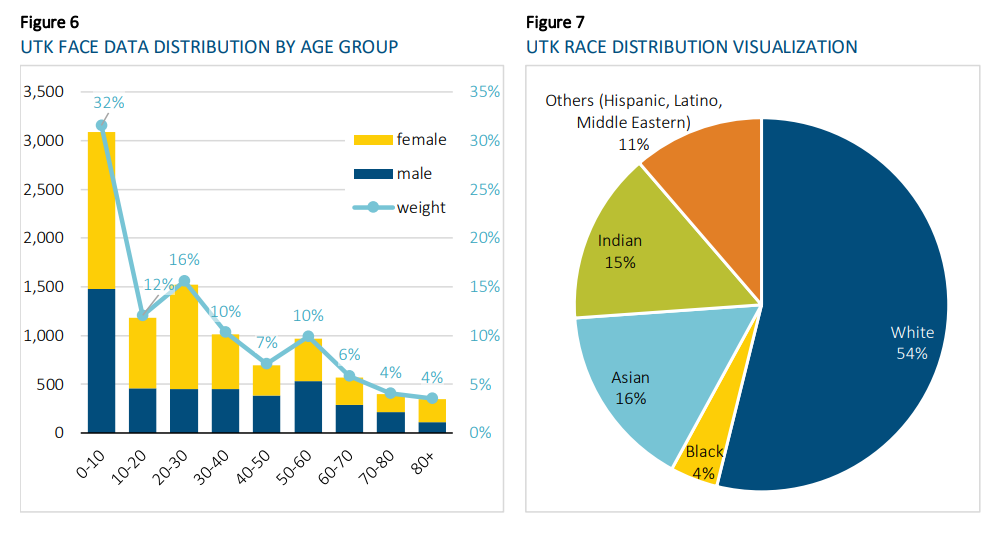

This paper is an introduction to AI technology designed for actuaries to understand how the technology works, the potential risks it could introduce, and how to mitigate risks. The author focuses on data bias as it is one of the main concerns of facial recognition technology. This research project was jointly sponsored by the Diversity Equity and Inclusion Research and the Actuarial Innovation and Technology Strategic Research Programs