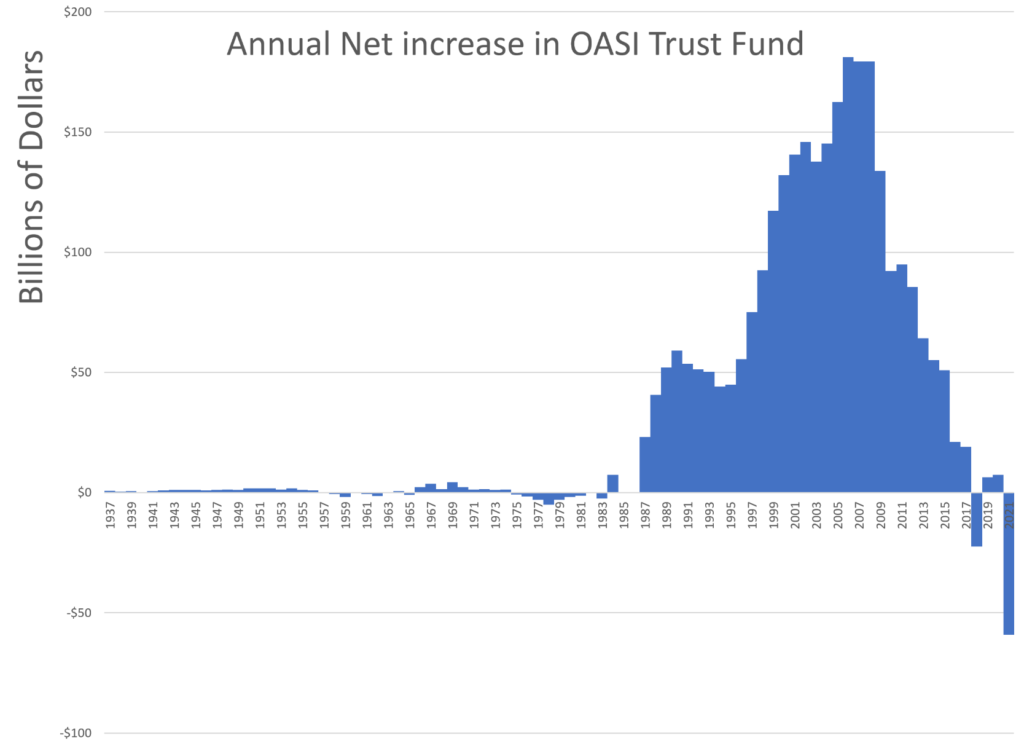

I am graphing the net change in the OASI (that’s the old age benefit part) Trust Fund, year-over-year.

I think you can easily see all those glorious years the Boomer payroll taxes were being stuffed into the Trust Fund… but really flowing right out into current spending for other goodies.

And you can see when that reversed and is now negative, and will continue to be negative until the Trust Fund is exhausted, in the early 2030s.

Candidates for Illinois governor are taking different approaches on how they’d tackle the state’s unfunded pension liabilities.

Illinois has among the most unfunded public sector employee pension liability. State numbers indicate around $151 billion unfunded, but some place like the American Legislative Exchange Council place the debt at $533 billion.

State Sen. Darren Bailey, who’s running against incumbent Democratic Gov. J.B. Pritzker, said he’ll use reduced state spending to pay down pensions.

“We’ll find the fat in the budget and we’ll begin to apply that to get this pension situation under control, but first and foremost, I will be sitting at the table with pensioners,” Bailey, R-Xenia, told The Center Square. “I fear that the pension debt may be that large looming problem that will sneak up on Illinois if we continue to ignore it as J.B. Pritzker has.”

Pritzker touts on his campaign website “fully funding pension contributions” as a way to reduce state pension liabilities, “going above and beyond with payments and expanding the employee pension buyout program.”

Pritzker’s campaign did not return requests for an interview.

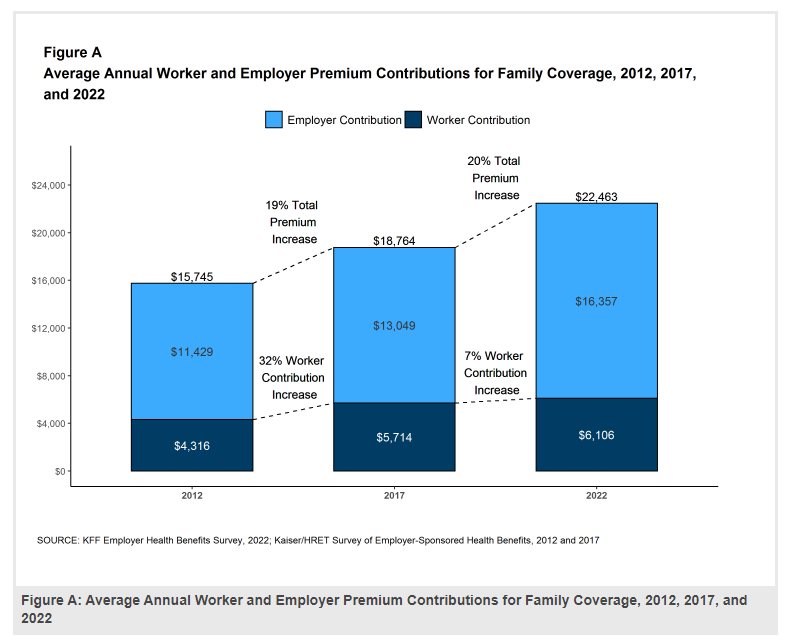

This 24th annual survey of employers provides a detailed look at trends in employer-sponsored health coverage, including premiums, employee contributions, cost-sharing provisions, offer rates, wellness programs, and employer practices. The 2022 survey included 2,188 interviews with non-federal public and private firms.

