Link: https://content.naic.org/sites/default/files/publication-fah-zu-financial-analysis-handbook.pdf

Graphic:

Excerpt:

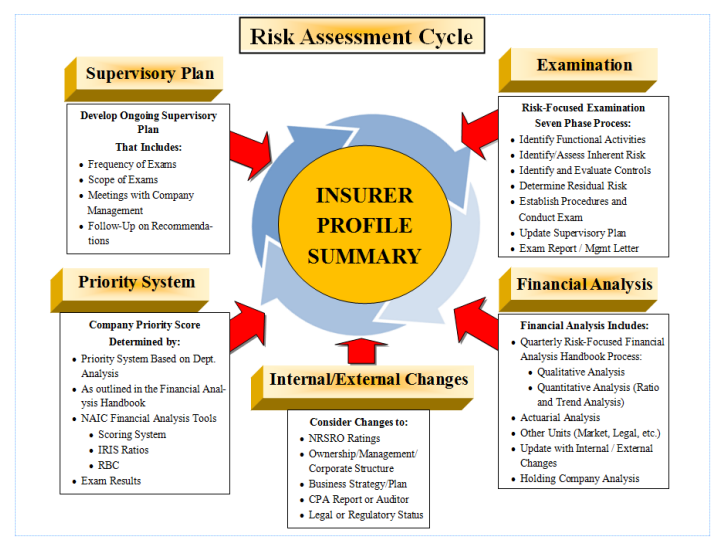

The risk-focused surveillance framework is designed to provide continuous regulatory oversight. The risk-focused approach requires fully coordinated efforts between the financial examination function and the financial analysis function. There should be a continuous exchange of information between the field examination function and the financial analysis function to ensure that all members of the state insurance department are properly informed of solvency issues related to the state’s domestic insurers.

The regulatory Risk-Focused Surveillance Cycle involves five functions, most of which are performed under the current financial solvency oversight role. The enhancements coordinate all of these functions in a more integrated manner that should be consistently applied by state insurance regulators. The five functions of the risk assessment process are illustrated within the Risk-Focused Surveillance Cycle.

As illustrated in the Risk-Focused Surveillance Cycle diagram, elements from the five identified functions

contribute to the development of an IPS. Each state will maintain an IPS for its domestic companies. State

insurance regulators that wish to review an IPS for a non-domestic company will be able to request the IPS from the domestic or lead state. The documentation contained in the IPS is considered proprietary, confidential information that is not intended to be distributed to individuals other than state insurance regulators.Please note that once the Risk-Focused Surveillance Cycle has begun, any of the inputs to the IPS can be changed at any time to reflect the changing environment of an insurer’s operation and financial condition.

Author(s): NAIC staff

Publication Date: 1 Jan 2022

Publication Site: NAIC