Annual premiums for employer-sponsored family health coverage reached $22,463 this year, with workers on average paying $6,106 toward the cost of their coverage. The average deductible among covered workers in a plan with a general annual deductible is $1,763 for single coverage. Workers at smaller firms contribute on average contribute nearly $2,000 more toward the cost of family coverage than workers at smaller firms. They also face general annual deductibles that are $1,000 higher on average. This year’s report also looks at employers’ experiences and views about mental health and substance use services, telemedicine, and wellness programs.

While the City of Baltimore extended the Fire & Police Pension System from a 20-year retirement plan to a 25-year one, a Baltimore City Council committee advanced a bill on Thursday to allow city elected officials to receive pension after eight years, rather than 12 years.

Baltimore City FOP Tweeted Friday saying, “This is one of the most egregious privileged class moves against labor in the history of Baltimore City.”

Baltimore City FOP went on to say the City Council should either vacate this decision, or start the process of returning the Fire & Police Pension System back to 20 years.

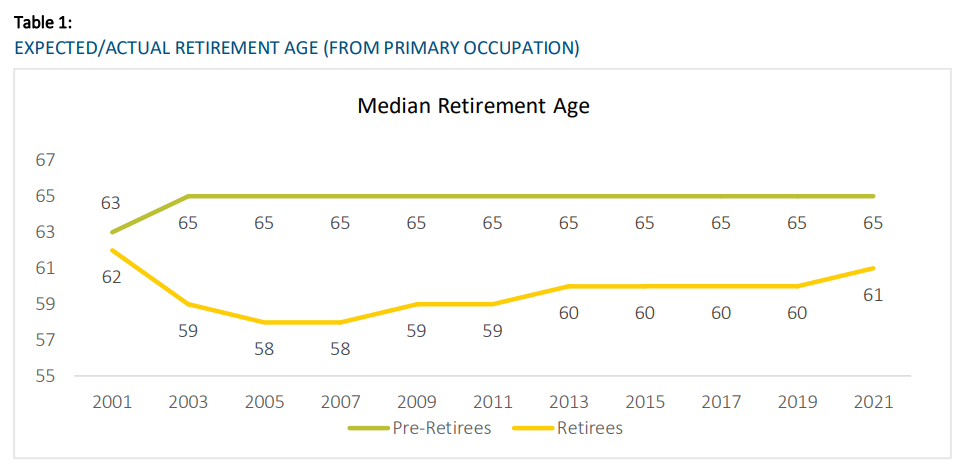

CHAPTER HIGHLIGHTS: • Despite the COVID-19 pandemic, level of concern about various risks remains historically low this year for both pre-retirees and retirees. Compared to 2019, level of concern dropped on some issues for retirees. As a result of this drop, retiree concerns are lower than those of pre-retirees by a larger gap than ever before. • The one exception to this trend was concern about fraud. In 2021, both retirees and pre-retirees were more concerned about fraud, and it is the highest concern among retirees, particularly Black/African American retirees. As in prior studies, those with lower income tend to show much higher levels of concern. • The biggest concerns for pre-retirees are their savings and investments not keeping up with inflation, not being able to afford long-term care, not being able to afford health care costs, not being able to maintain a reasonable standard of living throughout retirement, and potentially depleting all their savings. • While half of pre-retirees plan to retire gradually rather than all at once, retiree respondents indicate this seldom actually happens. Higher-income pre-retirees are more likely to plan to go straight from full time employment to retirement. • The COVID-19 pandemic has not affected plans that pre-retirees have for work, living arrangements, and lifestyle in retirement, although over a quarter report changing their lifestyle. • Despite the financial challenges that retirement poses, most do not have financial advisors, especially preretirees, lower-income respondents, and Black/African American respondents.

Milliman, Inc., a premier global consulting and actuarial firm, today released the results of its latest Milliman 100 Pension Funding Index (PFI), which analyzes the 100 largest U.S. corporate pension plans.

During October, the Milliman 100 PFI funded ratio rose from 108.8% on September 30 to 112.8% on October 31, reaching a new high for the year. The change was driven by a 35-basis-point hike in the monthly discount rate. The PFI projected benefit obligation decreased to $1.266 trillion as the discount rate rose from 5.36% in September to 5.71% for October—the highest rate since March 2010. This increase helped to offset October’s flat investment returns of 0.21%, which lowered the Milliman 100 PFI asset value by $4 billion.

BERLIN, Nov 5 (Reuters) – Germany’s more than 20 million pensioners will likely see their state benefit rise by up to 4.2% from July 2023, according to a governemt proposal seen by Reuters, lower than the expected inflation rate of 7.0%.

The state pension in western Germany will rise by 3.5%, while in former East Germany it will increase by 4.2% according to the draft, as the government continues to narrow the gap between the two regions.

A treaty adopted 35 years ago and meant to solve an entirely different problem is also protecting the climate. And with bipartisan support from the Senate and President Joe Biden’s Oct. 26 signature, the U.S. became the world’s 139th nation to adopt a key amendment to that agreement — the first time the U.S. has joined a legally binding global measure specifically to combat climate change.

Global warming was on the back burner in 1985 when scientists from the British Antarctic Survey found a gaping hole in the planet’s stratospheric ozone layer. A natural feature of the atmosphere, the ozone layer is located between about 10 to 25 miles above Earth’s surface. It shields the planet from the sun’s ultraviolet radiation, which is harmful in large doses to our skin and to myriad other aspects of plant and animal life.

Researchers rapidly pinned down the cause of the ozone destruction: chlorofluorocarbons, known as CFCs, which are chemicals used as refrigerants and to manufacture aerosol sprays and other materials. CFCs had been recognized for years as a threat to the ozone layer, but the ozone hole found in the mid-1980s was far worse than anything expected by that point.

By 1987, diplomats had crafted a treaty known as the Montreal Protocol to fix the problem. It was an immense success, ratified by every member state of the United Nations.

There was a major catch, though.

Both CFCs and their leading replacements – hydrofluorocarbons, or HFCs – trap heat in the atmosphere, causing global warming.

….

Enter the Kigali Amendment.

Adopted at a United Nations meeting held in the Rwanda capital in October 2016, it uses a variety of policy approaches to throttle back on both the production and consumption of HFCs. The amendment has put the world on track to eliminate more than 80% of HFCs by midcentury.

One reason the Kigali Amendment passed the Senate with bipartisan support (69-27, including 21 of the chamber’s 50 Republicans) is that national action on HFCs along the lines of Kigali was already in gear. The pandemic stimulus bill of late 2020 specified an 85% cut in HFC production by 2030. Many lawmakers, especially those from states with major chemical manufacturing, had recognized that cutting HFCs made sense. For one thing, nations that have not ratified the amendment cannot trade HFCs with those that have.

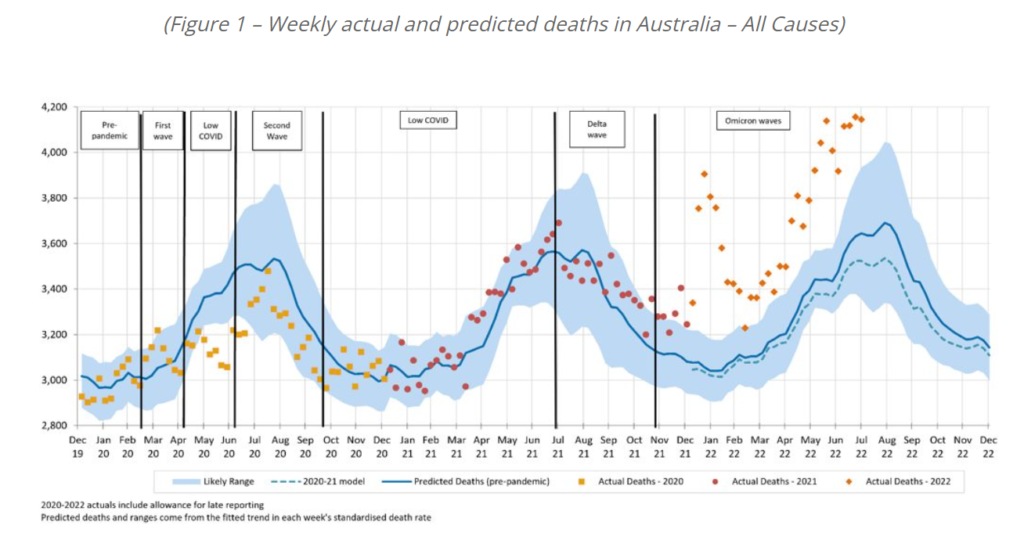

Total excess mortality for the month of July 2022 is estimated at 16% (+2,600 deaths), relative to expected mortality at pre-pandemic levels.

Total excess mortality for the first seven months of 2022 is 14% (+13,700 deaths).

Around half of the excess mortality for the first seven months of 2022 is due to COVID-19 (+7,100 deaths) with remaining excess of +6,600 due to the remaining causes.

October 2022 has the lowest COVID-19 surveillance deaths of any month in 2022.

We estimate that COVID-19 deaths will result in excess mortality of around 6% (+2,800) for August to October 2022, with overall excess mortality likely to be higher than this.

We continue to expect that COVID-19 will be the third leading cause of death in Australia in 2022.